Individual License: $4,950 | Team and Enterprise License Options Available

Key Takeaways

Download Table of Contents

World Market for Oncology Imaging AI – Markintel™ Horizon Report (2023–2032)

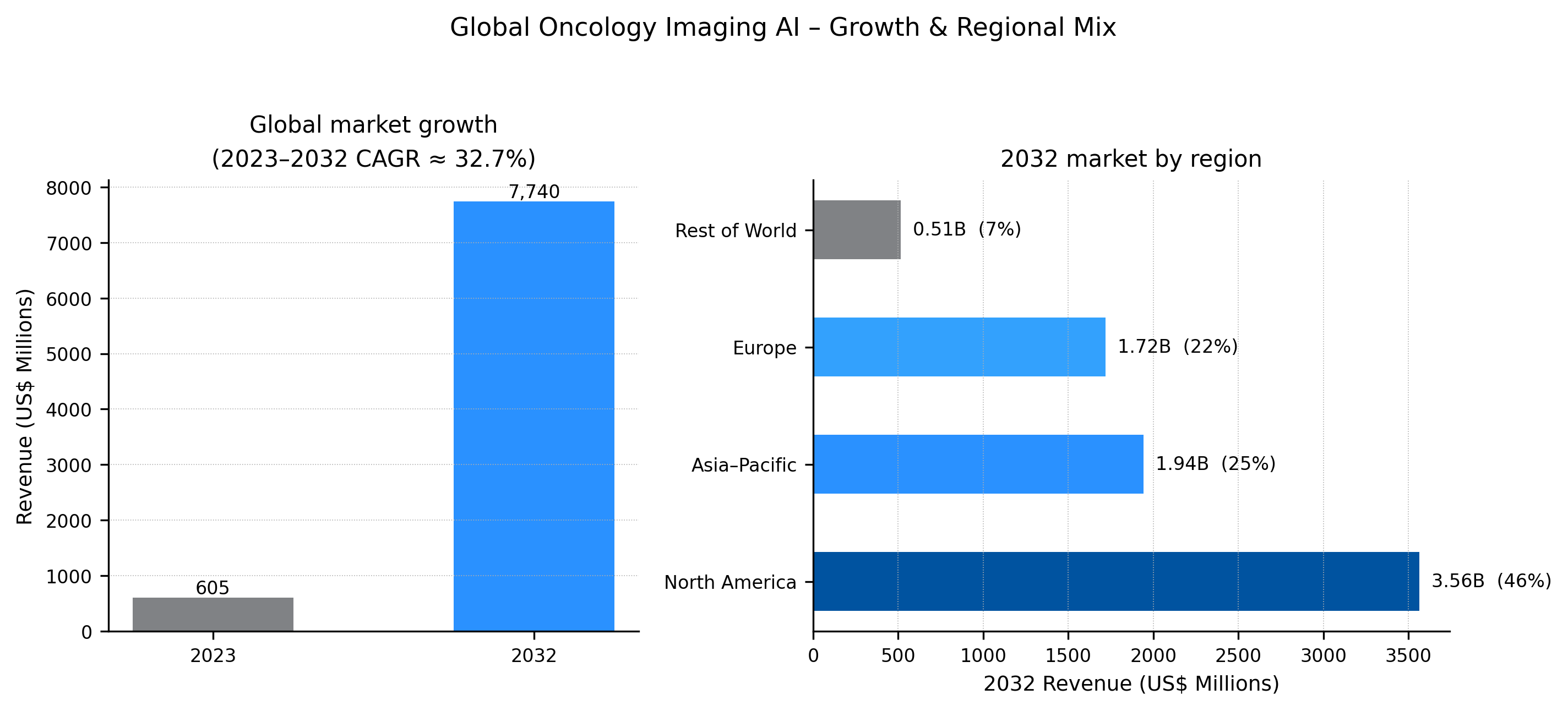

This Horizon report is Marketstrat’s dedicated deep dive on how AI is reshaping oncology imaging pathways globally—from breast and lung screening to complex CT/MRI staging, PET-based theranostics, and RT planning. The analysis quantifies the global market for Oncology Imaging AI from 2023 through 2032, then layers in a full competitive and GTM lens tailored to vendors, providers, and investors.

The report measures all imaging-centric AI software and AI‑linked revenue deployed across the oncology pathway (screening, detection, staging, treatment planning, response, and surveillance) across five core modalities—CT, X‑ray/DR (incl. DBT), MRI, PET/Nuclear, and Ultrasound—and a full buyer set spanning cancer centers, IDNs/AMCs, community providers, and teleradiology networks.

Beyond sizing, the study is structured as a practical playbook. Each major stakeholder cluster—AI software vendors, imaging OEMs, RT/TPS players, AI platforms & cloud orchestrators, provider/telerad networks, and imaging‑pharma/CROs—is analyzed through Markintel’s proprietary strategy frameworks, with explicit recommendations on attach‑rate expansion, packaging, evidence building, and partnership models. The goal is not just to explain the market, but to help decision makers sequence investments, shape offers, and defend margins in a fast‑moving but noisy category.