ONE BIG THING

Capacity economics is replacing algorithm novelty as imaging AI’s core battleground — validated this week by MASAI’s workload evidence, GE’s throughput-focused MRI clearances, and a tariff ruling that shifts OEM procurement conversations from cost volatility to capacity outcomes.

KEY TAKEAWAYS

- Policy shock absorber (but not a free pass): The week’s major macro signal is a Supreme Court decision invalidating IEEPA-based tariff authority—reducing near-term import-cost volatility for medtech and imaging equipment; however, other tariff lanes (e.g., Section 232) remain a residual risk vector, so procurement teams should treat this as “volatility down,” not “risk gone.” Following the Supreme Court’s ruling, the Administration has confirmed a 15% temporary surcharge (Section 122) effective immediately—up from the 10% figure discussed in our initial analysis.

- The Bottom Line: For medtech supply chains (especially MRI/CT components), the “10% risk” in our model is now a “15% hard cost” for the next 150 days. Adjust your Q2 margin forecasts accordingly.

- MRI platforms are pushing toward “installability + uptime” economics: GE HealthCare’s new FDA clearances for SIGNA Sprint, SIGNA Bolt, and SIGNA One software reinforce the OEM roadmap: faster installs, simplified site footprints (incl. helium-minimized designs), and software-defined workflow layers that directly target throughput and serviceability—not just image quality.

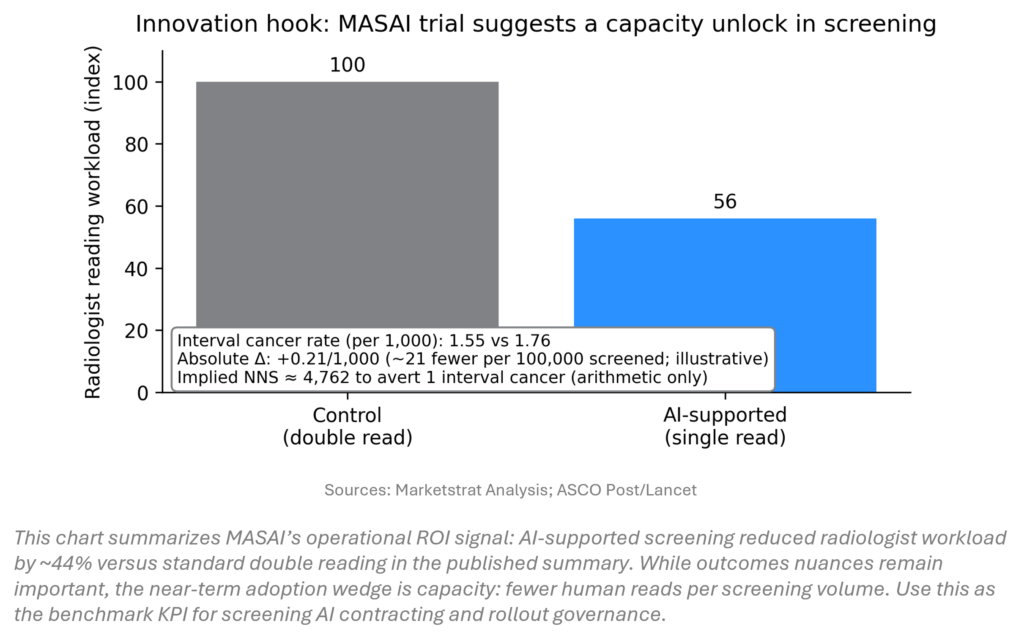

- Screening evidence that matters operationally: MASAI’s final results indicate ~44% radiologist workload reduction with AI-supported screening vs standard double reading, while interval cancer outcomes appear directionally improved but not statistically decisive in topline reporting—still, this is the kind of “labor productivity” evidence that can move budgets and workflow design in population screening programs.

- Platformization is real at scale: Asklepios’ rollout of Aidoc across 28 hospitals (Germany) is a clean data point that enterprise AI is increasingly sold like infrastructure—multi-site standardization, IT governance, and operational use cases—rather than stand-alone “apps.”

- Lung AI commercialization (UPDATE): Median appointing a U.S. president for eyonis LCS is a go-to-market “muscle build” step following prior clearance momentum—an indicator that lung screening AI is shifting from regulatory milestones to distribution, referral economics, and contracting execution.

- MIS/robotics keeps accelerating (and matters for imaging adjacencies): Medtronic’s first U.S. commercial Hugo case plus Banner’s robot fleet expansion (49 systems) show procedural platforms expanding aggressively; this has second-order impacts on imaging utilization (pre-op planning, intra-op imaging, post-op surveillance) and reinforces hospital capital prioritization dynamics. The competitive landscape is also shifting: J&J submitted its Ottava robotic system to the FDA in January 2026, setting up a three-way platform race (Intuitive, Medtronic, J&J) that will intensify hospital capital allocation decisions and raise the bar for imaging ROI narratives competing in the same budget envelope.

- Payment reality check: Two signals—provider-based compliance reminders (site-of-service attribution) and policy proposals for paying for AI—underscore that near-term “AI monetization” is more likely to be achieved via enterprise contracts, workflow ROI, and risk-sharing than clean per-scan reimbursement expansion.

QUICK GLANCE TABLE

| Date | Headline | Our Take | Source |

| 2026-02-20 | Supreme Court limits IEEPA tariff authority | Near-term cost volatility down for OEMs/providers; Section 232 remains the watch item for “tariff re-entry.” | NPR/CNBC/Reuters |

| 2026-02-19 | GE clears SIGNA Sprint/Bolt + SIGNA One | Clear signal the OEM battle is install + uptime + software stack; providers should demand measurable throughput and service KPIs in contracts. | GE + trade press |

| 2026-02-20 | GE + BARDA expand AI ultrasound | “Federal readiness” funding validates AI imaging for surge operations; watch for workflow/IP spillover into commercial ultrasound and ED pathways. | Trade press |

| 2026-02-14* | MASAI: AI-supported screening reduces workload ~44% | Strongest “AI ROI” data point this week is labor productivity, not reimbursement; screening programs are the near-term adoption wedge. | ASCO Post/Lancet |

| 2026-02-18 | Asklepios rolls out Aidoc across 28 hospitals | Enterprise AI is becoming IT + governance. Vendors without integration depth will be disintermediated. | HealthCareNow / Aidoc PR |

| 2026-02-18 | Median appoints U.S. president for eyonis LCS (UPDATE) | Lung AI competition shifts to distribution and screening workflow capture (not “who cleared first”). | Company PR |

| 2026-02-17 | Medtronic: first U.S. commercial Hugo case | Surgical robotics race intensifies; imaging vendors should position around perioperative imaging pathways and analytics. | Medtronic / MedTech Dive |

| 2026-02-18 | Danaher to acquire Masimo (~$9.9B) | Danaher’s diagnostics portfolio expansion (Masimo alongside Radiometer, Leica, Cepheid, Beckman Coulter) reinforces the trend of large platforms controlling hospital procurement relationships, which means imaging AI vendors increasingly compete for IT budget share against platform incumbents that bundle monitoring, diagnostics, and workflow. | Danaher IR / WSJ |

| 2026-02-19 | Provider-based compliance reminder: NPIs/attestations by 2028 | Hidden reimbursement risk sits in site-of-service attribution mechanics; imaging operators should audit off-campus departments now. | Foley article |

| 2026-02-18 | Banner adds 49 robotic surgery systems | Capex remains available for “platform” categories; expect higher bar for imaging ROI narratives in budget season. | Becker’s |

*The primary endpoint (interval cancer rate) published in The Lancet appears to have dropped around January 30–February 1, with the ScreenPoint press release on January 30.

INNOVATION HOOK

The highest-quality “innovation signal” this week isn’t a new model—it’s a workflow outcome. MASAI’s final readout supports an operating model shift in screening: AI-supported single reading that materially reduces human reading workload while maintaining comparable performance. That creates direct capacity headroom in a constrained radiologist labor market, and it reframes adoption decisions around throughput economics (studies per FTE) rather than incremental accuracy metrics alone.

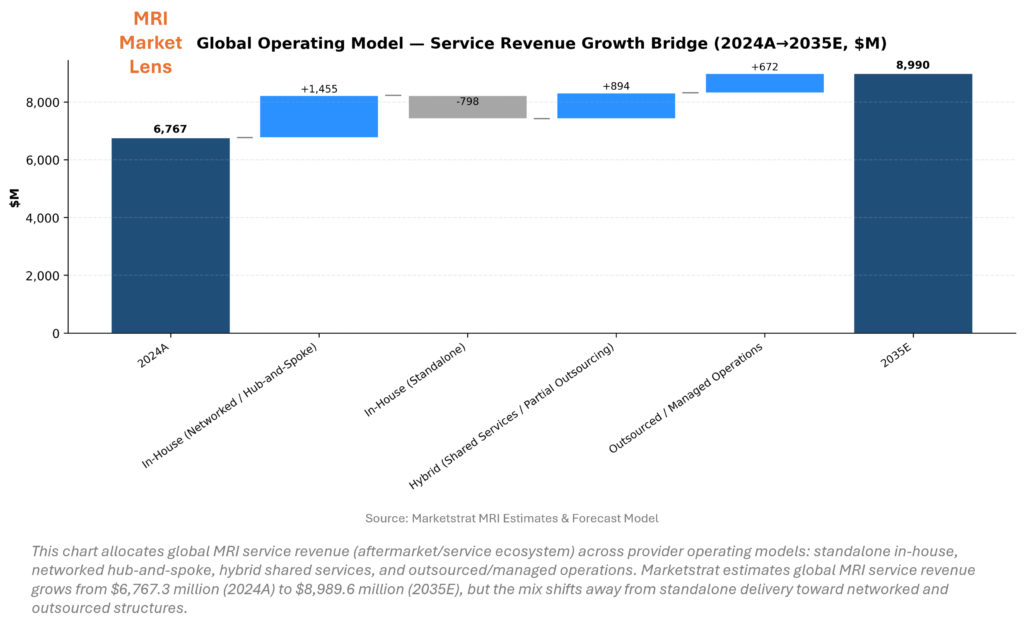

MARKET LENS — GLOBAL MRI MARKET BY OPERATING MODEL MIX

MRI service revenue grows from $6,767.3 million (2024A) to $8,989.6 million (2035E), but the underlying operating structure shifts away from standalone delivery toward networked, hybrid, and outsourced constructs. This reflects a structural operating reality: multi-site systems increasingly treat MRI as a managed fleet requiring standardized protocols, KPI governance, shared staffing pools, and centralized monitoring—especially as outpatient footprints expand.

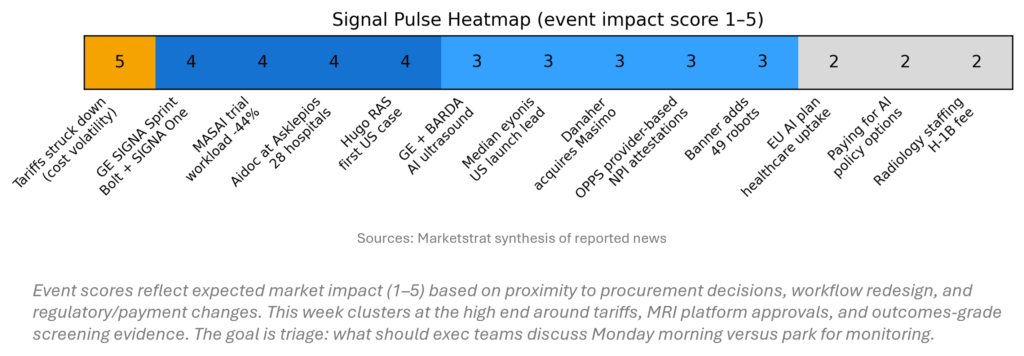

SIGNAL PULSE HEATMAP — FEB 14-20, 2026

The heatmap prioritizes events most likely to affect budgets, procurement timing, and workflow decisions in the next 1–2 quarters. This week’s highest-signal items sit in policy and platform lanes: tariff authority (cost volatility), MRI platform clearances (capacity economics), and enterprise AI distribution (multi-hospital rollouts). Lower-scoring items remain important but are less likely to force near-term decision cycles without follow-on data or formal rulemaking.

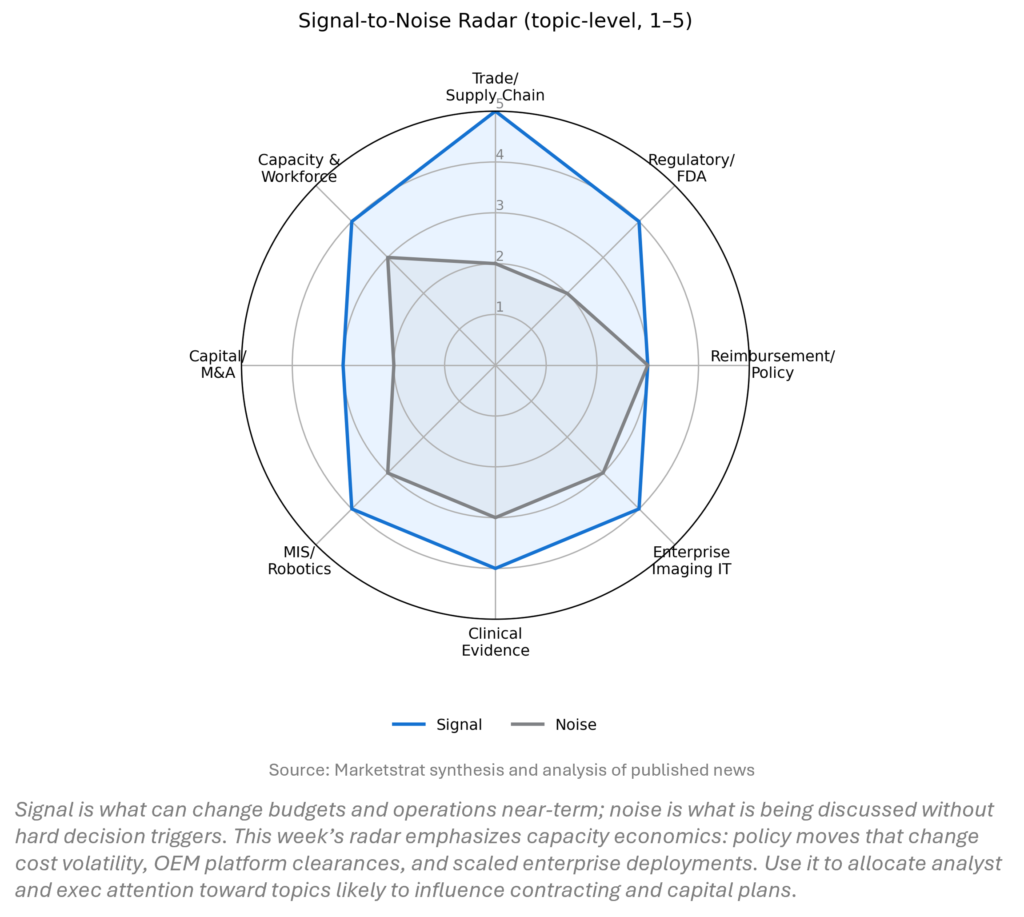

SIGNAL NOISE RADAR — FEB 14-20, 2026

The radar separates “high signal” topic lanes from areas dominated by narrative noise. This week, trade/supply chain and OEM platform economics are high-signal due to the policy move and MRI clearances. Enterprise imaging AI also trends high-signal because deployments are scaling beyond pilots. Reimbursement remains medium-signal/high-noise absent a new CMS rule, while governance/liability remains a steady, high-signal background theme as AI distribution widens.

REGULATORY PULSE

RegPulse remains the “velocity monitor” for radiology AI commercialization. This week’s update reflects newly identified clearances in the MRI platform/software lane, increasing 2026 YTD counts versus the prior baseline. The strategic point: regulatory activity is not only rising in classic standalone AI apps; it is shifting toward embedded workflow and modality software features that are easier to distribute and govern at scale inside enterprise environments.

MARKETSTRAT POV

- Providers: Treat AI adoption as a capacity plan, not a tech experiment—tie every algorithm deployment to measurable throughput KPIs (reading minutes saved, backlog reduction, scanner uptime), and redesign screening workflows around evidence like MASAI’s workload reduction rather than waiting for perfect reimbursement clarity.

- OEMs: Win on installability + serviceability + uptime guarantees. Use the post-tariff-volatility moment to shift contracting from “hardware discounts” to “capacity outcomes” (uptime SLAs, install cycle time, workflow software utilization) as differentiated value.

- AI vendors: Sell enterprise-ready packaging (integration, governance, monitoring) and prioritize distribution platforms (large health systems, consolidators, OEM channel partners). If you’re not inside the enterprise stack, you’ll compete on price and churn risk. Asklepios/Aidoc is the playbook, not the exception.

- Payers: Push the market toward outcomes-based adoption by requiring pre-specified performance + utilization guardrails; payment experiments should be structured to avoid runaway utilization while rewarding access and workflow efficiency. BPC’s map of options is directionally right—but execution will be local and contract-driven.

- MIS stakeholders: Robotics expansion is accelerating; imaging leaders should package perioperative imaging + analytics as an integrated pathway offering, not “adjacent services,” to win in the same capex decision cycles that are funding robot fleets.

Sources & Methodology

- Proprietary Data: Marketstrat Frameworks, Data Models, and Regulatory Pulse Tracker (Data through Feb 20, 2026).

- Market Intelligence: Broker Research, Expert Transcripts, and Filings via AlphaSense.

- Trade Reporting

- Analysis: Marketstrat Research & Synthesis.

About Marketstrat

Marketstrat® is a market intelligence and GTM enablement firm committed to empowering clients in data-driven industries. Under the Markintel™ brand, it delivers robust market intelligence, while GrowthEngine solutions offer specialized GTM advisory and app-based tools—together fueling growth, innovation, and competitive advantage. For more information, visit www.marketstrat.com.

Marketstrat® is a registered trademark and Markintel™ is a pending trademark of Marketstrat.

Check out free Research and Insights and Analysis of Industry Events

Check out our collection of Markintel Horizon and Markintel Pulse research.

Check out details on our reports, World Market for AI in Medical Imaging World Market for Oncology Imaging AI and other Pulse Reports in the Imaging space.