Individual License: $4,950 | Team and Enterprise License Options Available

This Horizon report is Marketstrat’s in-depth global analysis of the ultrasound market and broader ultrasound ecosystem — built for ultrasound OEM executives, strategy and corporate development teams, services / aftermarket leaders, providers, investors, and AI/workflow vendors adjacent to imaging. The report integrates ultrasound hardware, installed-base economics, service / aftermarket revenue, core AI recurring revenue, the broader AI bridge, market-structure views, competitive architecture, and strategic frameworks into one reconciled decision model.

Unlike conventional ultrasound reports that treat AI as an add-on chapter, this report treats AI as a first-class commercialization layer across acquisition guidance, reporting, quantification, cloud orchestration, enterprise governance, and recurring monetization. The goal is not just to describe the market — it is to explain where value is forming, how it is being monetized, how competition is reorganizing, and which commercial moves matter most over the next decade.

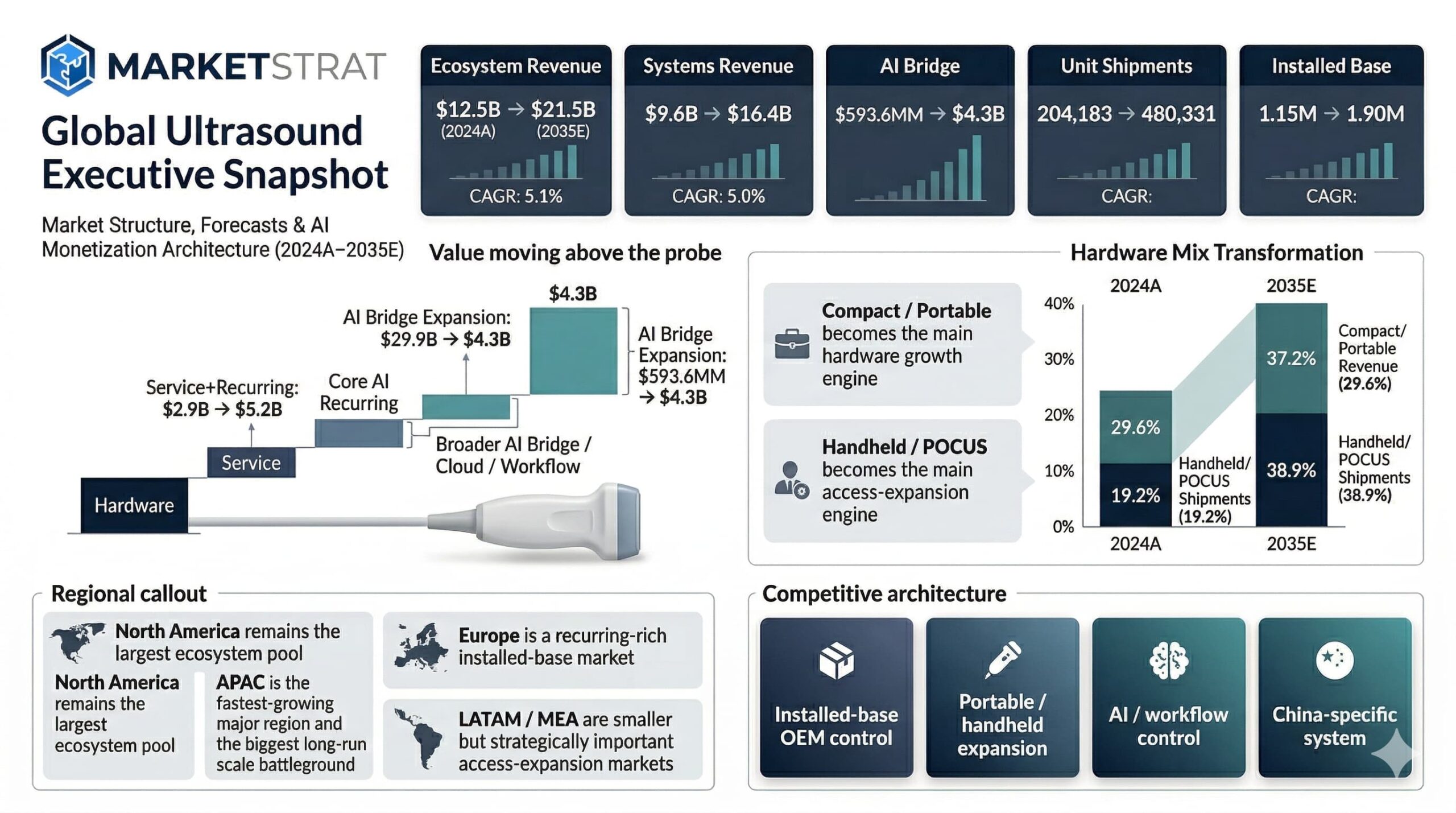

Ultrasound is broadening faster than it is premiumizing. World systems revenue rises from $9.6B in 2024A to $16.4B in 2035E, while annual shipments increase from 204,183 to 480,331 units and installed base expands from 1.15M to 1.90M units. That means the market is adding many more devices into many more settings than a simple topline revenue view suggests.

The more important structural shift sits above hardware. Total ecosystem revenue grows from $12.5B to $21.5B, while service + core AI recurring rises from $2.9B to $5.2B and the broader AI bridge expands from $593.6MM to $4.3B. In other words, the next value pool is increasingly tied to workflow, reporting, governance, cloud review, and software-linked operating leverage rather than to hardware ASP alone.

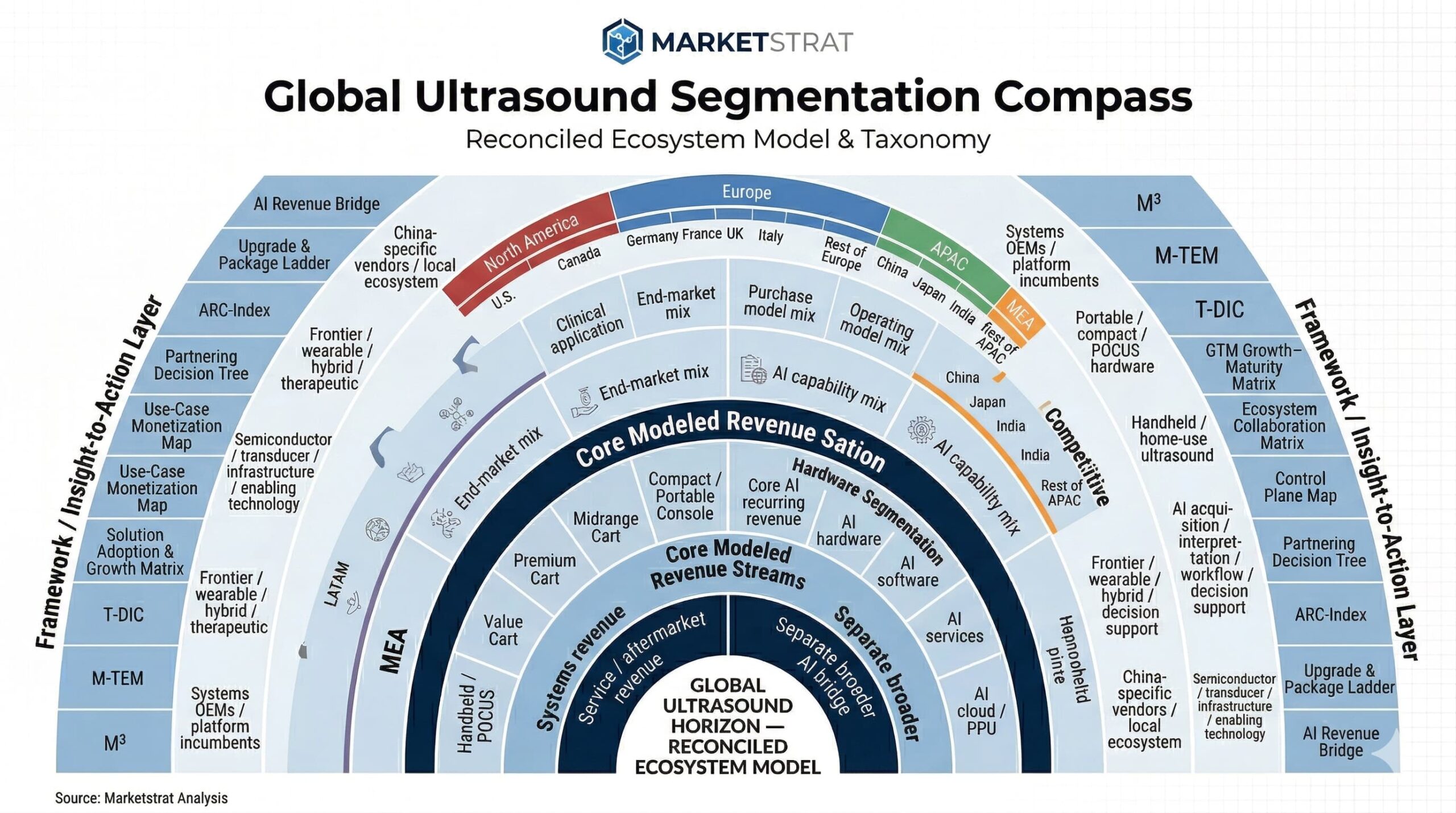

Market Segmentation

Core Ultrasound Segmentation Schema (2024A, 2035E, CAGR)

Market Structure Segmentation (2024A, 2035E, CAGR)