CMS coding, provider-IT rails, and MRI resilience reset the imaging AI stack

ONE BIG THING

This week’s most important shift was that imaging AI moved another step away from “interesting software” and toward operational infrastructure. CMS published HCPCS G0680 (effective April 1) for software analysis of coronary artery calcium and aortic valve calcification from chest CT; Infosys deepened the provider-IT implementation layer through Optimum Healthcare IT and Stratus; and helium disruption kept MRI uptime, refill exposure, and resilience in procurement math.

The commercial read-through is clear: enterprise buyers are underwriting billability, routability, implementation capacity, and uptime — not just model accuracy. That favors platform owners, services integrators, and OEMs with resilient architectures over stand-alone point solutions.

KEY TAKEAWAYS

- CMS’s G0680 code is the week’s clearest commercialization unlock. It does not make chest-CT calcium analysis clinically new, but it makes the workflow materially easier to route through outpatient operations.

- Medtronic’s Stealth AXiS clearance matters because it broadens a procedural ecosystem, not because it adds another isolated tool. Navigation, planning, and robotics continue to converge into multi-specialty platforms.

- Provider-IT distribution tightened again. Infosys buying Optimum and Stratus reinforces that implementation capacity is itself a control surface for healthcare AI deployment.

- Helium disruption kept MRI service continuity and total cost of ownership on the agenda. Low-helium and sealed-magnet logic now carry more boardroom relevance.

- Clinical evidence was useful but selective. The week favored pathway economics, specificity, and deployability over another headline sensitivity claim.

- The highest-value signals clustered where monetization clarity and deployment leverage intersected — not where research activity alone was highest.

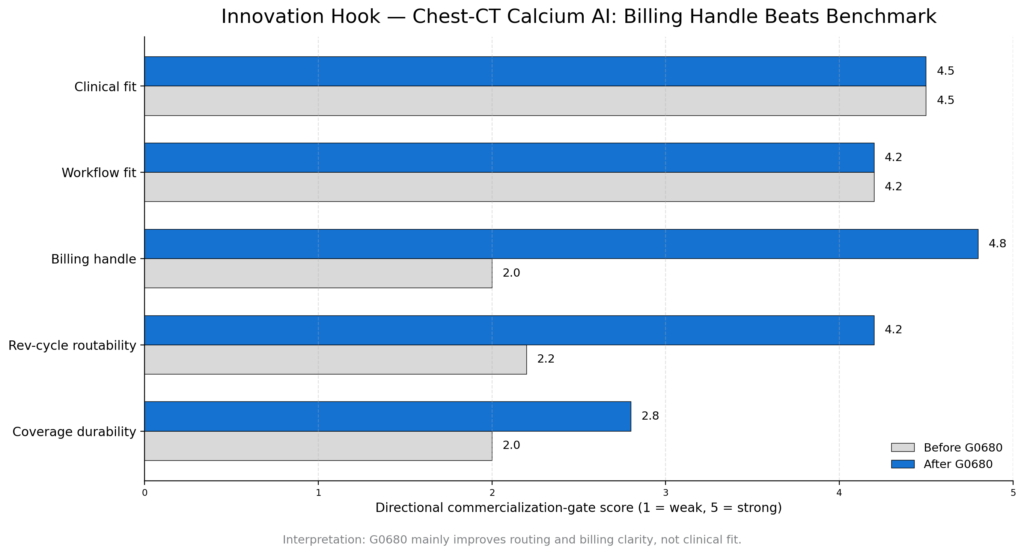

INNOVATION HOOK

The week’s most leverageable signal was not another AUC chart. It was a billing handle. G0680 does not change the clinical logic of chest-CT calcium analysis; it changes the internal economics of adoption by giving rev-cycle teams and service-line leaders something concrete to route.

That is the broader commercialization lesson for imaging AI: products clear the enterprise hurdle when clinical fit, workflow fit, billing clarity, and governance begin to align. This week, billing clarity improved first.

Sources: CMS OPPS transmittal; AAPC code summary; Marketstrat analysis

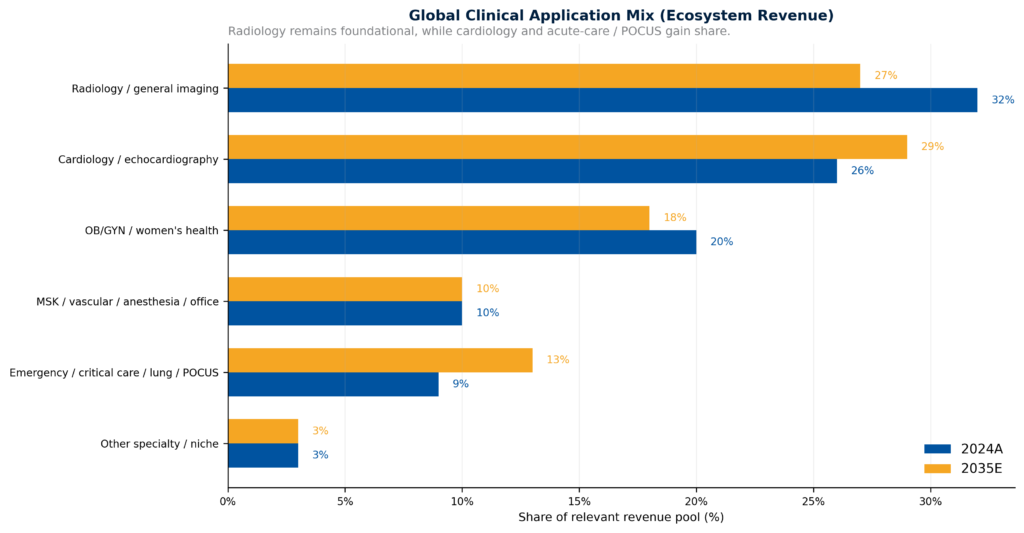

MARKET LENS – GLOBAL ULTRASOUND CLINICAL APPLICATION MIX

Radiology remains foundational, but the growth frontier is clearly no longer radiology-led alone. The practical implication is that cardiology and acute-care workflows should be treated as the two most commercially consequential application lanes for the next planning cycle, while women’s health remains a large but relatively more mature value pool.

Sources: Marketstrat Ultrasound Horizon Market Model.

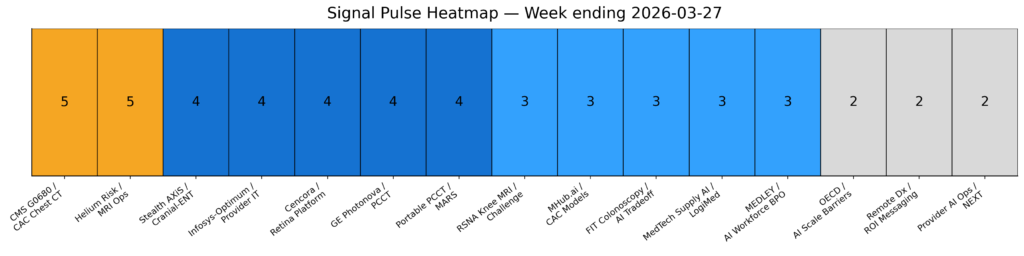

SIGNAL PULSE HEATMAP – MAR 21 – 27, 2026

Event-level

Two signals clearly sat at the top of the weekly stack: CMS G0680 and helium-driven MRI operating risk. Both matter because they affect enterprise behavior now, not only future optionality.

The next tier belonged to Medtronic, Infosys/Optimum, Cencora/EyeSouth, GE Photonova, and MARS. Lower-intensity items were valuable context setters but less likely to move near-term budget decisions on their own.

Sources: Marketstrat weekly scoring model.

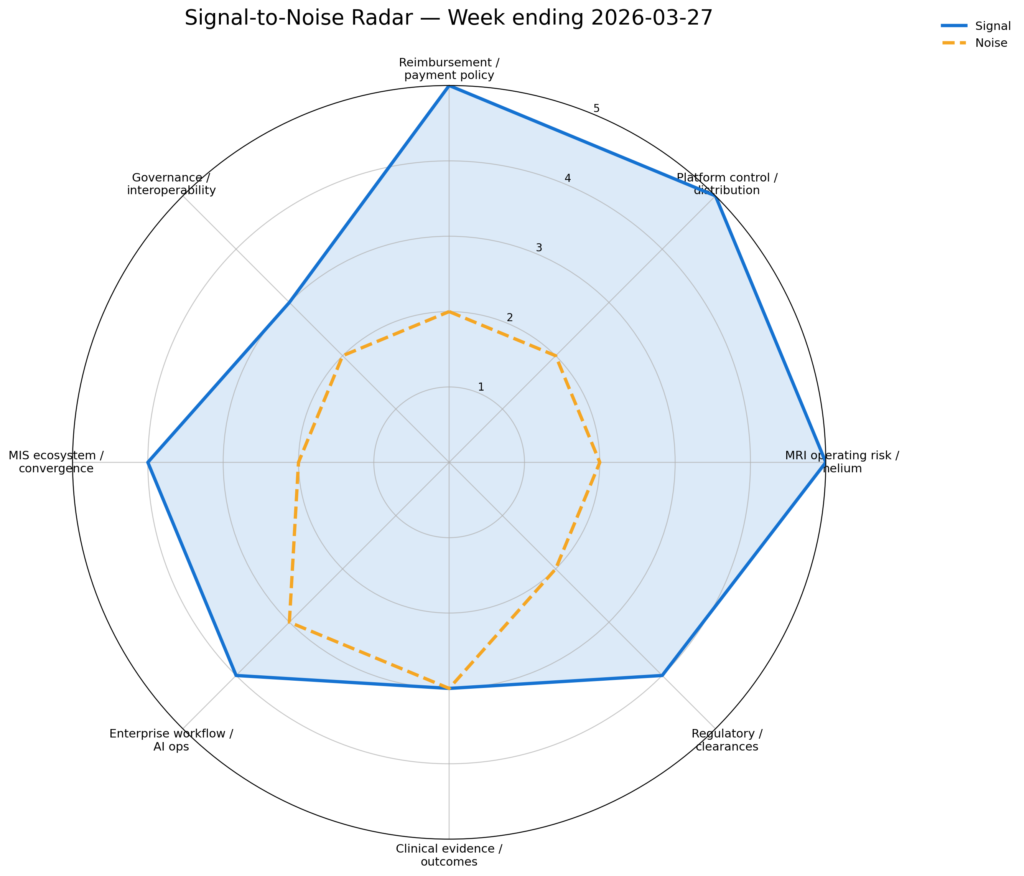

SIGNAL-TO-NOISE RADAR BY TOPIC – MARCH 21 – 27, 2026

The Radar shows where signal outran noise this week. Reimbursement, distribution control, and MRI operating risk were the cleanest areas of conviction.

Clinical evidence carried the highest relative noise because the evidence flow was more nuanced and pathway-specific than overtly directional for adoption.

Sources: Marketstrat weekly signal-to-noise scoring.

QUICK-GLANCE TABLE

| Signal | What happened | Strategic read | Score |

| CMS G0680 | CMS created an outpatient billing handle for software-based coronary and aortic valve calcium analysis from chest CT. | Turns opportunistic CT AI into a more routable rev-cycle workflow. | 5 |

| Helium / MRI | Qatar-related disruption and supplier reallocation kept helium pricing and MRI refill exposure live. | Resilience and TCO matter more in MRI procurement. | 5 |

| Medtronic | Stealth AXiS gained FDA clearance for cranial and ENT procedures. | Platform breadth in imaging-guided surgery continues to widen. | 4 |

| Infosys / Optimum / Stratus | Infosys agreed to acquire Optimum Healthcare IT and Stratus Global for a combined $560 million, moving deeper into provider IT and workflow implementation rails. | Healthcare AI scale often rides on services and operating-model capacity. | 4 |

| GE Photonova + MARS | GE advanced premium CT at the high end while MARS pushed portable photon-counting CT toward point-of-care workflows. | PCCT competition is spreading across both flagship and decentralized settings. | 4 |

| Cencora / EyeSouth | Cencora agreed to buy EyeSouth’s retina business for $1.1B. | Specialty-provider platforms remain powerful commercial chokepoints. | 4 |

| RSNA + MHub + FIT | Research signals highlighted better infrastructure, better standardization, and more nuanced pathway economics. | Evidence still matters — but only when it improves deployable economics. | 3 |

About Marketstrat

Marketstrat® is an independent market intelligence and advisory firm focused on MedTech, medical imaging and AI-enabled healthcare. Guided by its Markintel™ methodology, Marketstrat publishes specialized research and briefings, and provides custom research and advisory work that help leaders evaluate market opportunity, track competitive, regulatory, and evidence shifts, and make sharper strategy, product, and commercialization decisions.

Marketstrat® and Markintel™ are trademarks of Marketstrat Inc. All other trademarks are the property of their respective owners.