Capital, OEM strategy, provider consolidation, and procedural imaging are shifting the market from point algorithms to operating platforms.

🎧 Listen to this week’s Marketstrat Pulse Insight:

This week’s Marketstrat | Pulse Insights points to a sharper imaging AI market. Aidoc’s $150 million financing, GE HealthCare’s Advanced Imaging Solutions reorganization, RadNet’s Idaho imaging joint venture, Abbott’s Ultreon 3.0 clearance, and payer prior authorization standardization all reinforce the same thesis: imaging AI value is shifting from detection alone toward workflow control, economic proof, and platform-level deployment across the imaging journey.

Imaging AI’s next moat is not the number of algorithms in the portfolio. It is control of the workflow surface where clinical and economic decisions actually happen.

The market is moving beyond the algorithm

Imaging AI is entering a more disciplined phase.

For much of the category’s early commercial life, the conversation centered on whether algorithms could detect, segment, triage, or quantify better than the status quo. That question still matters. But it is no longer enough.

The stronger market question is now more operational: can the platform reduce friction, improve reporting, support follow-up, expand throughput, or change the economics of care delivery?

This week’s Pulse Insights shows that shift across several fronts. Capital is moving toward enterprise AI infrastructure. OEMs are bundling scanners, workflow, and enterprise imaging more tightly. Provider platforms are gaining more control over imaging access and downstream care coordination. Procedural imaging is moving closer to the moment of clinical decision-making.

The short version: imaging AI’s moat is shifting from model performance to workflow ownership.

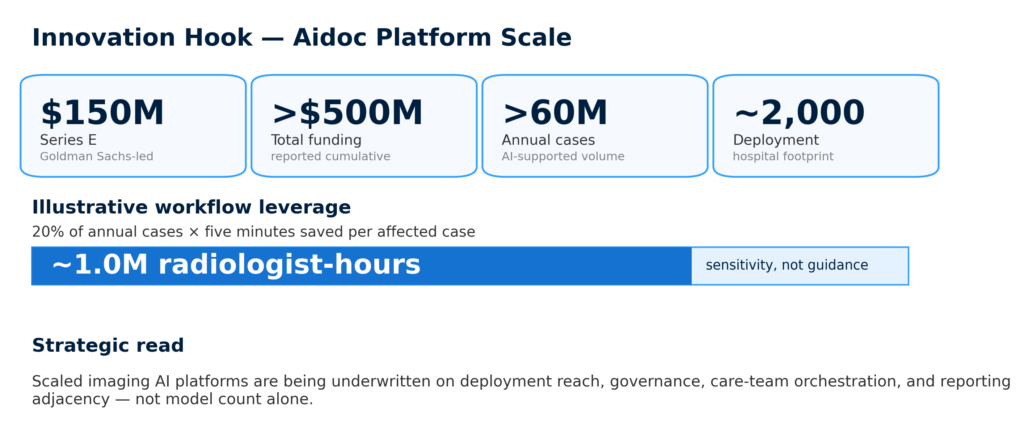

Aidoc resets the platform bar

Aidoc’s $150 million Series E was the week’s highest-signal AI event. The financing supports the company’s broader CARE foundation model, aiOS platform, deployment footprint, and automated draft-reporting roadmap.

That matters because Aidoc is not positioning around one narrow use case. The company is moving toward a broader operating layer for clinical AI across triage, orchestration, reporting adjacency, and enterprise deployment.

For health systems, this changes the buying frame. A point solution may still be valuable, but procurement committees are increasingly looking for platforms that reduce integration burden and deliver measurable workflow returns.

For AI vendors, the implication is more challenging. Technical performance remains necessary, but defensibility will depend on distribution, workflow embedding, governance, evidence, and integration with reporting or care coordination surfaces.

Aidoc’s financing highlights the move from point AI tools to enterprise clinical AI infrastructure.

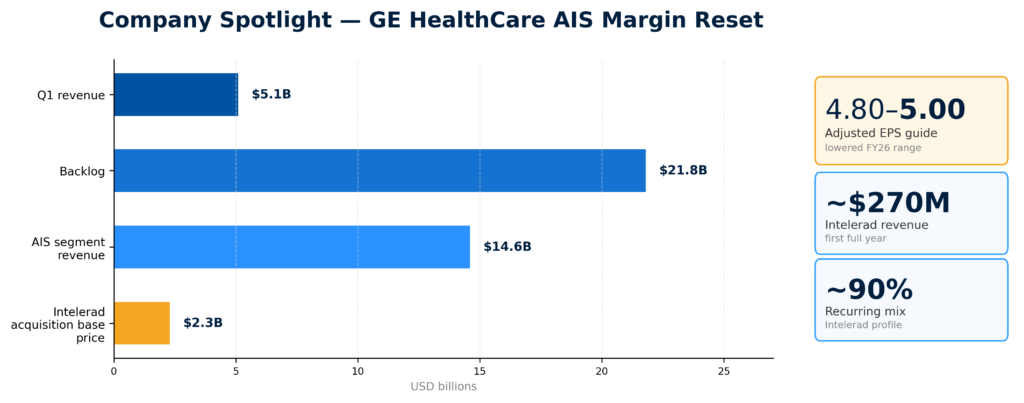

OEMs are building stacks under margin pressure

GE HealthCare Technologies Inc. (Nasdaq: GEHC) also generated one of the week’s most important signals. The company created Advanced Imaging Solutions, a new segment that combines imaging, advanced visualization, ultrasound, image-guided therapy, enterprise imaging, and related assets.

Strategically, the move is logical. Imaging buyers increasingly want integrated scanner-to-workflow solutions, not fragmented software layers. GEHC’s Intelerad acquisition becomes more strategically visible in this structure, linking enterprise imaging and diagnostic viewing more closely to the modality business.

But the same week also showed the pressure side of the story. GEHC lowered FY26 guidance and pointed to cost dynamics involving tariffs, supplier issues, freight, memory, oil, and other inflation factors.

That pairing matters. OEMs are trying to move up the software and workflow stack while defending margin. For buyers, that could mean more bundled offers. For competitors, it raises the premium on workflow attach, installed-base leverage, and service economics.

GEHC’s AIS reorganization shows the scanner-to-software strategy, while margin pressure shows why operating leverage matters.

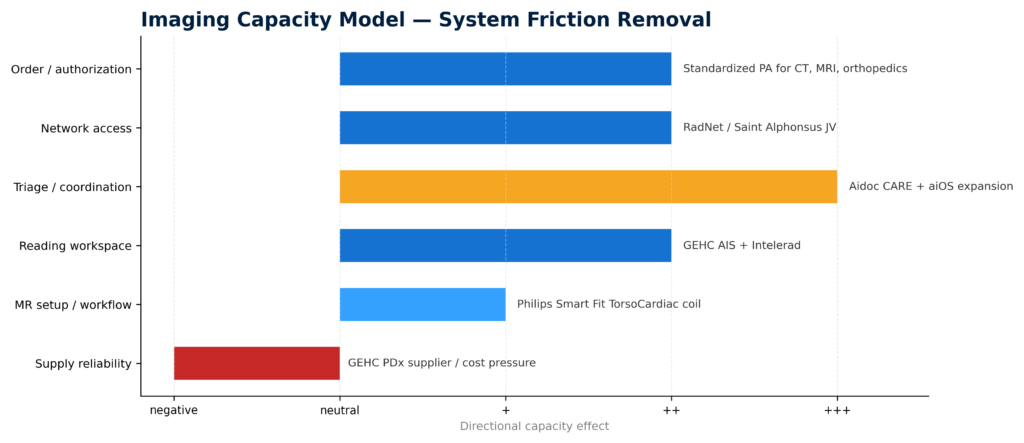

Distribution control is moving upstream

The provider side of the market is also shifting. RadNet Inc. (Nasdaq: RDNT) and Saint Alphonsus formed a joint venture in Idaho around Intermountain Medical Imaging. The transaction expands RadNet’s health-system-aligned outpatient imaging model and creates a regional surface for software and AI deployment through DeepHealth.

Azra AI’s acquisition of Thynk Health points to a different but related control point: oncology workflow. The combination brings together incidental findings, lung screening, report mining, and care navigation infrastructure.

These developments point to a broader strategic pattern. The economic value of imaging increasingly sits around the scan, not only inside the scan. Referral capture, scheduling, follow-up closure, oncology navigation, reporting workflow, and site-of-care routing are all becoming more important.

Platforms that own those control points may capture more durable value than vendors selling tools into disconnected workflows.

Procedural imaging is becoming a decision layer

This week also reinforced the imaging adjacency in minimally invasive surgery and procedural care.

Abbott Laboratories (NYSE: ABT) received FDA clearance and CE Mark for Ultreon 3.0, its AI-powered coronary OCT platform. Medtronic plc (NYSE: MDT) received CE Mark for Stealth AXiS, bringing planning, navigation, and robotics further into a platform configuration. Olympus Corporation (Tokyo Stock Exchange: 7733) and Canon Inc. (Tokyo Stock Exchange: 7751), through Canon Medical, introduced the Aplio i800 EUS premium ultrasound system in the United States.

These are not identical markets, but the strategic theme is consistent. Imaging is moving from diagnostic support into procedural execution.

In PCI, surgical navigation, endoscopic ultrasound, hyperspectral imaging, fluorescence-guided surgery, and intraoperative margin assessment, the competitive question is increasingly: what can the platform see, quantify, guide, or decide in real time?

Imaging capacity is shaped by workflow, prior authorization, AI orchestration, network access, and MR setup.

Why this matters

For providers, the bar for AI adoption should be operating impact. That means measuring turnaround time, reporting burden, follow-up closure, avoided handoffs, throughput, denial friction, or downstream pathway performance.

For vendors, the priority is packaging. Tools that cannot integrate into the clinical work surface will struggle against platforms that offer broader workflow value.

For investors and strategics, platform quality is becoming easier to distinguish. The strongest assets are likely to combine evidence, workflow adjacency, deployment scale, reimbursement relevance, and channel control.

Marketstrat POV

The next phase of imaging AI will be less forgiving.

The market will still reward strong technology, but it will increasingly penalize tools that do not fit into real operating models. The commercial premium is moving toward platforms that can reduce friction and own the workflow surface from scan acquisition through reporting, routing, follow-up, or procedure guidance.

The practical takeaway: the best-positioned imaging AI companies will not simply detect more findings. They will change where work happens, how fast it moves, and who controls the economics around it.

Subscribe to The Marketstrat Pulse for weekly intelligence on medical imaging AI, enterprise imaging, reimbursement, medtech strategy, and image-guided care: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

Related research themes

- Medical imaging AI commercialization

- Enterprise imaging and imaging IT platforms

- Imaging reimbursement and prior authorization

- Radiology workflow and throughput

- Image-guided minimally invasive surgery

- OEM software strategy and installed-base economics

- Provider consolidation and outpatient imaging platforms

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.