GE, Siemens, RadNet, Fujifilm, AGFA, Viz.ai, Lumexa, and CMS show how imaging value is moving into uptime, workflow, authorization, and utilization economics.

The most important imaging AI signals this week were not isolated algorithms. They were operating-stack signals. MRI uptime, interventional acquisition, outpatient slot capacity, enterprise imaging, prior authorization, and procedure workflow all moved into focus. Marketstrat’s read: imaging AI is becoming less about model count and more about measurable capacity, integration, governance, and commercial control.

🎧 Listen to this week’s Marketstrat Pulse Insight:

The operating layer is becoming the moat

Medical imaging AI is entering a more demanding commercial phase. The question is no longer whether algorithms can improve detection, triage, quantification, or workflow. Many can.

The more important question is whether they can improve the operating system around imaging.

That operating system includes scanner uptime, acquisition workflow, technologist productivity, exam scheduling, enterprise image access, prior authorization, follow-up routing, procedure-room utilization, and AI governance.

This week’s strongest signals pointed in that direction. GE HealthCare and Siemens Healthineers pushed AI deeper into modality and acquisition infrastructure. RadNet showed a capacity metric that ties AI directly to scan throughput. Fujifilm and AGFA reinforced enterprise imaging as a platform-control layer. Viz.ai moved pulmonary AI toward disease-pathway orchestration. CMS continued to turn prior authorization into an API-enabled implementation issue.

The implication is clear: imaging AI is shifting from model proof to capacity control.

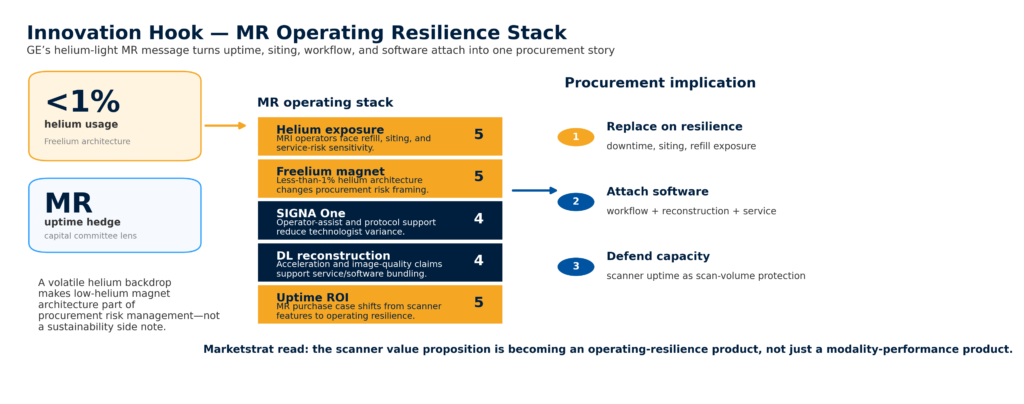

Marketstrat visual showing MRI operating resilience across helium exposure, uptime, siting flexibility, workflow automation, and software attach.

MRI is becoming an operating-resilience category, with uptime, helium exposure, siting, and AI workflow entering the procurement case.

MR is now an uptime and resilience category

GE HealthCare’s ISMRM announcements framed MRI around more than field strength, image quality, or scanner features. SIGNA Sprint with Freelium, SIGNA Bolt, and SIGNA One were packaged into a broader workflow and resilience narrative: helium-light architecture, siting flexibility, deep-learning workflow, and operator support.

The helium element is commercially important. MRI economics depend on uptime, service reliability, refill exposure, installation constraints, and total cost of ownership. A lower-helium architecture becomes more than a sustainability claim when helium availability and pricing remain strategic concerns.

Marketstrat’s read is that MR procurement is being reframed. The next wave of scanner differentiation will combine imaging performance with operating resilience. OEMs that can connect magnet architecture, workflow AI, service economics, and siting flexibility have a stronger capital-committee story than vendors selling scanner specifications alone.

Interventional imaging AI is moving closer to the live procedure

Siemens Healthineers received FDA clearance for six Artis interventional imaging systems with Optiq AI. That matters because it places AI closer to the live acquisition chain in image-guided therapy.

This is not a generic AI interpretation story. It is a procedure-room productivity story. AI-supported interventional imaging can be positioned around dose optimization, image consistency, procedural confidence, and lab efficiency.

For hospitals, the replacement-cycle argument becomes more operational. For Siemens, it strengthens the interventional imaging portfolio at a moment when buyers are looking for capital equipment that can defend both clinical performance and workflow economics.

Outpatient imaging scale is becoming a software-and-capacity story

RadNet’s Q1 update was the clearest operating leverage signal of the week. The company reported strong growth in advanced imaging volume and continued progress in Digital Health ARR. More important for the broader imaging AI market, it highlighted a concrete workflow metric: C-MODE thyroid AI reduced ultrasound slot times from 30 minutes to 20 minutes across nearly 300 sites.

That type of metric matters because AI buyers increasingly need capacity proof.

A workflow that opens exam capacity without adding a new site, a new scanner, or incremental real estate is strategically meaningful. For outpatient imaging operators, that can translate into better utilization. For vendors, it supports a more credible ROI narrative. For investors, it links AI software to the economics of physical imaging distribution.

Lumexa’s four-center expansion added another distribution signal. Hospital-affiliated outpatient imaging continues to professionalize around joint ventures, de novo siting, and local referral capture. The strategic theme is not just center count. It is control over local access, referral density, modality mix, and operating workflow.

Enterprise imaging remains a control surface

Fujifilm’s Synapse partnership with Ardent and AGFA’s enterprise imaging go-live momentum reinforced that enterprise imaging is still a platform market.

Health systems are not simply replacing PACS. They are consolidating radiology, cardiology, image storage, diagnostic viewing, workflow execution, and cross-department access. That creates a higher bar for point solutions that cannot integrate into systemwide architecture.

The buyer need is straightforward: less fragmentation, fewer workflow switches, cleaner image access, and more consistent deployment execution. The commercial implication is tougher terrain for narrow tools that sit outside the enterprise imaging stack.

Viz.ai’s Pulmonary Suite added a disease-pathway layer to the same theme. Pulmonary AI is moving from finding abnormalities to managing follow-up, reducing leakage, and routing care across teams. That broadens the ROI conversation from radiology productivity to downstream program economics.

Prior authorization is becoming infrastructure

CMS’ electronic prior authorization initiative matters for imaging because advanced imaging, contrast-linked workflows, oncology pathways, and radiopharmaceutical-adjacent services all depend on documentation, payer approval, and scheduling certainty.

Digital prior authorization can reduce manual work, but it also makes payer rules more structured, data-driven, and enforceable. Providers should treat this as a workflow infrastructure issue, not only a compliance item.

Imaging groups should invest in authorization analytics, structured documentation, payer-specific denial tracking, and API readiness before payer systems gain the cleaner data advantage.

The imaging AI moat is moving from the model to the operating stack: uptime, capacity, authorization, workflow integration, governance, and procedure economics.

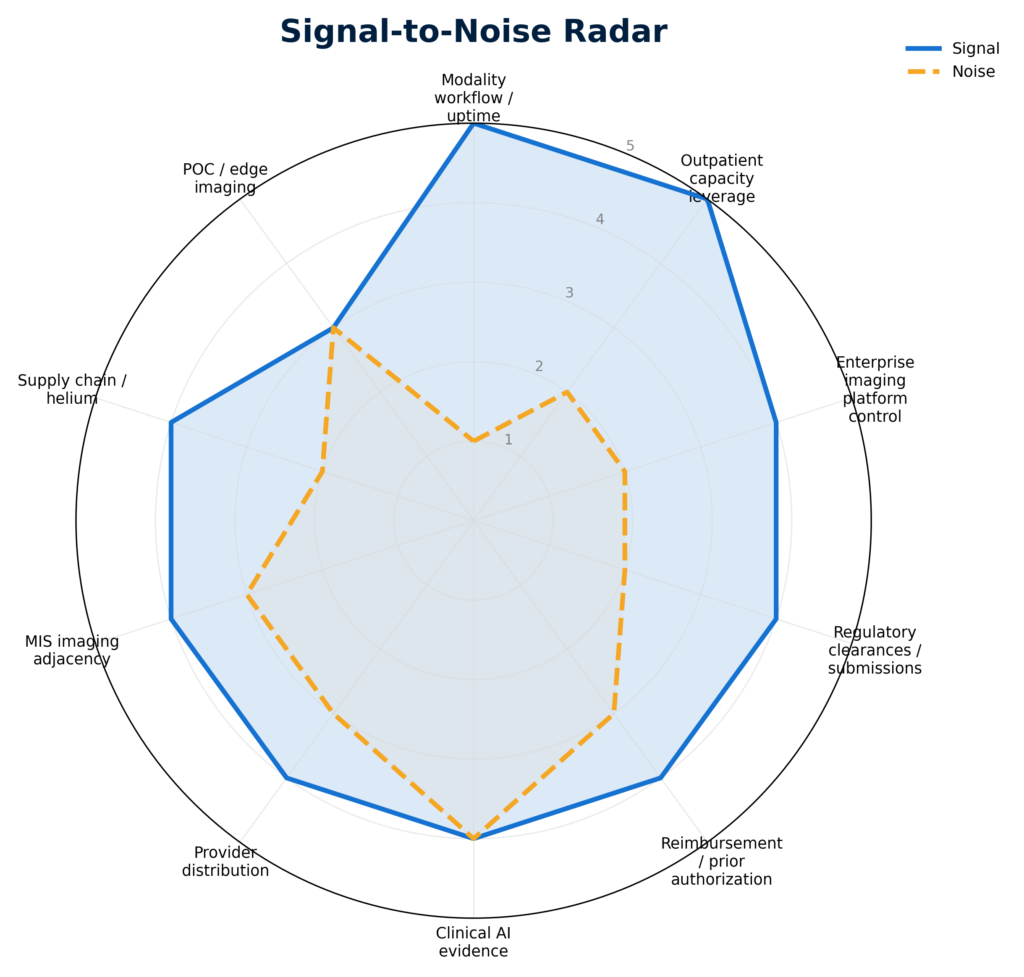

Marketstrat signal-to-noise radar for imaging AI and enterprise imaging market signals for week ending May 15, 2026.

The highest-conviction weekly signals clustered around modality workflow, outpatient capacity, enterprise imaging, regulatory activity, and supply-chain sensitivity.

What this means for providers, vendors, and investors

For providers, AI procurement should be tied to measurable operating impact: exam slots opened, downtime reduced, follow-up leakage closed, authorization touches removed, QA burden managed, or procedure-room utilization improved.

For vendors, model performance remains necessary but insufficient. The stronger commercial story is integration into enterprise imaging, modality workflow, revenue-cycle infrastructure, or specialty care pathways.

For investors and strategics, the highest-quality assets are likely to be those with workflow control, distribution access, governance infrastructure, or utilization leverage. Standalone algorithms without channel power or operating proof may face pricing pressure.

The market is not moving away from imaging AI. It is demanding that imaging AI behave like infrastructure.

CTA: Subscribe to The Marketstrat Pulse for weekly market intelligence across medical imaging AI, enterprise imaging IT, reimbursement, OEM strategy, provider consolidation, and image-guided procedure platforms: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

Related research themes

- Medical imaging AI commercialization

- Enterprise imaging IT and PACS/VNA consolidation

- MRI uptime, helium exposure, and scanner workflow

- Outpatient imaging access and provider distribution

- Prior authorization and revenue-cycle infrastructure

- Digital pathology and procedure-platform economics

- Image-guided minimally invasive procedures

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.