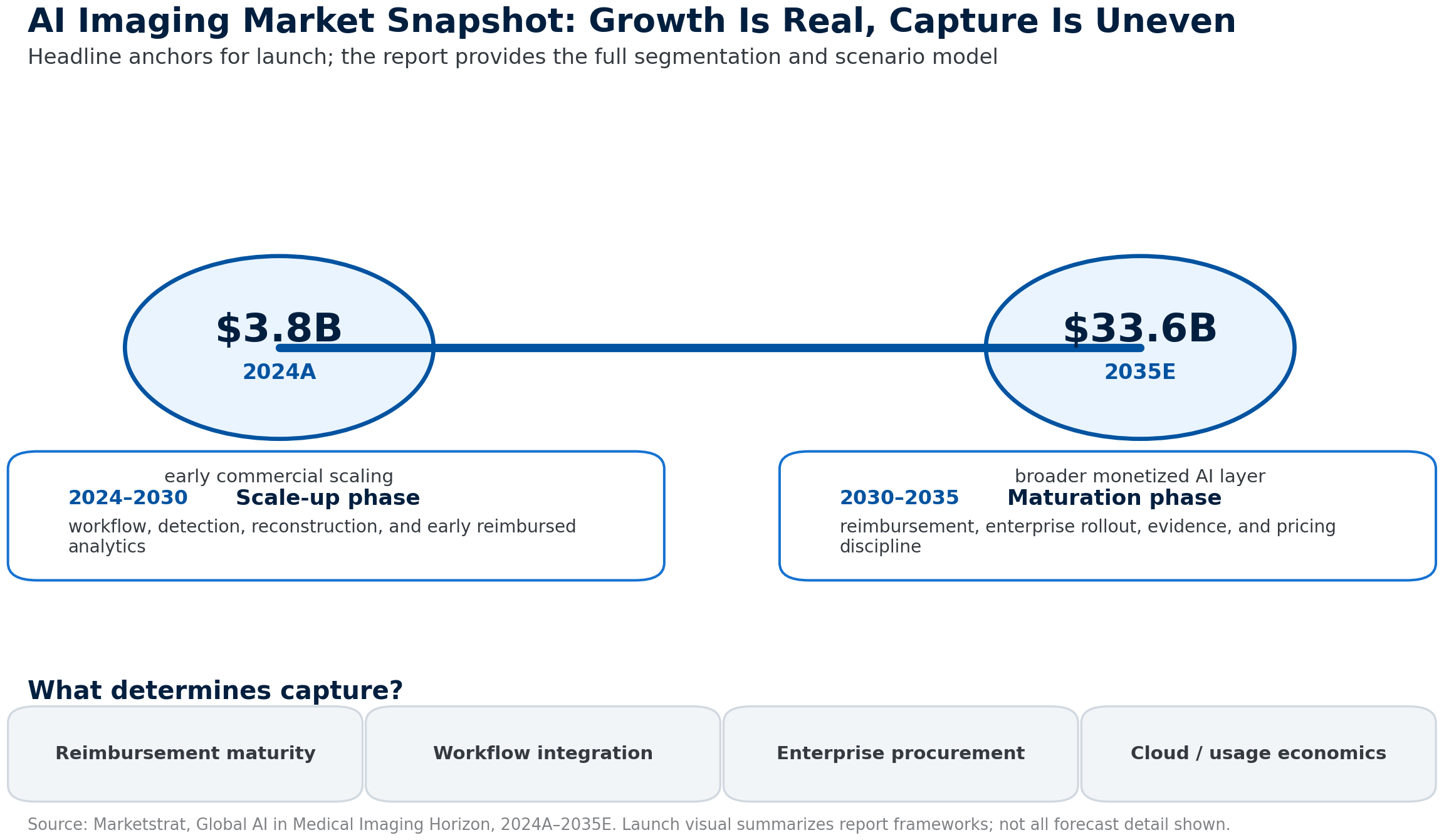

The report is built around a reconciled 2024A–2035E market model and covers the major commercial dimensions of medical imaging AI: modality, clinical area, clinical application, technology layer, revenue stream, end-user organization, geography, and reimbursement tier. The base-case forecast places the global AI medical imaging market at approximately $3.8B in 2024A and approximately $33.6B by 2035E, with growth shaped by reimbursement expansion, enterprise platform adoption, AI-enabled productivity, cloud deployment, and disease-specific quantitative analytics.

![]()

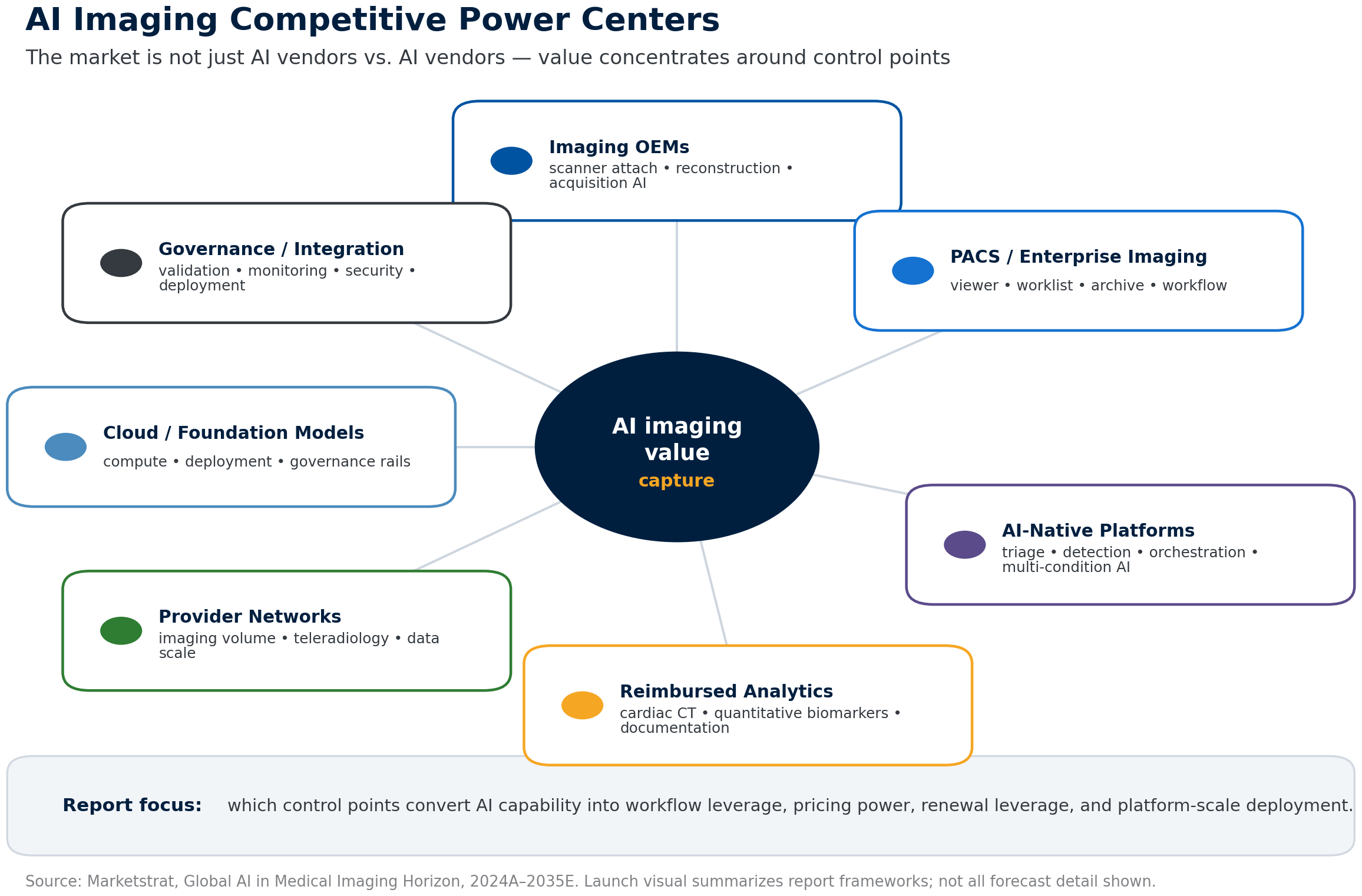

The AI medical imaging competitive landscape is consolidating around workflow control, enterprise integration, reimbursement leverage, and platform-scale distribution. The market is no longer best described as a fragmented population of algorithm developers. It is becoming a layered competitive system in which OEMs, enterprise imaging vendors, AI-native platforms, specialty analytics companies, cloud providers, and provider networks are all competing to control the deployment surface.

The report analyzes the competitive landscape across the major AI imaging control points, including imaging OEMs, enterprise imaging vendors, PACS / RIS / VNA platforms, AI-native clinical platforms, reimbursed quantitative analytics companies, breast and oncology AI vendors, reconstruction and acquisition AI companies, reporting and workflow automation vendors, AI orchestration / governance platforms, cloud infrastructure providers, and provider-network AI platforms.

Companies discussed include GE HealthCare, Siemens Healthineers, Philips, Canon Medical, Fujifilm, United Imaging, Pro Medicus, Sectra, Intelerad, AGFA HealthCare, Aidoc, Viz.ai, RapidAI, Qure.ai, Annalise.ai, DeepHealth / RadNet, HeartFlow, Cleerly, Elucid, Circle Cardiovascular Imaging, Lunit, iCAD, ScreenPoint, Hologic, Vara, Rad AI, Microsoft / Nuance, deepc, CARPL.ai, Ferrum Health, Blackford, Incepto, AWS, Microsoft Azure, Google Cloud, NVIDIA, and others.