The week ending June 12 showed imaging AI moving beyond point algorithms and into reporting workflow, enterprise imaging workspaces, validation infrastructure, and operational capacity.

This week’s Marketstrat Pulse points to a structural shift in imaging AI. The highest-signal activity was not another standalone detection model. It was the concentration of reporting-native AI, cloud enterprise imaging, validation infrastructure, device cyber resilience, and provider platform financing around the workflows that determine radiology productivity. DeepHealth, Rad AI, GE HealthCare, Siemens Healthineers, CARPL.ai, Enlitic and RadNet each advanced pieces of the new imaging control layer.

🎧 Listen to this week’s Marketstrat Pulse Insight:

The shift: from point algorithms to workflow control

Radiology AI is entering a more operational phase.

The first wave of imaging AI centered on detection, triage, and algorithm performance. Those capabilities remain important, but the commercial battleground is widening. The more durable question is now whether AI can sit inside the daily workflow of imaging organizations and release measurable capacity.

That is why the week ending June 12 was notable. The market’s strongest signals clustered around reporting-native AI, enterprise imaging workspaces, image exchange, data normalization, validation infrastructure, cybersecurity, and provider platform financing.

The common denominator is control of the workflow layer. In imaging, that layer sits between the scanner, the radiologist, the report, the referring physician, the payer, and the patient. It is where productivity is either created or lost.

Reporting AI becomes the highest-leverage surface

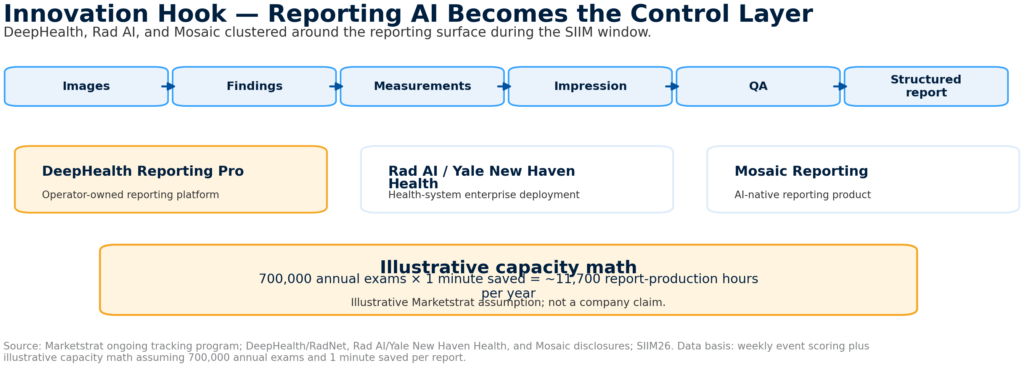

The week’s clearest signal came from radiology reporting.

DeepHealth, RadNet’s AI and health informatics subsidiary, launched Reporting Pro, an AI-assisted radiology reporting platform. Rad AI announced an enterprise deployment with Yale New Haven Health. Mosaic Clinical Technologies launched Mosaic Reporting, extending Radiology Partners’ internal workflow infrastructure into a product posture.

The strategic importance is not simply that these tools use AI to help write reports. It is that reporting is one of the few workflow layers that can touch most imaging exams across modalities and sites.

A pathology-specific detection model may deliver high clinical value, but it usually applies to a subset of exams. Reporting infrastructure can apply across the daily radiology production environment. That makes it a broader distribution surface and, potentially, a more attractive monetization layer.

The operational questions will be practical: does the platform reduce minutes per case, improve structured reporting, reduce addenda, support QA, and integrate cleanly into existing PACS, RIS, EHR, and dictation environments?

GE HealthCare pushes cloud enterprise imaging at SIIM

GE HealthCare used SIIM 2026 to reinforce the enterprise imaging workspace thesis, including Genesis Radiology Workspace and InteleShare.

That matters because enterprise imaging is moving beyond archive-and-viewer procurement. Health systems increasingly need platforms that support distributed reading, cloud access, image exchange, remote workflow, AI orchestration, and exception management.

The competitive implication is straightforward. Vendors that control the cloud workspace and the data-movement layer have a stronger position than vendors selling isolated applications. In an environment where radiology staffing remains constrained and imaging volumes continue to rise, workflow orchestration becomes a capacity tool, not just an IT upgrade.

Governance and validation move into the buying process

The CARPL.ai and Enlitic partnership highlights another underappreciated shift: validation infrastructure is becoming a commercial requirement.

Enterprise AI buyers do not only need access to algorithms. They need normalized imaging data, local validation, audit trails, performance monitoring, and governance workflows. Without those tools, imaging AI remains difficult to scale beyond pilots.

This is a critical market-development point. The buyer is not just evaluating whether an algorithm performs well in a published study. The buyer is asking whether the model performs safely in its own patient population, across its own scanners, protocols, sites, and workflows.

That pushes the market toward infrastructure. AI marketplaces, data-normalization platforms, validation environments, and monitoring tools will become more important as health systems move from experimentation to enterprise deployment.

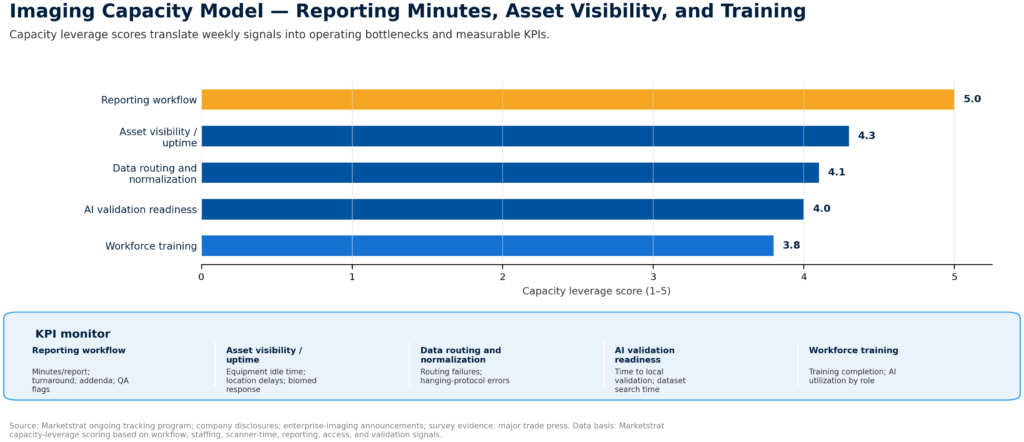

Capacity is no longer just scanner time

The week also showed that imaging capacity is becoming a multi-layer constraint.

Siemens Healthineers received an ARPA-H SHIELD contract focused on AI-enabled medical-device cyber resilience. GE HealthCare and Carilion expanded asset visibility and RTLS infrastructure. Philips’ Future Health Index added adoption evidence around AI productivity while highlighting inconsistent AI training.

These events point to a broader definition of capacity. Scanner availability still matters, but it is only one part of the operating system. Imaging organizations also need reliable devices, trained users, integrated workflows, clean data, validated AI tools, and reporting processes that do not create downstream friction.

For providers, this means AI procurement should be evaluated against measurable workflow outcomes. For vendors, it means product strategy must include implementation, training, validation, governance, and integration. For investors, it means distribution surfaces and workflow ownership may be more important than model count.

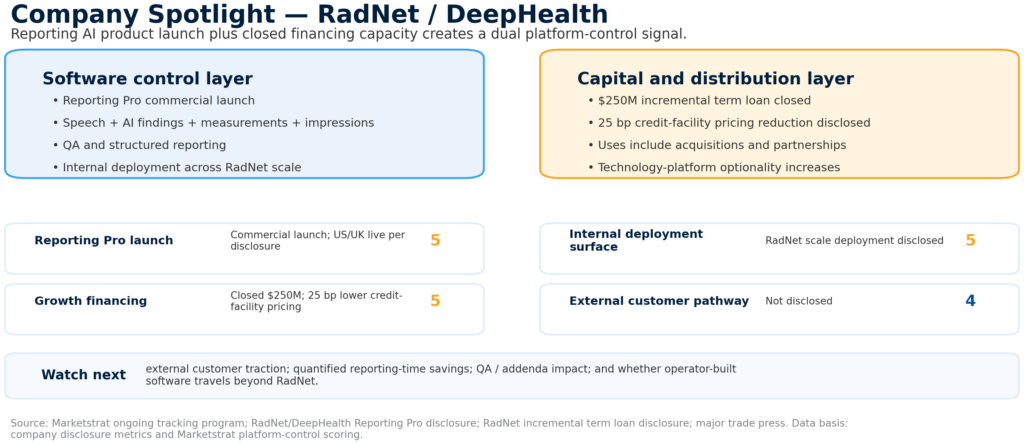

RadNet’s financing reinforces the platform thesis

RadNet’s $250 million incremental term loan was one of the week’s most important commercial signals.

The financing gives RadNet additional flexibility for acquisitions, organic expansion, health-system partnerships, technology platforms, and general corporate purposes. Paired with DeepHealth’s Reporting Pro launch, the signal is not just financial. It is strategic.

Scaled imaging operators can become deployment surfaces for software. They can test products internally, refine workflow, accumulate operational evidence, and then take those capabilities to external customers. That operator-plus-software model is still developing, but it deserves close attention.

Marketstrat POV

The next phase of imaging AI will be less about isolated algorithm wins and more about platform position.

The companies best positioned will be those that can prove workflow impact, deploy across enterprise environments, support governance, and reach high-volume clinical settings. That includes scaled imaging operators, enterprise imaging vendors, OEMs with installed-base leverage, and AI companies embedded in reporting and validation workflows.

The practical takeaway: imaging AI is becoming part of the operating infrastructure of radiology. The market will reward tools that reduce friction, protect capacity, and fit into the real economics of imaging delivery.

Subscribe to The Marketstrat Pulse for weekly analysis of medical imaging AI, enterprise imaging, nuclear medicine, reimbursement, provider-platform strategy, and image-guided procedure markets: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.