The global mammography market is structurally mature but strategically active. The gantry pool remains the anchor, yet the most important growth and competitive movement is occurring around the gantry: AI/workflow software, CEM-enabled diagnostic pathways, service retention, interventional breast procedures, breast ultrasound, breast MRI, mobile access infrastructure, and risk-based screening.

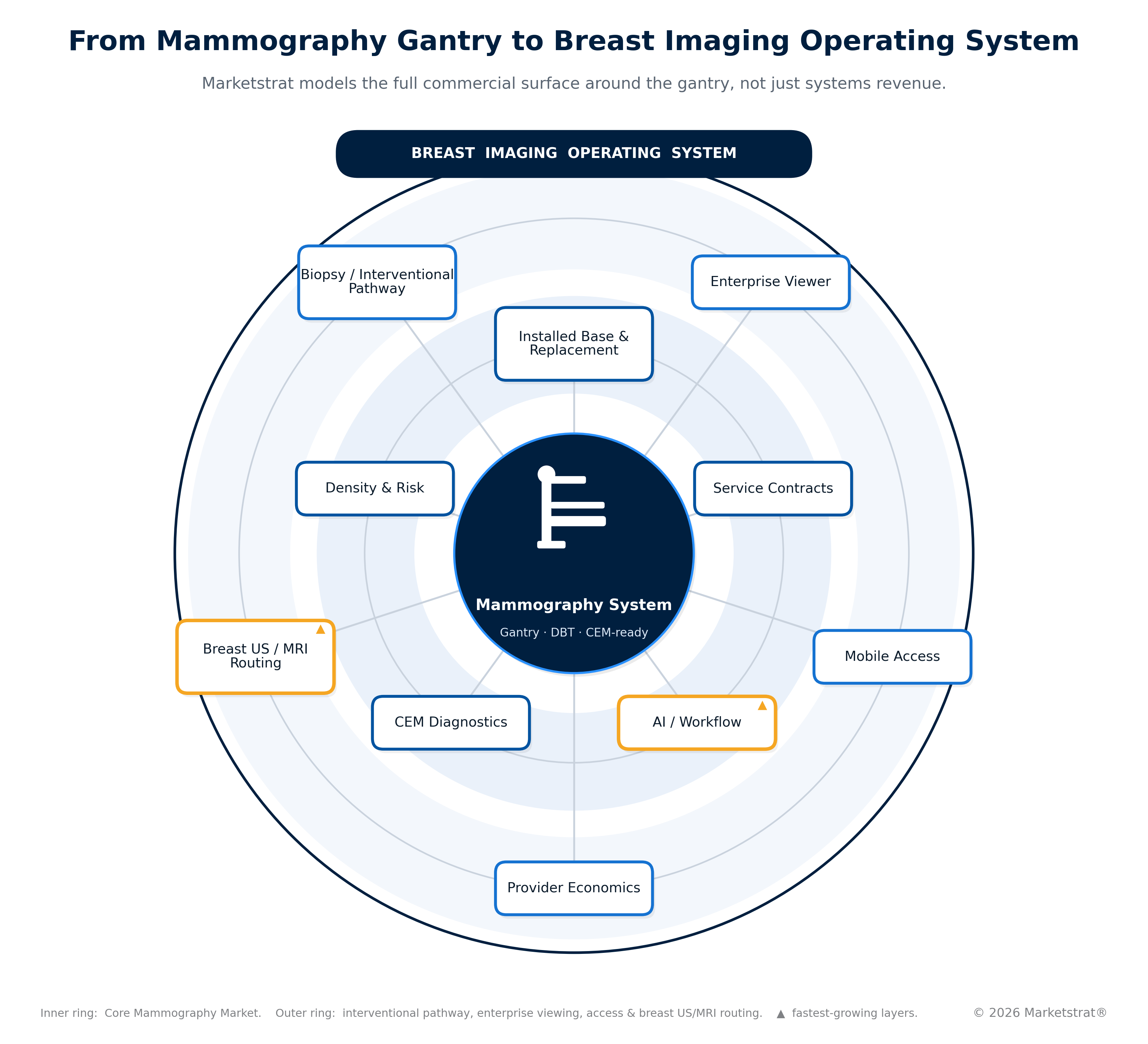

The report’s market architecture separates three layers:

Core Mammography Market

Dedicated mammography systems, mammography-specific service, mammography-specific software/workstations, and mammography AI/workflow.

Interventional Breast Pathway

Biopsy systems, localization, image-guided intervention, and related downstream procedure economics.

Breast Imaging Ecosystem Opportunity

The Core Mammography Market plus the Interventional Breast Pathway and breast ultrasound/MRI adjacencies.

This matters because a flat or modestly growing gantry market can still control a larger and faster-moving ecosystem. The report’s framework analysis shows equipment and service as stable, installed-base-heavy pools, while AI/workflow, CEM, breast ultrasound, breast MRI, and biopsy/intervention drive a broader strategic opportunity.

1. Mammography is shifting from hardware replacement to ecosystem control

The strongest competitors are not simply those with the most installed gantries. They are the companies that can defend replacement accounts, attach service, integrate AI and workflow, enable CEM, support biopsy pathways, and keep the breast imaging study inside their operating environment.

2. DBT is becoming baseline in developed markets

DBT remains strategically important, but in many developed markets it is increasingly a replacement-cycle and premium-standard feature rather than a greenfield growth story. Future differentiation shifts toward workflow, patient experience, AI integration, CEM readiness, dose, acquisition speed, service, and fleet economics.

3. CEM is the most important near-term premium technology overlay

Contrast-enhanced mammography is not yet a broad screening standard, but it is strategically important for dense-breast workup, diagnostic problem-solving, selected MRI-substitution use cases, CEM-guided biopsy, and premium breast-center positioning. The report treats CEM as a practical near-term overlay rather than a distant frontier technology.

4. AI monetization must be separated from provider economics

The report distinguishes vendor-net AI/workflow revenue from provider-gross economics. Vendor revenue includes software, OEM-bundled AI, SaaS, enterprise subscriptions, and per-study fees. Provider-gross value includes patient-pay add-ons, workflow productivity, recall management, reimbursement, and downstream throughput. This separation avoids double counting and clarifies who captures value.

5. Breast ultrasound and breast MRI are not inside the core denominator, but they matter commercially

Supplemental imaging is central to the broader breast imaging pathway. Breast ultrasound and breast MRI are treated as adjacencies rather than core mammography revenue, but they materially shape diagnostic follow-up, dense-breast workflows, high-risk pathways, provider economics, and vendor ecosystem strategy.

6. Regional strategy is not one global adoption curve

The report frames mammography as a local policy and procurement market with global platform economics. Adoption is shaped by screening age bands, public-program design, insurance coverage, procurement systems, workforce constraints, provider-network structure, and local service capacity.

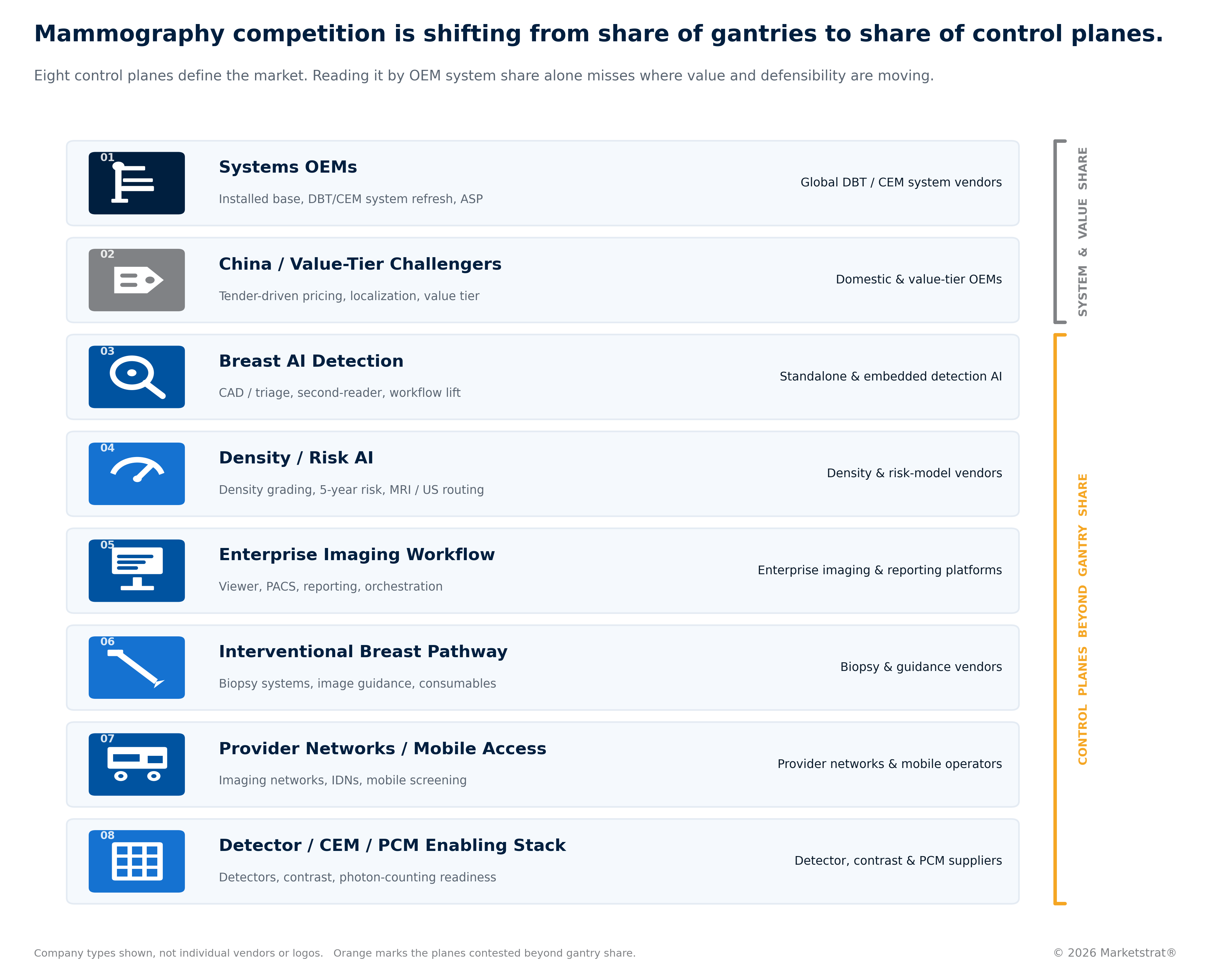

Marketstrat structures the mammography market into eight competitive clusters because the market is increasingly shaped by control planes rather than a flat OEM ranking.

The report analyzes:

The report’s competitive conclusion is that no single company controls every layer. Hologic remains the strongest vertical breast-health incumbent, GE and Siemens are credible enterprise and CEM/premium-technology challengers, software and AI platforms increasingly influence reading workflow, and China/value-tier players create a different unit-versus-value competitive tension.