Markintel Insights | Powered by Marketstrat

March 29-31, 2025

Executive Summary

The American College of Cardiology’s 2025 Annual Scientific Session (ACC.25) in Chicago confirmed a clear pivot in cardiovascular care: therapy innovations are moving well beyond conventional pharmacology and stent technology, toward integrated solutions bridging cardiometabolic treatments, AI-driven diagnostics, and value-based care models. Attendance returned to pre-pandemic levels, with 17,000+ professionals gathering to review over 50 late-breaking trials. This year’s program underscored six broad themes:

- Practice-Changing Clinical Trials: Landmark data on semaglutide (GLP-1) in PAD and oral PCSK9 inhibitors redefined frontiers in cardiometabolic risk reduction.

- Rise of Digital & AI: Extended ECG monitoring, AI-based imaging, and telehealth solutions transitioned from novelty to mainstream.

- Device Evolution: Transcatheter aortic valve replacement (TAVR) progress—now 80% of aortic valve replacements in the U.S.—and dedicated solutions for aortic regurgitation.

- Strategic Company Moves: Major pharma and medtech players signaled expansions, collaborations, and acquisitions targeting cardiometabolic therapies and digital health.

- Regulatory Tailwinds: Fast-track approvals, plus new CMS reimbursement pathways, are accelerating adoption of novel diagnostics and therapies.

- Future Outlook: Convergence across metabolic and cardiovascular therapies, next-gen valve devices, AI-based care models, and potential breakthroughs in lipoprotein(a) and gene therapies.

Executives and investors at ACC.25 appear to have left with a clear direction: cardiology is evolving toward proactive risk reduction and holistic patient management, powered by metabolic drugs, wearable tech, and advanced AI—offering both sizable market potential and stiff competition.

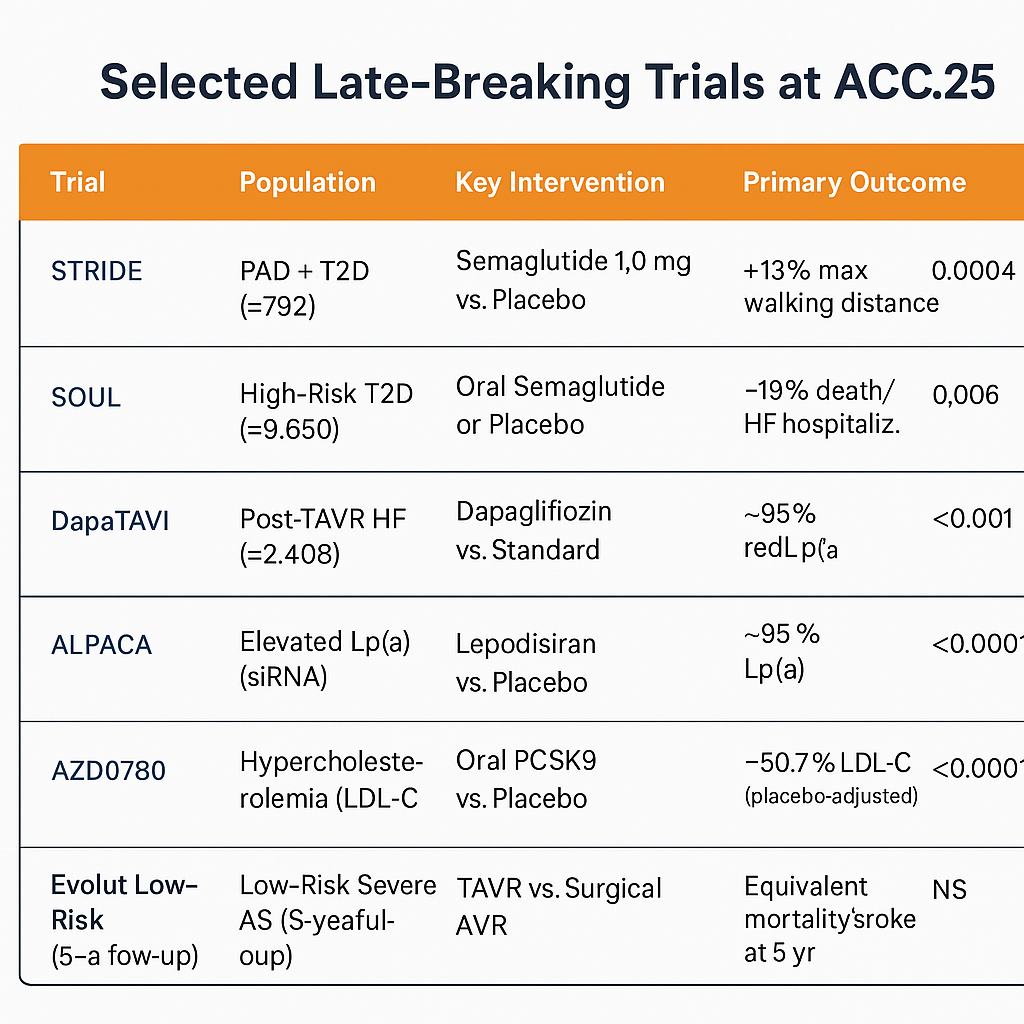

1. Key Clinical Trials & Scientific Breakthroughs

Each row above shows the p-value comparing the active intervention versus its respective control (placebo or standard care). These p-values indicate the statistical significance of each trial’s primary endpoint when comparing the treatment group to its control.

1.1 GLP-1 and SGLT2 Updates

- STRIDE (Semaglutide in PAD)

- Finding: +13% improvement in maximal walking distance vs. placebo (p=0.0004) at 52 weeks in patients with peripheral artery disease (PAD) and type 2 diabetes.

- Implication: First therapy in >20 years shown to enhance PAD functional outcomes. Likely to prompt label expansion and guideline updates.

- SOUL (Oral Semaglutide in High-Risk T2D)

- Finding: 14% reduction in 3-point MACE (CV death, MI, stroke) vs. placebo (p=0.006) in ~9,650 diabetics at high cardiovascular risk.

- Implication: Novo Nordisk to file for a formal cardiovascular risk-reduction indication for oral semaglutide, potentially reshaping frontline therapy for T2D patients with ASCVD.

- DapaTAVI (Dapagliflozin Post-TAVR)

- Finding: 28% reduction in the composite of all-cause death or heart failure hospitalization in older TAVR recipients at 1 year (p=0.02).

- Implication: Extends SGLT2 inhibitors into post-procedural HF management, reinforcing the “cardiorenal-metabolic” continuum of Farxiga.

1.2 Lipid Management: Lp(a) and Oral PCSK9

- ALPACA (Lepodisiran siRNA for Lp(a))

- Finding: ~95% drop in Lp(a) at 6 months; no major adverse events.

- Implication: Lp(a)-targeting agents could reach an estimated 8–20% of patients with high Lp(a) and no approved therapies. Phase 3 outcomes data will confirm event reduction.

- AZD0780 (Oral PCSK9 Inhibitor)

- Finding: 50.7% LDL-C reduction, plus modest 19.5% Lp(a) lowering.

- Implication: An oral PCSK9 could alter the dynamics of the injectable PCSK9 market, potentially expanding patient uptake through simpler administration.

1.3 Structural Heart and HF

- Five-Year Evolut Low-Risk

- Finding: TAVR vs. surgical AVR in low-risk aortic stenosis remained comparable out to 5 years.

- Implication: Reinforces TAVR durability in younger, lower-risk cohorts, fueling TAVR’s continued ascendancy.

- JenaValve for Aortic Regurgitation

- Finding: Encouraging early outcomes for non-calcified aortic regurgitation, historically not well served by TAVR.

- Implication: FDA humanitarian device exemption likely; potential new niche segment for transcatheter therapies.

Quote from Dr. John Wilson (Cleveland Clinic):

“Between GLP-1 agonists crossing into PAD management and emerging TAVR solutions for pure aortic regurgitation, this year’s ACC.25 gave us a clear roadmap to more targeted, less invasive treatment strategies.”

2. Company Announcements & Product Launches

2.1 Pharma Expansions

- Novo Nordisk: High-profile presence fueled by semaglutide data. Announced intent to file for expanded oral semaglutide indications in cardioprotection.

- Merck (Acceleron): Showcased sotatercept (Winrevair) data in PAH, planning an aggressive rollout and potentially evaluating broader uses.

- AstraZeneca: Spotlight on AZD0780 (oral PCSK9) and new post-TAVR label expansions for Farxiga; positioning itself at the forefront of cardiometabolic synergy.

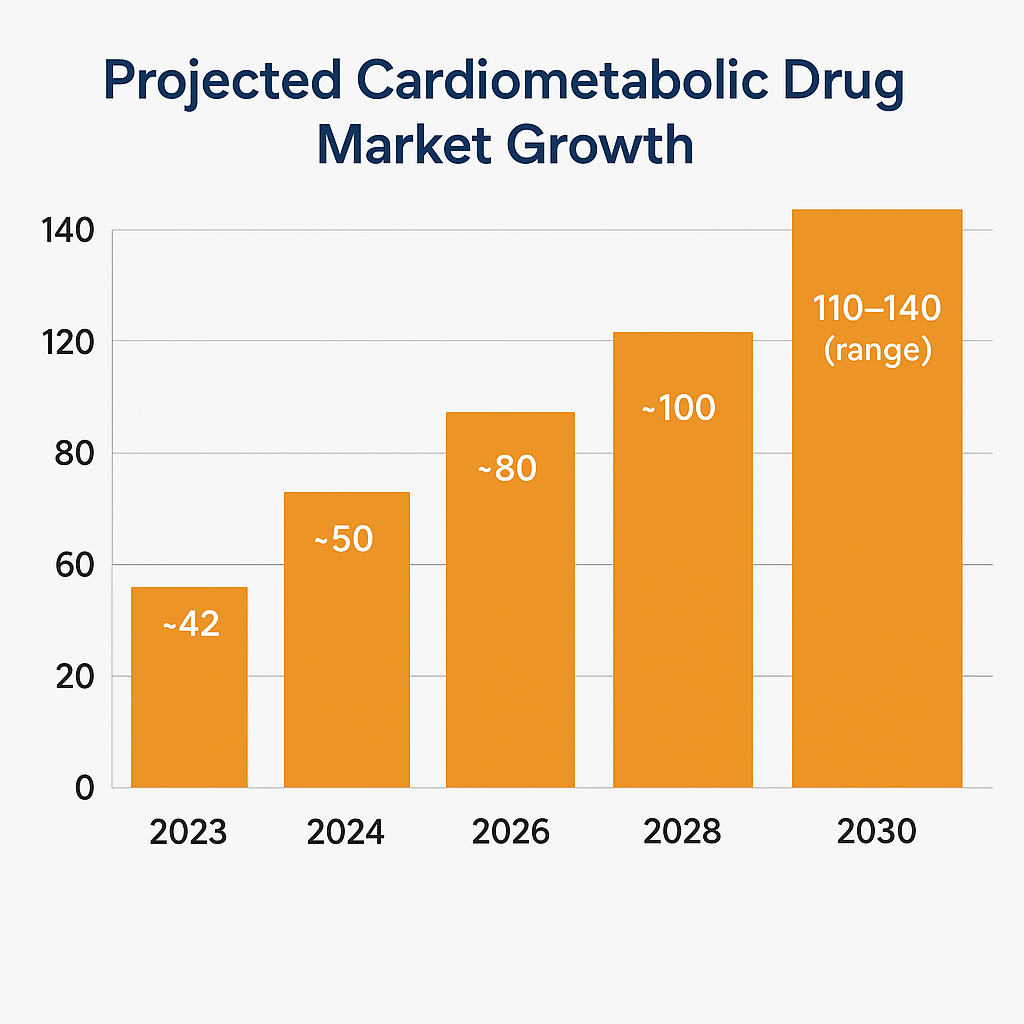

GLP-1 therapies (semaglutide, tirzepatide, etc.) are expanding from diabetes and obesity into cardiovascular/renal indications, fueling robust CAGR.

Above chart represents Marketstrat + industry estimates for the global GLP-1/cardiometabolic market through 2030. The numbers primarily reflect revenues driven by GLP-1 receptor agonists and related agents used in diabetes, obesity, heart failure, and broader cardiometabolic indications.

The 110–140B range in 2030 captures different uptake scenarios depending on further label expansions (e.g., for obesity, CKD, HF) and payer coverage. Growth is driven by the expanding role of these agents in cardiovascular risk reduction, as highlighted by trials reported at ACC.25.

2.2 Medtech Leadership

- Edwards & Medtronic: Reinforced TAVR dominance. Medtronic’s Evolut 5-year data indicates stable performance. Edwards advanced Sapien systems and teased expansions in mitral/tricuspid pipelines.

- JenaValve: Emerging player on track for AR-specific TAVR. Likely a near-term acquisition target if results remain consistent.

- Boston Scientific: Faced neutral results on Sentinel cerebral protection (PROTECT-TAVI). May shift emphasis to LAAC (Watchman) and next-gen ablation.

2.3 Imaging & Diagnostics

- GE HealthCare: Debuted Flyrcado™ (Flurpiridaz F-18) PET tracer with CMS pass-through payment plus the Revolution Vibe CT with AI-driven recon. A direct challenge to standard SPECT.

- iRhythm: Real-world analyses underscored Zio® patch superiority vs. 48-hour Holter, fueling adoption in arrhythmia detection.

2.4 Digital Health & Partnerships

- ACC’s Innovation Stage buzzed with collaborations:

- cliexa & ACC: Remote monitoring pilot for AFib/HF integrated into EHR workflows.

- UltraSight: AI-guided echo acquisition by novices—pointing to broader echo access.

3. Technology Trends & Innovations

3.1 AI in Cardiology

- Diagnostics: Deep-learning ECG risk stratification models match high-sensitivity troponin’s accuracy (AUC ~0.91).

- Imaging: AI-driven echo (100% sensitivity for severe AS) and AI-based CT recon (GE’s TrueFidelity™) reduce manual workloads and interpretive variability.

- Clinical Decision Support: Predictive models for LAA occlusion candidates, trial recruitment (e.g., Health360x).

3.2 Remote Monitoring & RPM

- Arrhythmias: 64% of actionable arrhythmias in daily-symptom patients occurred after 48 hours—missed by short-term Holters. Favors extended patch monitoring, implants, or even consumer wearables.

- Heart Failure: Weight/BP telemonitoring reduces 30-day readmissions via early interventions.

3.3 Telehealth & Hospital-at-Home

- Tele-Cardiac Rehab: Gains traction with improved adherence data.

- Virtual Triage: Apple Watch-based AF alerts triaged into e-consults, potentially reducing ED burdens.

3.4 Big Data & Omics

- Integration of registries and real-world data to identify hidden risk factors (e.g., Lp(a), microvascular disease), guiding next-generation therapies and screening policies.

4. Market Dynamics & Competitive Landscape

4.1 Pharmaceuticals

- GLP-1 Race: Novo Nordisk’s semaglutide vs. Lilly’s tirzepatide; analysts project the class could exceed $100B by 2030 as obesity, HF, and CKD indications expand.

- PCSK9 Disruption: Oral options from AZ, potential Lp(a) therapies from Lilly/Novartis set the stage for a second wave in lipid-lowering.

4.2 Devices & Procedures

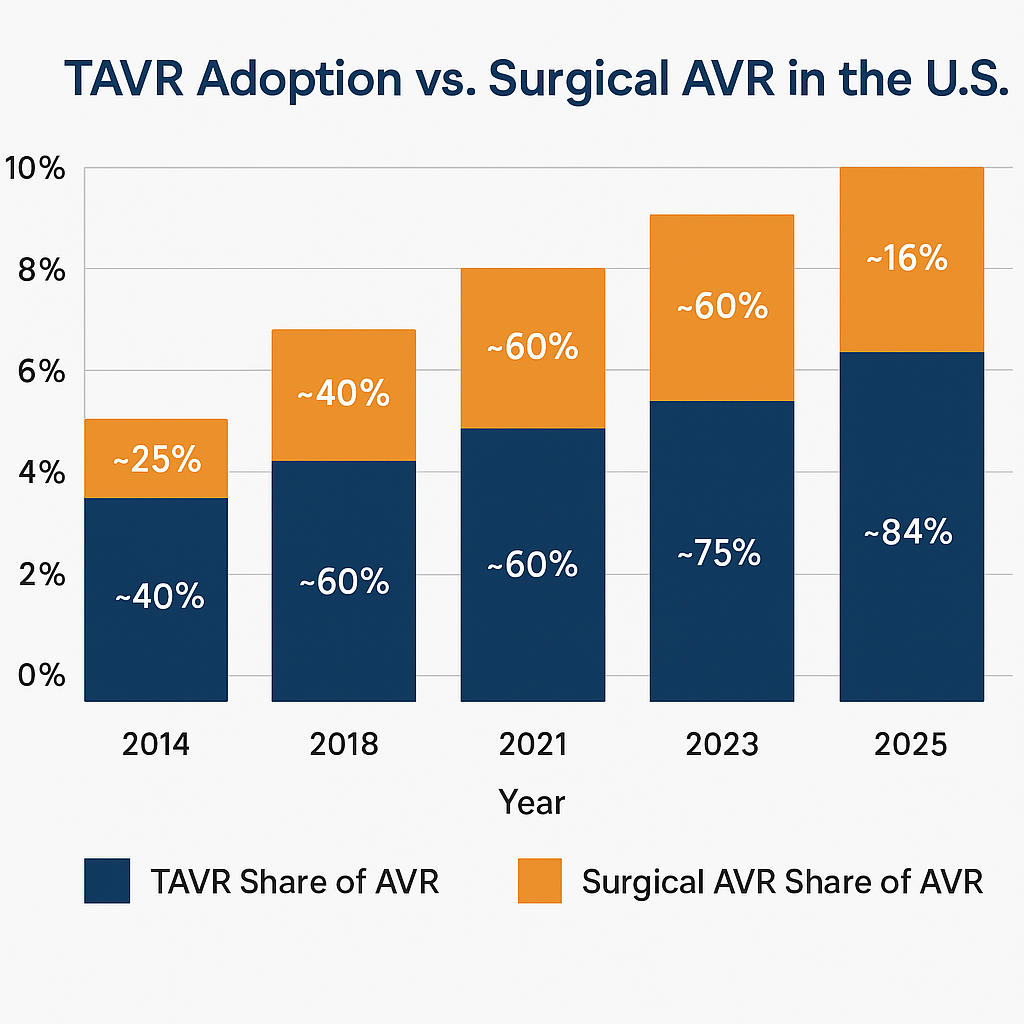

- TAVR Dominance: 80–84% of aortic valve replacements are transcatheter. Next battleground: younger patients, AR expansions, and competing structural solutions (mitral/tricuspid).

- Cerebral Embolic Protection Stall: Neutral trials hamper broad adoption. Boston Scientific may pivot resources toward LAAC or next-gen therapies.

TAVR has rapidly gained market share, surpassing 80% of aortic valve replacements in 2025, reflecting expanding indications (including low-risk AS).

Above chart shows approximate historical and forecasted shares of aortic valve replacements (AVR) performed via transcatheter (TAVR) versus conventional surgery (SAVR). The data are based on Marketstrat + industry estimates synthesized from reported U.S. procedural volumes. Exact percentages may vary by source but reflect the overall trajectory seen in ACC and registry data.

The 2025 figure (~84% TAVR) aligns with multiple industry analyses indicating continuous expansion of TAVR indications (from high- to low-risk patients) and broader adoption.

4.3 Digital Health Convergence

- Major Tech (Apple, Google, Amazon) quietly exploring deeper inroads into cardiology data, forging partnerships or acquisitions.

- Medtech vs. Consumer lines blurring; remote monitoring patch vendors and smartwatch-based solutions vie for overlapping segments.

4.4 Value-Based Care Pressures

- Hospitals and payers pushing solutions reducing readmissions and complications—SGLT2 in TAVR, integrated remote monitoring, AI triage—to improve outcomes under bundled payments.

5. Regulatory Developments

5.1 FDA Approvals

- Sotatercept (Winrevair): Approved for PAH with Breakthrough Therapy status. Sets precedent for rapid uptake of high-impact rare disease therapies.

- Bentracimab: Investigational ticagrelor reversal agent nearing BLA submission. Could revitalize brand adoption if approved.

5.2 CMS Reimbursement

- Pass-Through for GE’s Flyrcado PET tracer ensures separate payment, accelerating PET adoption for coronary perfusion imaging.

- RPM & Telehealth codes expanded; tele-cardiology coverage parity extended through 2026.

5.3 Guideline Updates

- Expect near-term ACC/AHA or ESC statements endorsing GLP-1 in PAD, shorter DAPT durations post-PCI, and universal Lp(a) screening once a targeted therapy is approved.

5.4 Compliance & Diversity

- The FDA focuses on trial diversity, requiring sponsors to detail enrollment of underrepresented cohorts. Could raise trial costs but improve real-world applicability.

6. Future Outlook

Short Term (Next 1–3 Years)

- Accelerated GLP-1 Uptake: Guidelines likely to endorse semaglutide in patients with PAD, fueling broad cardiologist adoption.

- TAVR Market Growth: Valve expansions (AR devices, younger low-risk approvals) plus marketing from big players driving volumes.

- M&A and Partnerships: Larger device or pharma players may acquire mid-tier AI/digital health startups for synergy in connected care.

Long Term (5+ Years)

- Cardio-Metabolic Convergence: Drugs addressing diabetes, obesity, and HF become standard CV risk management. Potential broad coverage of obesity meds if outcomes-based data remain strong.

- Gene & siRNA Therapies: Lp(a) and ANGPTL3-targeted therapies could reduce residual ASCVD risk significantly, diminishing the role of traditional lipid management in severe dyslipidemias.

- Holistic Digital Models: Continuous monitoring plus AI will enable “always-on” cardiology care, especially for heart failure and arrhythmias.

- Surgical vs. Transcatheter: As TAVR, mitral, and tricuspid transcatheter solutions expand, the balance of power shifts further toward minimally invasive approaches.

Conclusion and Strategic Considerations

ACC.25 signaled a turning point in cardiology where metabolic therapies, AI-driven diagnostics, and structural heart innovations converge to shape next-generation care. As TAVR cements its place, GLP-1 and SGLT2 options expand into new CV indications, and lipoprotein(a)/PCSK9 breakthroughs near market readiness, stakeholders should:

- Reevaluate Portfolios and Pipelines: Pharma must integrate cross-specialty (CV + metabolic) strategies; device manufacturers should diversify beyond aortic stenosis.

- Accelerate Digital/AI Adoption: Clinical trial data show tangible benefits and growing reimbursement support. Early investments in AI or remote solutions can yield competitive advantage.

- Focus on Outcomes & Value: Payers and providers increasingly demand evidence of cost-effectiveness. Emphasize economic analyses, real-world data, and synergy with value-based care imperatives.

- Monitor Regulatory & Guideline Shifts: Fast-track designations, pass-through reimbursements, and revised guidelines (e.g., shorter DAPT, Lp(a) screening) will rapidly influence adoption.

In sum, the window for strategic action is now. Over the next five years, new market entrants and incumbents who embrace integrated cardio-metabolic solutions, advanced device therapies, and AI-enabled care will be poised to reshape cardiovascular medicine and capture the resultant growth opportunities.

Note

- Data charts are based on Marketstrat + industry estimates, which combine internal analysis, public registry data, financial disclosures from major device and pharmaceutical manufacturers, and published market research forecasts.

- The p-values in Exhibit 1 derive from each respective trial’s official presentation or publication at ACC.25.