Marketstrat analyzes how CMS, Heartflow, Cleerly, Viz.ai and Philips are shifting imaging AI toward payment, workflow control and capacity.

🎧 Listen to this week’s Marketstrat Pulse Insight:

Medical imaging AI is entering a more demanding stage of commercialization. Regulatory clearance still matters, but the week ending July 10, 2026 showed that payment architecture, workflow control and measurable capacity release are becoming stronger determinants of adoption.

The latest Marketstrat Pulse Insights note centers on a two-sided shift. CMS is proposing to compress payment for specified routine imaging in excepted off-campus hospital departments while creating a provisional separate-payment structure for designated software services. At the same time, Heartflow, Cleerly, Keya Medical, Viz.ai, Cortechs.ai, CliniComp, Sectra and Philips are building value above the commodity imaging layer.

The central implication is straightforward: imaging AI must increasingly prove that it can be paid, distributed or converted into operating capacity.

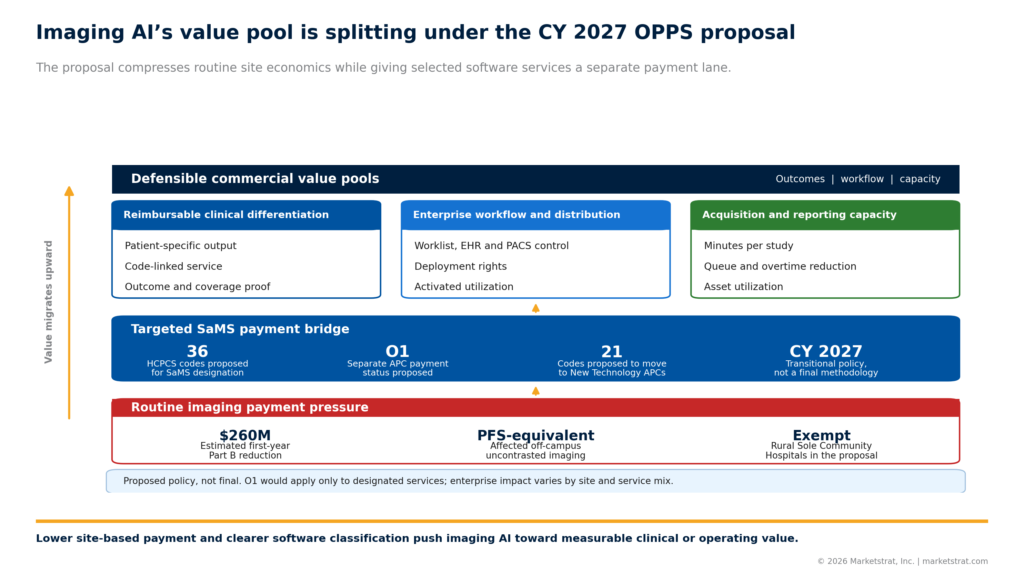

CMS separates imaging payment from software payment

The proposed CY 2027 Hospital Outpatient Prospective Payment System rule is the period’s most consequential policy development. CMS is proposing Physician Fee Schedule-equivalent payment for specified uncontrasted imaging furnished in excepted off-campus provider-based departments. The proposal would reduce the economic value associated with the hospital outpatient setting for affected services and place more pressure on cost per completed study.

Separately, CMS is proposing a Software as a Medical Service framework for designated codes, including a new status indicator intended to support separate payment and a transitional movement of selected services into New Technology APCs.

This is not broad reimbursement for imaging AI. The proposal is code specific, setting specific and provisional. Some software services may gain clearer payment visibility, while many workflow and productivity tools will remain provider funded.

A clinical service that produces a separately recognized patient-specific output can support per-use economics. A routing, reporting or capacity tool generally needs an enterprise business case based on time released, asset utilization, reduced leakage or improved follow-up.

Coronary plaque AI is becoming a disease-management category

Heartflow (NASDAQ: HTFL), Cleerly and Keya Medical are moving beyond plaque detection and measurement toward staging, structured reporting and longitudinal management.

The commercial unit is no longer simply an analytical output. The product must help clinicians classify disease, communicate risk, select therapy and revisit the patient over time. The strongest platform will need workflow fit, clinical actionability, evidence of changed management and a durable reimbursement path.

Heartflow’s plaque-staging approach, Cleerly’s configurable reporting and Keya Medical’s entry into quantitative plaque analysis show that competition is moving toward the complete care-management output.

The evidence standard must rise with that ambition. Reclassification is useful, but it does not by itself establish improved outcomes. The next proof points are whether staging changes medication, referral or intervention decisions, and whether payers support serial or expanded use.

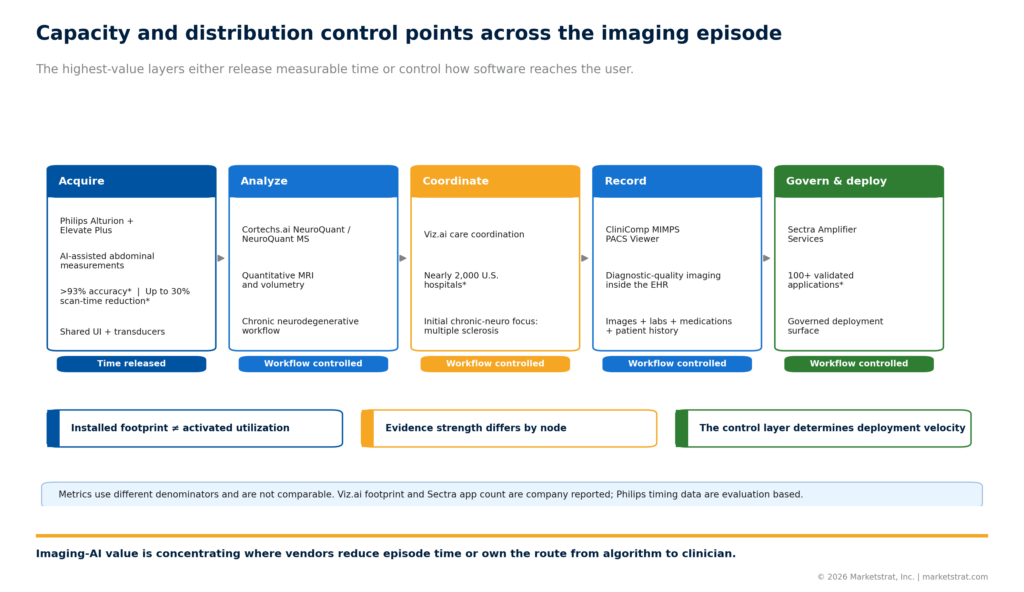

Distribution is becoming part of the product

Viz.ai’s integration of Cortechs.ai quantitative neuro-MRI tools shows how a specialist application can use an installed care-coordination platform to reach clinicians and chronic-disease workflows. CliniComp’s EHR-integrated PACS Viewer moves diagnostic-quality imaging closer to the longitudinal patient record. Sectra (STO: SECT B)’s enterprise-imaging environment illustrates how platforms can become governed channels for multiple applications.

The platform increasingly determines which products are deployable, visible to clinicians and commercially preferred. For point-solution vendors, integration can accelerate customer access, but it may also transfer control of the account, margin and usage data to the platform owner.

For providers, the attraction is lower application sprawl and a more standardized deployment path. The risk is dependence on fewer operating layers. Procurement teams will need to assess application portability, data access, governance, implementation responsibility and exit terms.

Installed footprint should also be separated from activated utilization. Availability through a large network represents a distribution opportunity, not adoption evidence. Activated sites, case volume, user engagement and renewal behavior are the stronger commercial measures.

Philips moves capacity AI into fleet economics

Philips (NYSE: PHG) is applying a related strategy on the acquisition side. Alturion and Elevate Plus are positioned as part of an ultrasound fleet, with common workflows and transducer compatibility intended to reduce implementation friction in high-volume environments.

The commercial value is not simply an AI-assisted measurement function. It is the possibility of more consistent acquisition, faster onboarding and improved throughput across an installed base.

Providers should track examination time, repeat scans, operator variability, training requirements, completed-study volume and staffing effects. Controlled evaluations can establish an initial signal, but enterprise adoption depends on whether gains persist across sites, operators and patient populations.

For independent AI vendors, OEM embedding raises the competitive bar. A comparable function bundled into the equipment and service relationship can be easier to adopt than a separate application. Independent vendors will need superior capability, multi-OEM reach or stronger evidence to offset that channel advantage.

Marketstrat view: the market is bifurcating

Marketstrat expects imaging AI business models to divide into two principal lanes.

The first consists of clinically bounded software services with an applicable billing pathway. These products can pursue per-use reimbursement, but they also face payer scrutiny around duplicate analysis, downstream utilization and evidence of outcome value.

The second consists of provider-funded workflow and capacity infrastructure. These products must demonstrate that they release minutes, reduce queues, increase completed studies, lower overtime, improve follow-up or avoid capital expenditure.

This bifurcation changes the diligence standard. Providers need study-level business cases. Vendors need a payment dossier and a distribution dossier. OEMs and enterprise platforms can use installed-base access as a moat. Payers need to distinguish additive clinical services from productivity tools. Investors and strategic acquirers should emphasize activated volume, implementation capacity, renewal behavior and channel control rather than clearance counts alone.

Imaging AI is no longer competing only on whether an algorithm works. It is competing on whether the product can be paid, distributed and converted into measurable clinical or operating value.

What to watch next

The near-term watchlist includes the final treatment of the CMS proposals, the coverage path for plaque quantification and staging, activated utilization from platform partnerships, and real-world capacity evidence from acquisition automation.

Each item tests the same thesis. Permission creates market access. Payment, workflow and capacity determine whether that access becomes durable adoption.

Read the full Marketstrat Pulse Insights research note for the detailed event analysis, stakeholder implications, deep dives, watchlist and source appendix. Subscribe at marketstrat.com for weekly research across medical imaging, imaging AI, enterprise imaging, reimbursement and image-guided care.

Subscribe to The Marketstrat Pulse for weekly analysis across medical imaging AI, enterprise imaging, reimbursement, provider platforms, regulatory activity and image-guided procedures: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.