ONE BIG THING

HIMSS26 showed that imaging AI is moving from stand-alone applications toward enterprise imaging orchestration — cloud-native viewers, workflow routing, and integrated diagnostics are becoming the real control surface, while reimbursement friction and MRI operating risk remain the main constraints on scaled adoption.

🎧 Listen to this week’s Marketstrat Pulse Insight on HIMSS26:

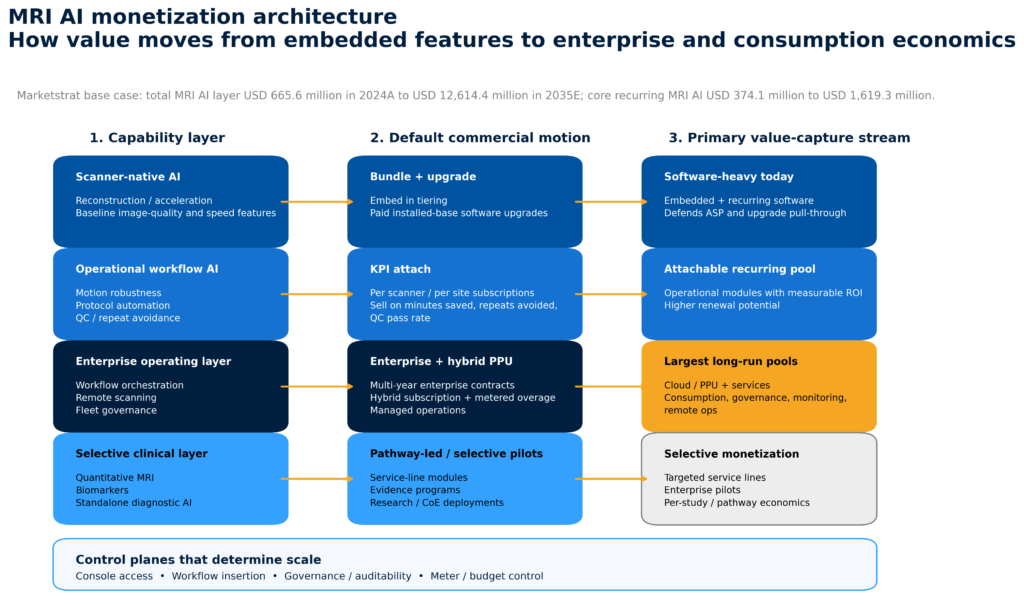

MARKET LENS – MRI AI MONETIZATION ARCHITECTURE

MRI is especially receptive to operational AI because the modality combines long exam times, protocol complexity, staffing sensitivity, motion vulnerability, and high installed-base dependence. External evidence supports the timing. MRI AI is scaling now because MRI departments are not buying “AI” in the abstract. They are buying relief from very specific constraints. Early commercial winners in MRI AI are rarely the most ambitious diagnostic stories. They are the use cases that convert directly into throughput, standardization, quality assurance, and labor leverage.

Source: Marketstrat MRI Horizon Research Program

KEY TAKEAWAYS

- Fact: GE HealthCare, Sectra, Merge, FUJIFILM Healthcare Americas Corporation, Philips, and Visage Imaging all used HIMSS26 to emphasize cloud-native viewing, orchestration, and integrated workflow rather than isolated algorithm launches. Interpretation: enterprise imaging is becoming the AI deployment layer that matters most commercially.

- Fact: Brainomix deployed 360 Stroke across all 25 WVU Health System sites. Interpretation: the most important AI adoption signal remains enterprise rollout, not incremental accuracy claims; this is AI behaving like infrastructure across a network rather than a site-by-site pilot.

- Fact: the FDA’s AI-enabled medical devices page was updated again, and the agency’s language points toward more explicit tagging or classification work for foundation-model-enabled devices. Interpretation: governance and compliance cost are rising alongside model ambition, which favors vendors with platform discipline and enterprise deployment maturity.

- Fact: GE’s View clearance and QT Imaging’s updated Breast Acoustic CT clearance, all reinforce that workflow software and novel platform filings are advancing through very different regulatory lanes. Interpretation: incremental workflow AI still scales fastest through familiar pathways, while truly novel platforms are choosing heavier regulatory burden to create whitespace.

- Fact: Medtronic’s announced $550 million agreement to acquire Scientia Vascular and Olympus’ VISERA ELITE III U.S. launch show that MIS competition continues to revolve around procedural ecosystem depth and visualization control. Interpretation: robotics and surgical imaging remain capital-allocation competitors to imaging IT modernization.

- Fact: helium pricing shock after the Qatar LNG disruption revived MRI operating-risk concerns. Interpretation: even in a software-heavy week, physical operating constraints still matter, especially for siting, relocation, service continuity, and total-cost-of-ownership arguments in MRI.

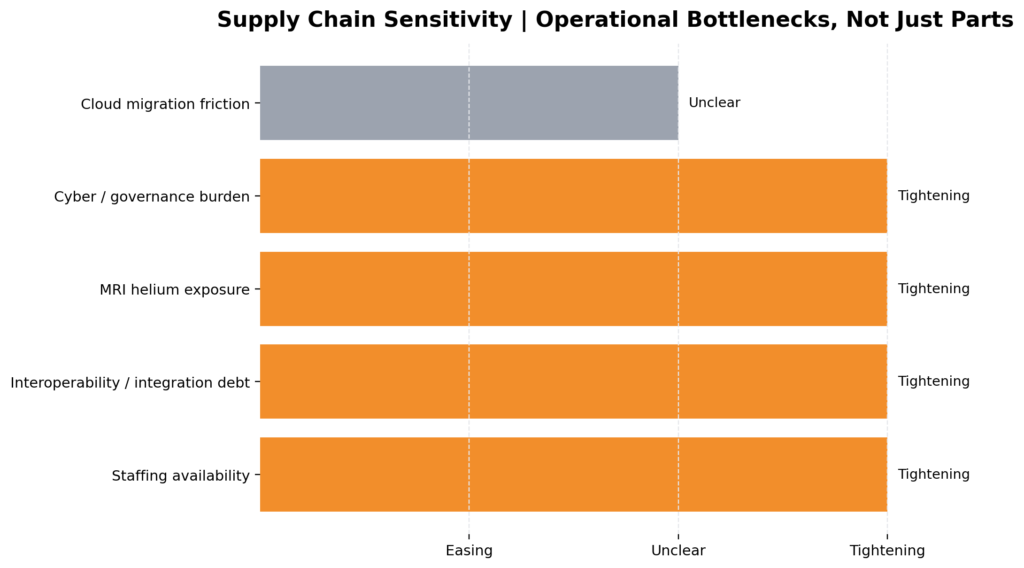

SUPPLY CHAIN SENSITIVITY

This week’s supply-chain picture was more operational than component-led, with one important exception: helium. Reuters’ reporting on the Qatar-related shock matters because MRI operators remain exposed to uptime, relocation, and refill risk even as the industry narrative keeps shifting toward software productivity. Note: industry experts indicate medical MRI operators are treated as priority-tier helium consumers and are unlikely to face allocation cuts; the near-term risk is cost inflation and TCO pressure rather than supply interruption. At the same time, HIMSS26 reinforced that interoperability debt, governance burden, and workflow fragmentation still function like hidden supply-chain constraints inside enterprise imaging. In other words, execution friction is now part of the supply chain story.

Sources: Reuters; gasworld; FDA; Sectra; Merative/Merge; Marketstrat analysis.

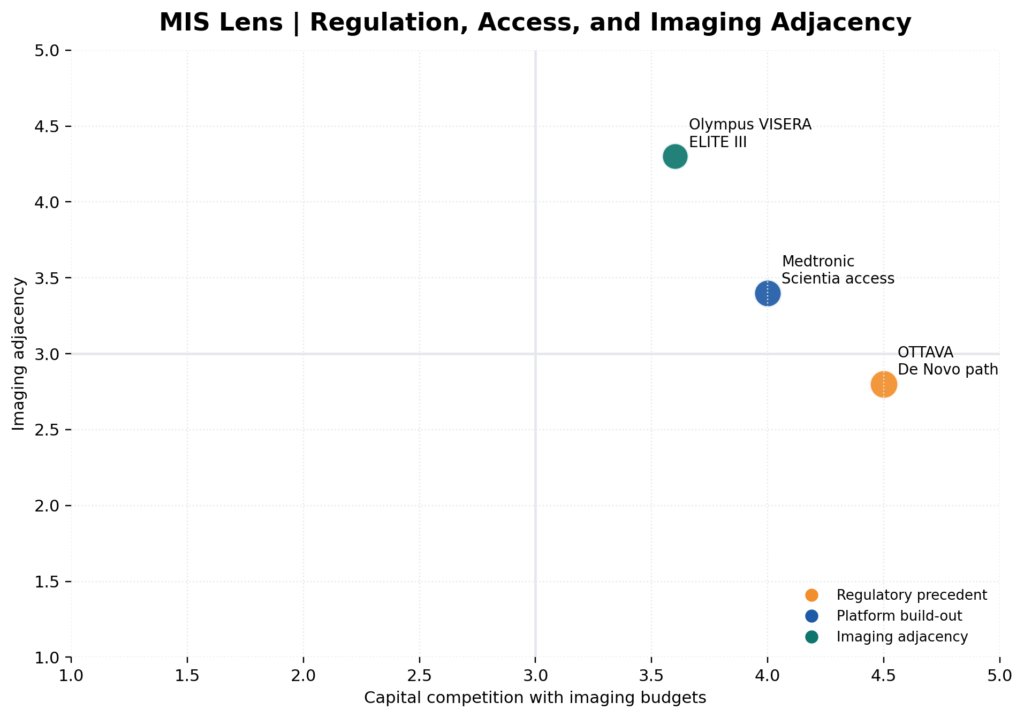

MINIMALLY INVASIVE SURGERY (MIS) LENS

MIS remains relevant because the same commercial playbook now visible in enterprise imaging is also showing up in surgical platforms. J&J’s OTTAVA De Novo submission (Jan ’26) is a classic platform-control move: accept a heavier regulatory path to try to define a new soft-tissue robotics predicate. Medtronic’s Scientia acquisition strengthens the neurovascular access layer rather than the robot itself, but the underlying logic is the same — procedural ecosystems are being built around completeness, reliability, and control. Olympus’ VISERA ELITE III reinforces that surgical imaging still competes for capital when it is sold as a multispecialty standardization platform.

Sources: Johnson & Johnson; Medtronic; Olympus; Marketstrat analysis.

Note: This section covers the MIS competitive landscape as strategic context for imaging capital allocation. Because MIS is a newer lens in the Pulse, some events predate the current week’s window — including J&J’s OTTAVA De Novo submission (Jan. ’26) — but are included where they anchor the platform architecture analysis or inform how current-week moves (Medtronic/Scientia, Olympus VISERA ELITE III) should be read.

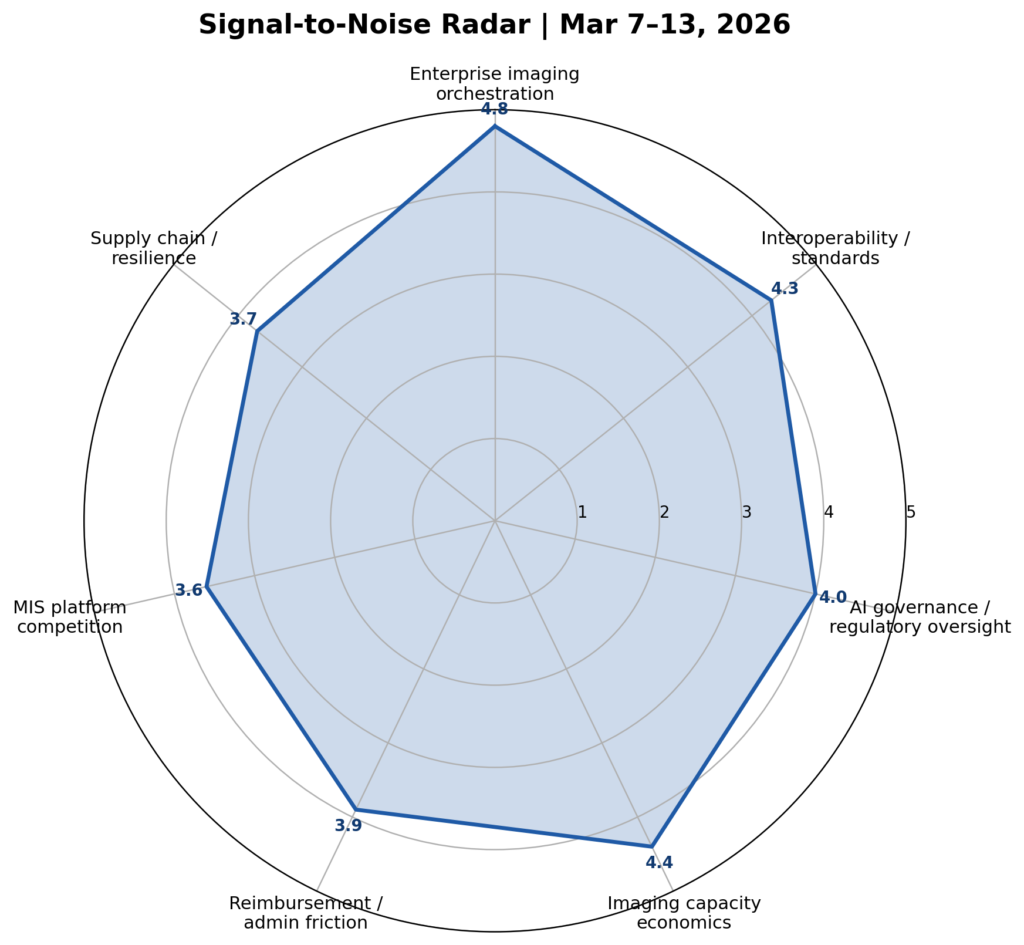

SIGNAL-TO-NOISE RADAR BY TOPIC – MARCH 7 – 13, 2026

The radar reads as a HIMSS26 map: enterprise imaging orchestration, capacity economics, interoperability, and governance all score at the high end because vendors converged on the same commercial language — fewer interfaces, cleaner deployment, clearer ROI. Reimbursement remains meaningful, but it was more a drag factor than the week’s central direction-setter. Supply chain and MIS stayed active but secondary.

Sources: Marketstrat weekly topic scoring (derived from this week’s events and policy signals)

QUIC-GLANCE TABLE

| Date | Headline | Our Take | Source |

| 2026-03-09 | GE HealthCare wins FDA 510(k) for View diagnostic viewer | GE’s clearance matters because it pulls cloud-native diagnostic viewing and advanced visualization into the core workspace, strengthening the case that workflow control — not just modality hardware — is now a strategic software surface. | Q1 |

| 2026-03-09 | Sectra showcases MCP-powered AI workflows at HIMSS26 | Sectra is pushing AI integration toward orchestration and open standards inside ente rprise imaging, which matters more commercially than another single-model launch because it changes who owns deployment friction. | Q2 |

| 2026-03-10 | Philips expands HealthSuite diagnostics at HIMSS; adds cloud pathology on AWS | Philips is broadening the integrated diagnostics thesis beyond radiology alone, which raises the value of cross-domain data harmonization and supports a larger enterprise software attach story. | Q3 |

| 2026-03-05* | Fujifilm pushes Synapse AI Orchestrator and Worklist Orchestrator | Fujifilm’s signal is about workflow routing and assignment logic. That is strategically stronger than point-AI news because it embeds value into daily study distribution and enterprise operations. | Q4 |

| 2026-03-10 | Visage 7.1.20 adds browser viewing, Chat+, and AI reporting at HIMSS26 | Visage continues to make the premium CloudPACS case by reducing workflow fragmentation rather than simply showcasing another algorithm layer. | Q5 |

| 2026-03-09 | Merge positions cloud-native enterprise imaging and orchestration at HIMSS26 | Merge’s message matters because it frames cloud migration as a practical prerequisite for standardized remote reading and orchestration, not just an IT architecture preference. | Q6 |

| 2026-03-11 | Brainomix deploys 360 Stroke across all 25 WVU sites | This is one of the week’s clearest proofs that AI is now being deployed as network infrastructure. Multi-site rollout is a much stronger commercial signal than another limited-site validation study. | Q7 |

| 2026-03-10 | FDA updates AI-enabled device list and signals foundation-model tagging work | The update is a governance signal. As FDA tracking becomes more explicit for modern AI architectures, compliance burden and platform maturity will matter more in procurement and valuation. | Q8 |

| 2026-03-10 | QT Imaging secures FDA 510(k) for enhanced Breast Acoustic CT | A meaningful but narrower regulatory event: practical usability improvements can matter more than headline novelty when the commercialization path depends on workflow fit. | Q9 |

| 2026-03-10 | Medtronic agrees to buy Scientia Vascular for $550M | This is a portfolio-completeness move in neurovascular, reinforcing that OEM value increasingly comes from owning more of the procedural chain rather than a single device category. | Q10 |

| 2026-03-11 | Olympus launches VISERA ELITE III in the U.S. | Surgical imaging remains a real capex claimant. Olympus is selling multispecialty OR standardization rather than a niche visualization upgrade, which is the right commercial framing in a tight-budget environment. | Q11 |

| 2026-03-12 | Helium prices spike after Qatar LNG halt, reviving MRI operating risk | This week’s supply-chain signal was not abstract: helium risk affects MRI service continuity, relocations, and lifecycle economics, which can re-enter procurement logic quickly. | Q13 |

| 2026-03-10* | UHC’s April 1 radiology PC documentation rule becomes a live operational issue | Not a new policy this week, but it is becoming commercially relevant now because it directly strengthens the ROI case for AI documentation and reporting tools. | Q14 |

Source Key

- Q1 — GE HealthCare / Business Wire, Mar. 9, 2026 — View diagnostic viewer 510(k).

- Q2 — Sectra, Mar. 9, 2026 — MCP-powered enterprise imaging at HIMSS26.

- Q3 — Philips, Mar. 10–11, 2026 — Integrated Diagnostics and cloud-enabled pathology at HIMSS26.

- Q4 — Fujifilm, Mar. 5, 2026 — Synapse AI Orchestrator / Worklist Orchestrator at HIMSS26.

- Q5 — Visage / PR Newswire, Mar. 10, 2026 — Visage 7.1.20 at HIMSS26.

- Q6 — Merative / Merge, Mar. 9, 2026 — cloud-native enterprise imaging and orchestration.

- Q7 — Brainomix / DAIC, Mar. 11, 2026 — 25-site WVU rollout.

- Q8 — FDA, Mar. 10, 2026 — AI-enabled medical devices list update.

- Q9 — QT Imaging / Business Wire, Mar. 10, 2026 — enhanced Breast Acoustic CT clearance.

- Q10 — Medtronic, Mar. 10, 2026 — Scientia Vascular acquisition.

- Q11 — Olympus, Mar. 11, 2026 — VISERA ELITE III U.S. launch.

- Q12 — Johnson & Johnson, Mar. 7, 2026 — OTTAVA De Novo submission.

- Q13 — Reuters / gasworld, Mar. 11–12, 2026 — helium shock and MRI operator risk.

- Q14 — APMA / Becker’s, Jan. 5–6, 2026; included because the Apr. 1 implementation horizon makes it operationally live this week.

This week’s Pulse research note also covers: enterprise imaging orchestration and cloud-native diagnostic viewers; FDA regulatory activity including imaging software clearances and AI governance signals; reimbursement and policy developments affecting imaging AI adoption; imaging capacity economics and workflow productivity models; MRI operational risk including helium supply sensitivity; enterprise AI deployment across health system networks; surgical robotics and MIS platform competition; and hospital capital allocation across imaging IT, AI, and procedural platforms.

Full analysis with frameworks, signal dashboards, and deeper dives available on AlphaSense.

About Marketstrat

Marketstrat® is a market intelligence and GTM enablement firm committed to empowering clients in data-driven industries. Under the Markintel™ brand, it delivers robust market intelligence, while GrowthEngine solutions offer specialized GTM advisory and app-based tools—together fueling growth, innovation, and competitive advantage. For more information, visit www.marketstrat.com.

Marketstrat® is a registered trademark and Markintel™ is a pending trademark of Marketstrat.

Check out free Research and Insights and Analysis of Industry Events

Check out our collection of Markintel Horizon and Markintel Pulse research.

Check out details on our reports, World Market for AI in Medical Imaging World Market for Oncology Imaging AI and other Pulse Reports in the Imaging space.