The week ending June 26 showed that imaging AI adoption now depends on workflow governance, platform layering, reimbursement, enterprise distribution and supply resilience.

Imaging AI activity resumed across CT, MRI and mammography, but the week’s bigger signal was not clearance volume. Aidoc and HOPPR moved report drafting toward the next workflow frontier. DeepHealth/RadNet expanded mammography into cardiovascular and prior-exam signal capture. GuideAI and Cercare showed that focused clinical niches still matter. The adoption test is shifting from “authorized” to “deployable, governed, reimbursable and operationally useful.”

🎧 Listen to this week’s Marketstrat Pulse Insight:

Imaging AI’s center of gravity is moving

The week ending June 26 was not defined by a flood of FDA clearances. It was defined by a more important shift: imaging AI is moving beyond the question of whether it can be authorized.

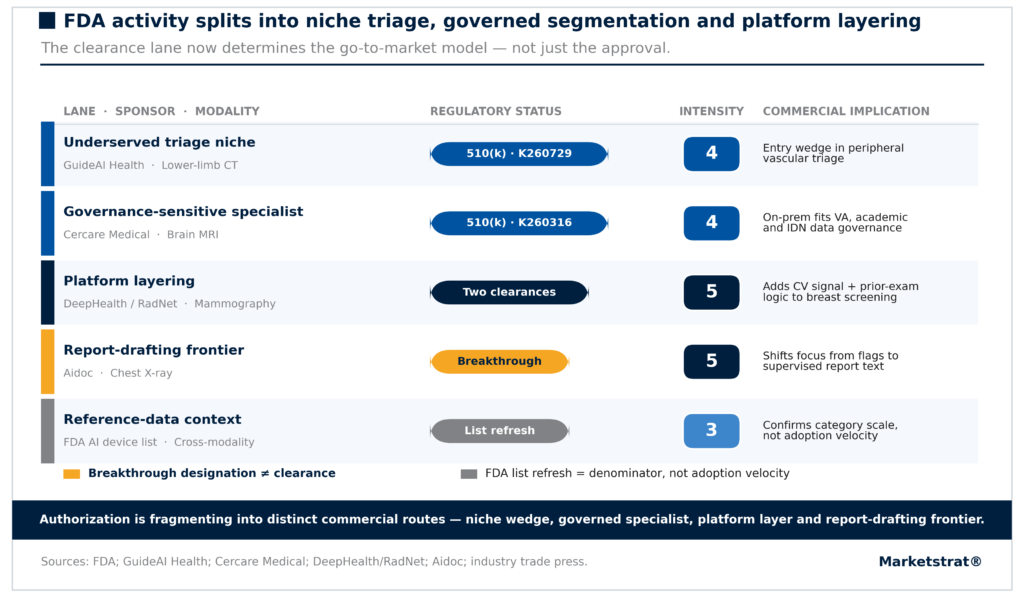

GuideAI Health received FDA 510(k) clearance for VascularAssist Occlusion Triage, a CT-based peripheral vascular tool for lower-extremity disease prioritization. Cercare Medical cleared Oncology Virtual Expert, an on-premise brain-tumor MRI segmentation product. DeepHealth, the imaging AI arm of RadNet, received two clearances that add breast arterial calcification assessment and prior-exam integration to Breast Suite.

Those events matter, but the broader pattern matters more. New entrants are selecting clinical niches where competition is less crowded. Specialists are designing software around governance-sensitive buyers. Platforms are layering more functions onto high-volume screening workflows.

The market is no longer asking only whether imaging AI can pass regulatory review. It is asking whether the tool can be used inside real clinical operations.

Marketstrat FDA lanes map showing GuideAI, Cercare, DeepHealth and Aidoc across imaging AI regulatory pathways.

FDA activity split across niche triage, governance-led segmentation, platform layering and report-drafting frontier signals.

Report drafting moves into the regulated workflow conversation

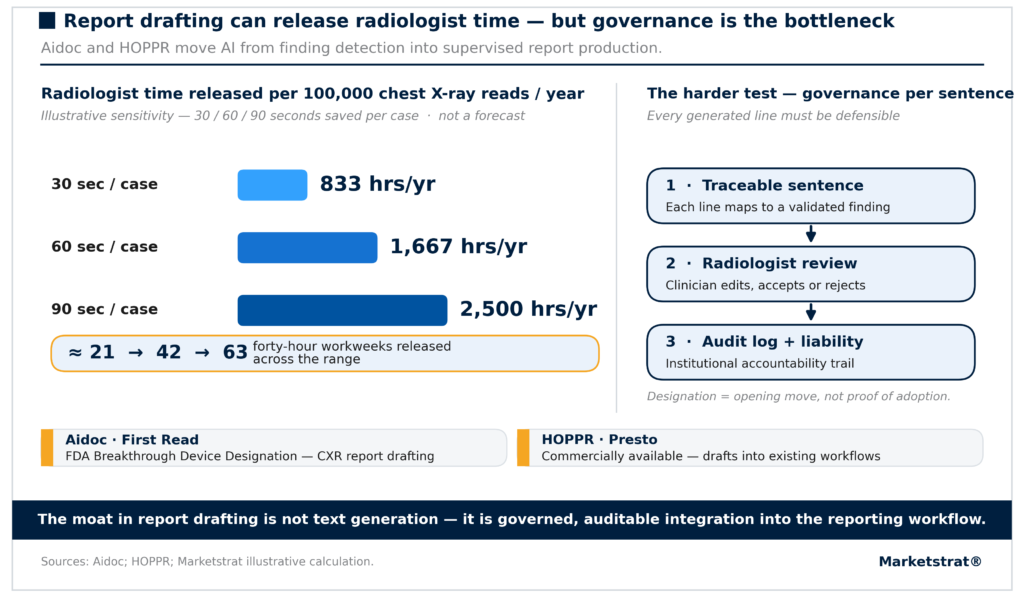

Aidoc’s FDA Breakthrough Device Designation for First Read is one of the week’s most important signals. It is not a clearance, but it brings report drafting into a more formal regulatory frame.

That distinction is critical. Triage AI flags cases. Detection AI highlights findings. Report-drafting AI moves closer to the final clinical record.

The product challenge therefore changes. A successful reporting tool must do more than generate fluent text. It needs to map generated language to validated findings, fit institution-specific reporting templates, preserve radiologist review, log edits and remain auditable. It must also work inside the systems radiologists already use.

HOPPR’s Presto launch highlights the same operating reality from a different angle. Hospitals do not want to rip out PACS, reporting systems or dictation workflows to test generative reporting. A model-agnostic infrastructure layer that imports AI findings into existing reporting environments may be more commercially valuable than a model that sits outside workflow.

Marketstrat exhibit showing illustrative radiologist time savings from AI report drafting and the governance chain for generated report text.

Report drafting can release radiologist time, but governance per sentence is the adoption gate.

DeepHealth shows why mammography is becoming a platform

DeepHealth’s new FDA clearances show the strategic value of a high-volume screening encounter. Breast arterial calcification assessment creates an opportunistic cardiovascular signal from a routine mammogram. Prior-exam integration strengthens longitudinal comparison and workflow logic.

Mammography is well suited to platform layering because it has recurring patient volume, historical imaging data and established screening infrastructure. One encounter can support multiple clinical questions: cancer detection, density, prior comparison, future risk and cardiovascular signal capture.

For DeepHealth and RadNet, this is not only a software story. It is a deployment-surface story. RadNet’s outpatient imaging footprint gives DeepHealth a channel to test workflow, refine adoption and build commercial proof inside real screening operations.

The key question is whether these added signals translate into economic value. Payers and providers will look for evidence of reduced recalls, better risk stratification, appropriate follow-up, referral quality and measurable patient outcomes.

Capacity evidence is becoming the cleanest provider ROI language

Provider buyers respond to AI most clearly when it releases measurable capacity. Kaiser Permanente’s reported MRI acceleration results were important because they translated AI into scan-time and wait-time improvements.

That type of proof is easier for administrators to underwrite than another accuracy metric. A tool that compresses scan time, shortens a backlog or improves asset utilization can be connected to revenue, access, overtime, staffing and patient experience.

Report drafting extends the same logic to radiologist time. If a supervised reporting layer saves even small amounts of time per high-volume study, the capacity effect can become meaningful across a large imaging operation. The caveat is that productivity claims must be tested against actual radiologist behavior, review requirements and reporting quality.

Akumin and CGS Premier’s relocatable-clinic initiative points to another form of capacity release: physical access. Imaging throughput is not only constrained by machines and readers. It is constrained by site availability, deployment cycles, rural access, staffing and capital intensity.

Distribution and supply still decide who scales

This week also reinforced a less glamorous but more durable commercial point: adoption depends on distribution architecture.

Sectra’s cloud imaging agreements show how regional and outpatient networks are standardizing on enterprise imaging layers. Pro Medicus’ investment and resale arrangement with Echo IQ show the value of channel access for cardiac AI. Akumin’s relocatable-clinic model shows that physical distribution remains a strategic variable.

For vendors, the implication is direct. A strong model still needs a route into workflow. That route may be an owned network, a cloud platform, a reseller arrangement, an enterprise reporting layer or a mobile infrastructure model.

Supply resilience is the other side of the same adoption equation. Lantheus’ CRL for LNTH-2501 was tied to third-party manufacturing, underscoring that nuclear imaging commercialization depends on production quality and radiopharmacy execution. Helium, breast-biopsy needles and reporting labor are different constraints, but each can limit throughput after the technology itself works.

Clearance opens the door. Adoption still depends on workflow integration, reimbursement logic, distribution control and the physical ability to complete the imaging episode.

What Marketstrat is watching next

The next phase of imaging AI will likely be decided by five tests.

First, reporting AI must prove sentence-level governance and fit into existing dictation workflows. Second, breast AI platforms must show whether multi-signal screening improves outcomes or mainly creates more downstream work. Third, capacity AI must quantify minutes released and exams added. Fourth, reimbursement must expand beyond the narrow set of cardiac imaging use cases with dedicated payment pathways. Fifth, enterprise imaging and provider platforms will increasingly control which tools get deployed.

For executives, investors and product leaders, the market is moving from model proof to adoption architecture.

Subscribe to The Marketstrat Pulse for weekly analysis across medical imaging AI, enterprise imaging, reimbursement, provider platforms, regulatory activity and image-guided procedures: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.