A light approval week revealed a sharper market signal: imaging AI is being judged by its ability to protect constrained clinical pathways.

🎧 Listen to this week’s Marketstrat Pulse Insight:

A narrow approval week with a broad operating signal

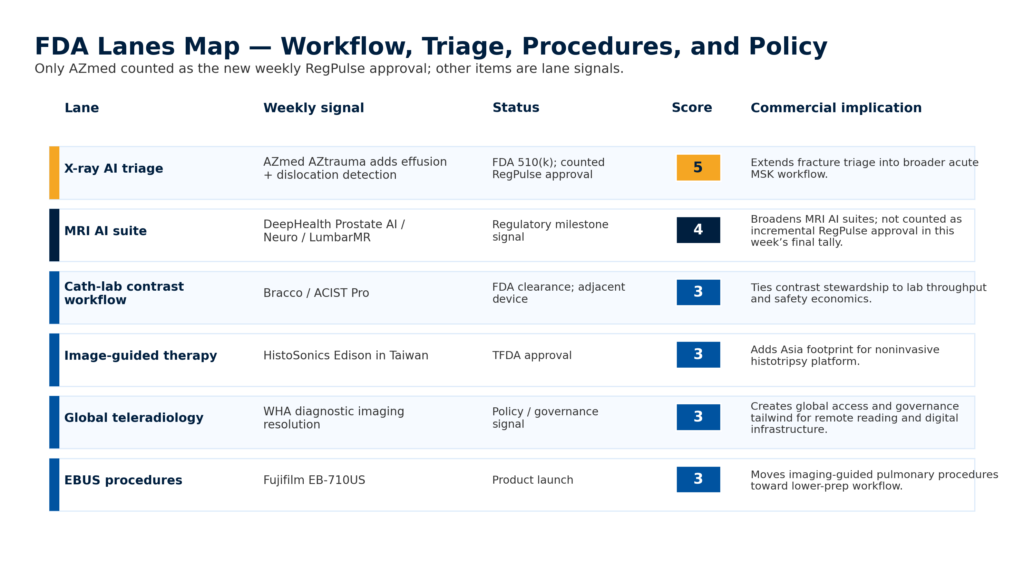

The week ending May 22, 2026, did not produce a flood of new imaging AI approvals. Marketstrat’s RegPulse count increased by one, with AZmed’s expanded AZtrauma clearance as the single new counted approval.

That does not make the week quiet. It makes it more revealing.

The strongest market signal was not approval volume. It was the way companies, providers, policymakers, and evidence generators converged around one problem: imaging capacity is under pressure, and the next generation of AI-enabled tools is being evaluated by whether it reduces friction in real pathways.

Capacity is no longer just a question of scanner count or radiologist headcount. It now includes emergency department timing, MRI access, X-ray triage breadth, cloud data readiness, image-guided procedure workflow, radiologist assistant utilization, breast biopsy consumables, and teleradiology infrastructure.

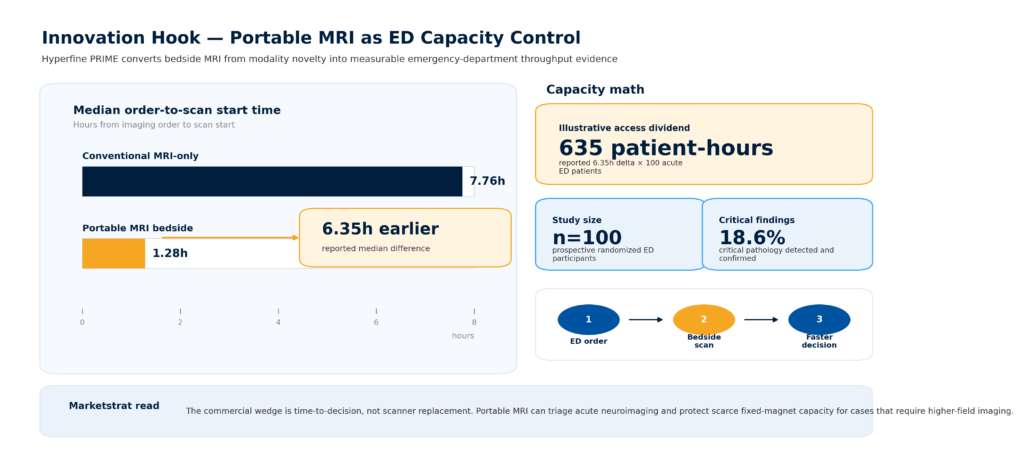

Signal 1: Portable MRI reframed time-to-imaging

Hyperfine’s PRIME study was the clearest operating signal of the week. The reported median order-to-scan start time was 1.28 hours in the portable MRI arm versus 7.76 hours for conventional MRI-only workflow.

That is a meaningful framing shift.

Portable MRI does not need to replace fixed MRI to matter commercially. Its strategic role is to shorten acute imaging delays, reduce transport dependency, and protect fixed-magnet capacity for cases that require higher-field imaging. For hospital operators, that moves portable MRI from modality novelty to workflow intervention.

The reason this matters is simple: ED imaging delays ripple across triage, boarding, specialist availability, and downstream care decisions. A faster scan pathway can create value even when the image is not a full substitute for conventional MRI.

Portable MRI turns time-to-imaging into a measurable ED capacity metric.

Sources: Hyperfine PRIME study results; Marketstrat analysis

Signal 2: X-ray AI is moving toward multi-pathology triage

AZmed’s expanded AZtrauma clearance added joint effusion and dislocation detection to fracture detection on X-ray. This was the only new RegPulse approval counted this week.

The commercial read-through is broader than the label itself. X-ray AI has often been evaluated as a narrow abnormality detector. A broader MSK triage module creates a stronger enterprise value proposition because the same integration can support more emergency and outpatient presentations.

For providers, the relevant question becomes: how many decisions can one workflow tool influence per exam?

For vendors, the implication is clear. Point solutions remain viable only when they offer superior performance, distribution, or integration. Otherwise, multi-pathology suites will have a stronger buyer case.

Signal 3: The platform layer is becoming a control surface

DeepHealth announced regulatory milestones across prostate, neuro, and lumbar MRI workflows. Flywheel integrated with AWS HealthImaging to support imaging data for trials, AI development, and secondary research. GE HealthCare and UW Medicine launched a collaboration tied to imaging research and clinical workflow development.

Together, these moves point toward an infrastructure thesis.

The algorithm remains important, but the commercial control layer may sit elsewhere: the MRI suite, the data curation layer, the enterprise imaging platform, the cloud repository, the clinical research network, or the OEM-academic workflow environment.

This is why imaging AI procurement is becoming less like software selection and more like operating architecture design. Health systems want tools that fit into reporting, routing, trial imaging, longitudinal follow-up, and governance.

Regulatory and policy signals widened across X-ray AI, MRI workflow, contrast management, teleradiology, and EBUS procedures.

Sources: AZmed / RADIN Health; DeepHealth; Bracco / ACIST; HistoSonics; WHO; Fujifilm.; Marketstrat Analysis

Signal 4: Policy and supply risk are part of the capacity stack

Two non-algorithmic signals were especially important.

First, MARCA was reintroduced to support Medicare payment for certain radiologist-assistant-supported services under radiologist supervision. That is a labor-capacity signal. It does not solve radiologist shortages, but it points toward team-based throughput as a policy lever.

Second, ACR issued guidance around a stereotactic breast biopsy needle shortage. This is a reminder that imaging pathways can break at the consumable level. A high-value cancer workup can be slowed not only by scanner access or interpretation backlog, but by needle availability, modality substitution, and triage decisions.

These issues belong in the same strategic conversation as AI because they define whether imaging can happen at the right time.

What this means for providers, vendors, and investors

Providers should evaluate imaging AI through a capacity lens. That means asking whether a tool reduces wait time, broadens triage coverage, standardizes reporting, lowers downstream leakage, improves staffing leverage, or supports scarce-specialist workflows.

Vendors should package products around pathway value, not model count. The strongest positioning will connect performance to a measurable operating metric: minutes saved, scans routed, reports standardized, data prepared, procedures streamlined, or capacity protected.

Investors should separate clearance volume from commercial leverage. The market will reward companies that can prove the link between AI-enabled workflow and utilization economics.

The next imaging AI winners will not be defined only by detection performance. They will be defined by whether they reduce bottlenecks in constrained clinical pathways.

Related research themes

- Radiology AI commercialization

- Enterprise imaging platform control

- MRI workflow and throughput

- X-ray AI triage

- Cloud-native imaging data infrastructure

- Imaging reimbursement and labor policy

- Teleradiology and global access

- Image-guided procedure workflow

- Supply-chain sensitivity in imaging

Subscribe to The Marketstrat Pulse: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.