Roche/PathAI, ACR/SIIM governance, Siemens and Philips earnings, CMS prior-auth digitization, and new workflow clearances show imaging value moving beyond model performance.

Imaging AI’s next phase is less about proving algorithms and more about governing, monitoring, integrating, and monetizing them inside clinical workflow. This week’s Marketstrat Pulse highlights five signals: Roche’s PathAI acquisition, the ACR/SIIM AI practice parameter, OEM margin stress at Siemens and Philips, CMS electronic prior authorization, and new clearances across pathology, ultrasound, CT/MR, urology, and EUS.

🎧 Listen to this week’s Marketstrat Pulse Insight:

The operating era begins

The imaging AI market is moving into a more disciplined phase.

For several years, the public story was algorithm performance: detection, sensitivity, specificity, validation cohorts, and FDA clearances. Those still matter. But this week’s highest-signal developments point to a different commercial center of gravity.

The question is becoming: who controls the workflow after the model is deployed?

That control surface can be pathology image management, scanner automation, PACS/RIS integration, reporting, AI quality assurance, prior authorization, radiation therapy planning, urodynamics, EUS-guided drainage, or molecular imaging supply.

This is the operating era of imaging AI.

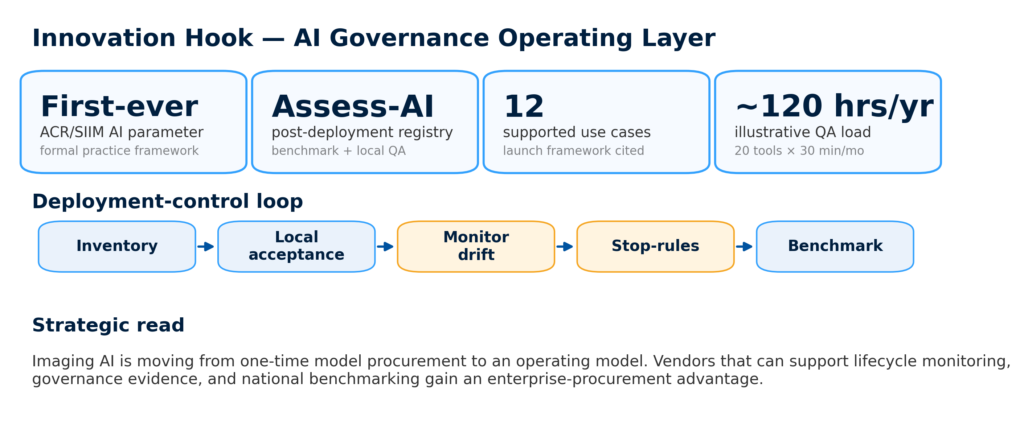

Marketstrat visual showing imaging AI governance workflow, including inventory, local acceptance, drift monitoring, stop-rules, and benchmarking

Signal 1: Digital pathology AI becomes infrastructure

Roche’s agreement to acquire PathAI for $750M upfront plus up to $300M in milestones is the clearest platform-control signal of the week.

This is not simply an AI transaction. It is a diagnostic workflow transaction.

Pathology AI sits at the intersection of image management, algorithm development, biomarker discovery, companion diagnostics, lab operations, and oncology decision-making. Roche’s move signals that strategic buyers increasingly view AI pathology as a scaled operating layer, not a narrow software feature.

For radiology AI vendors, the read-through is direct. The market is rewarding platforms that live inside decision pathways. Model count alone is not enough if the vendor lacks distribution, workflow integration, governance support, or downstream economic relevance.

Signal 2: Governance becomes part of procurement

The ACR/SIIM practice parameter and Assess-AI registry framework may be even more important than a new model clearance.

The framework formalizes what health systems need to manage after AI goes live: an AI inventory, version tracking, local acceptance testing, performance monitoring, stop-rules, privacy controls, and benchmarking.

That shifts the budget conversation from AI license to AI operating model.

For providers, governance creates work. A system running multiple AI tools needs a practical process for monitoring performance, escalating issues, documenting exceptions, and deciding when a model should be paused or replaced.

For vendors, governance creates differentiation. FDA clearance and strong validation metrics remain necessary, but enterprise buyers will increasingly ask whether the vendor can support lifecycle monitoring, auditability, registry participation, and local performance review.

The new imaging AI moat is not model count. It is monitored workflow control.

Signal 3: OEM demand is not the same as OEM margin durability

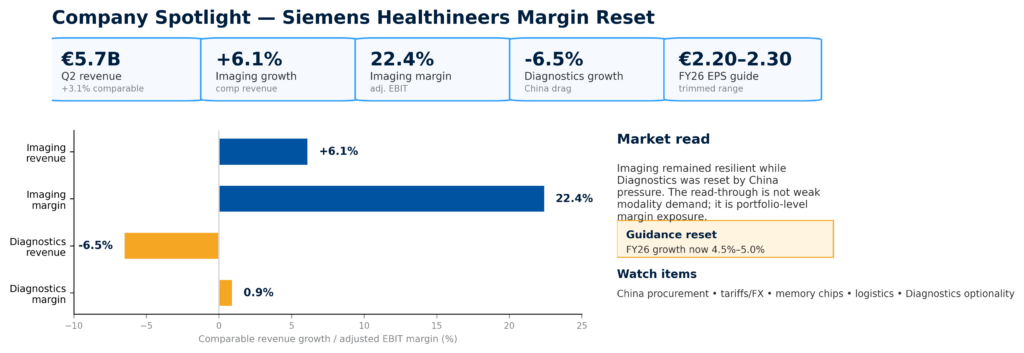

Siemens Healthineers and Philips provided the week’s cleanest OEM signals.

Siemens Healthineers showed resilient Imaging performance, but cut FY26 guidance as Diagnostics in China deteriorated sharply and cost pressures remained active. Philips posted order growth and reiterated guidance while leaning on productivity, AI-enabled workflow, and service partnerships.

The strategic message is nuanced.

Imaging demand can remain healthy while portfolio-level margin risk rises. Hardware replacement cycles, modality demand, and service relationships can still be attractive. But OEMs now face a more complex margin environment involving China procurement and reimbursement, tariffs, foreign exchange, electronics, memory chips, helium exposure, logistics, and service reliability.

That changes how large OEMs sell.

Scanner performance still matters, but procurement increasingly focuses on uptime, workflow automation, installed-base economics, service attach, software bundling, and total operating cost.

Marketstrat chart on Siemens Healthineers Q2 FY2026 imaging growth, diagnostics pressure, and FY26 guidance reset.

Signal 4: Regulation is widening into decision layers

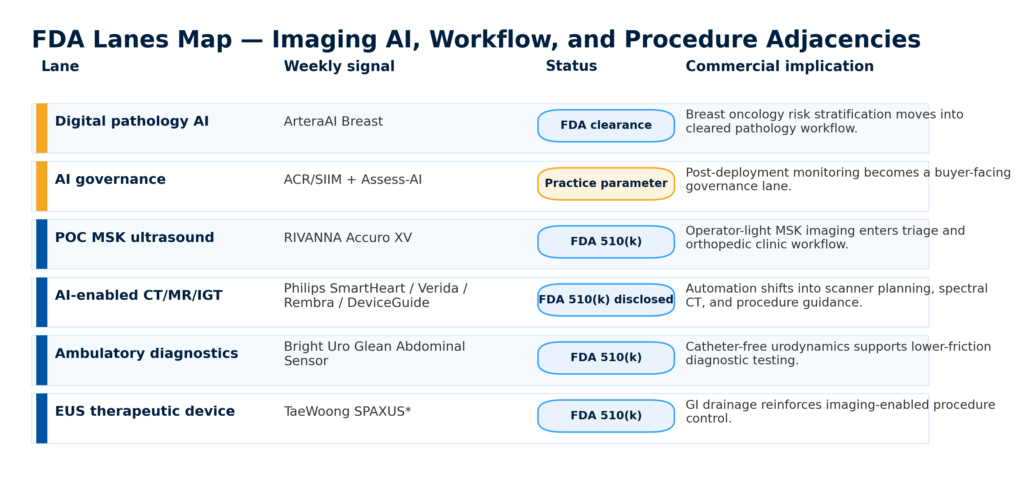

This week’s regulatory activity was broader than traditional radiology AI.

ArteraAI Breast extends AI risk stratification into breast oncology pathology. RIVANNA’s Accuro XV opens a point-of-care MSK ultrasound lane. Philips disclosed AI-enabled CT, cardiac MR, and image-guided therapy clearances. Bright Uro added catheter-free urodynamics. TaeWoong’s SPAXUS clearance reinforces EUS-guided drainage as a procedure-control adjacency.

The pattern is important.

AI and imaging are moving into decision layers that sit before, during, and after the diagnostic read. This includes scanner acquisition, treatment-risk stratification, triage location, procedural guidance, radiation planning, and follow-up pathways.

The strongest opportunities are likely to appear where imaging changes a decision, not merely where it adds a visual output.

FDA lanes map for imaging AI, digital pathology, point-of-care MSK ultrasound, AI-enabled CT/MR, urodynamics, and EUS therapeutic devices.

Signal 5: Prior authorization becomes digital infrastructure

CMS is pushing providers and EHR vendors toward electronic prior-authorization readiness ahead of payer API requirements in 2027. UnitedHealthcare also said it will remove prior-authorization requirements for 30% of services that previously required approval.

For imaging providers, this can reduce visible administrative friction. Fewer manual submissions, fewer portal checks, and cleaner electronic workflows should matter.

But it is not a simple retreat from utilization management.

Digital prior authorization can also make payer control more standardized, more measurable, and more precise. Imaging groups should expect the bottleneck to shift from manual work to payer-specific rules, API readiness, denial analytics, and evidence packaging.

Marketstrat POV

The week’s main lesson is that imaging AI is becoming an operating asset class.

Providers should build governance capacity before scaling tool count. Vendors should treat lifecycle monitoring as a commercial feature. OEMs should sell workflow capacity and reliability, not only scanner specifications. Investors should focus on workflow control surfaces rather than standalone algorithms with weak channel access.

The next phase of imaging AI will not be won by the loudest model story. It will be won by platforms that reduce friction across triage, reporting, prior authorization, access, follow-up, procedure planning, and post-deployment quality assurance.

Related research themes

Subscribe to The Marketstrat Pulse for weekly market intelligence across medical imaging AI, enterprise imaging IT, reimbursement, MedTech strategy, and image-guided procedures:

https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

- Medical imaging AI governance

- Enterprise imaging and PACS workflow

- Digital pathology platform strategy

- Imaging reimbursement and prior authorization

- OEM imaging margin pressure

- Image-guided procedure platforms

- PET/CT and molecular imaging economics

- Radiology AI procurement and post-deployment monitoring

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.