OEM-provider alliances, cloud enterprise imaging, and CPT signals accelerate distribution-led adoption across radiology and Minimally Invasive Surgery.

ONE BIG THING

Enterprise imaging is being purchased as infrastructure—alliances + cloud + scaled reporting networks—while MIS platforms apply the same “bundle + workflow” playbook.

KEY TAKEAWAYS

- Distribution moats are shifting upstream: multi-year OEM–provider alliances and managed imaging operations are becoming the default path to AI scale (vs point-solution adoption).

- Cloud enterprise imaging is the new “operating system”: migrations reduce upgrade friction and create the substrate for modular AI add-ons and workflow analytics.

- Reimbursement plumbing is moving (slowly) in emerging modalities: Category III CPT codes don’t equal coverage, but they create the claims “handle” needed for payer evidence and policy formation.

- Regulatory is bifurcating: incremental clearances in procedural guidance and visualization continue—while policy-level proposals (and PCCP-style lifecycle controls) could materially reshape radiology AI pathways.

- Provider-side scale is consolidating: teleradiology and enterprise imaging operations are concentrating—this is a distribution shift that matters as much as algorithm performance.

- MIS read-through: robotic ablation consolidation and single-use visualization clearances reinforce platformization and intensify capital allocation competition with imaging IT modernization.

LATE-BREAKING UPDATE (March 2, 2026 — post-publication window)

RadNet to Acquire Gleamer for ~€230M (~$250M): The Infrastructure Thesis Gets Its Proof Point

As this edition went to press, RadNet announced the acquisition of French radiology AI company Gleamer for up to €230M. RadNet will integrate Gleamer’s high-volume AI suite (BoneView, ChestView) into its DeepHealth subsidiary, creating what is likely the world’s largest radiology AI portfolio by scan volume. Gleamer’s 700+ European client base provides immediate trans-Atlantic distribution scale.

Why it matters for this edition’s thesis: This deal is a direct expression of the “One Big Thing” — enterprise imaging AI is being purchased as infrastructure. DeepHealth is no longer an aggregation of screening point solutions; it is becoming a comprehensive AI operating system for high-volume routine radiology workflow. The strategic pattern — platform + distribution + volume economics — mirrors the GE-UCSF alliance logic at a different layer of the stack.

Marketstrat will publish a dedicated research note on the RadNet/Gleamer acquisition with full competitive, financial, and strategic analysis. Contact us for further details.

QUICK-GLANCE TABLE

| Date | Headline | Our Take | Source (URL) |

| 2026-02-26 | GE HealthCare + UCSF Health launch 10-year Care Alliance | OEMs are moving into operating-model partnerships; remote scanning + workforce programs signal capacity economics as the core thesis. | UCSF (Home) / MedTech Dive (MedTech Dive) |

| 2026-02-26 | Sectra signs NHS trust for Sectra One Cloud enterprise imaging | Cloud migration is becoming the default upgrade path—and the easiest “surface” to attach AI modules at scale. | Sectra (Sectra Medical) |

| 2026-02-25 | AMA approves Category III CPT X579T for breast ultrasound tomography | Early reimbursement infrastructure: creates traceable utilization, but coverage will hinge on evidence and payer policy formation. | ICE (ICE) |

| 2026-02-24 | Quantum Surgical acquires NeuWave Medical | MIS platform consolidation continues: robotics + ablation bundling can accelerate adoption—if economics and evidence follow. Note: NeuWave was divested by J&J (Ethicon), which is concentrating its MIS portfolio on the Ottava robotic platform — a signal of portfolio rationalization in the robotics-ablation space.” | GlobeNewswire (GlobeNewswire) |

| 2026-02-24 | Brainomix extends Series C to $25.4M | “Scale capital” is flowing to outcomes-anchored imaging AI; the U.S. commercialization push is the tell. | PRNewswire (PR Newswire) |

| 2026-02-23* | Medica Group acquires Axon Diagnostics + Mitis Health | Teleradiology + diagnostics networks are consolidating; distribution and staffing leverage matter as much as software. | AuntMinnieEurope (AuntMinnieEurope) |

| 2026-02-26 | FDA clears platform for personalized workflow during TAVR/cardiac pacing | CTA-to-fluoro planning/overlay expands intra-procedural imaging guidance—incremental regulatory lane, meaningful workflow impact. | Cardiovascular Business (Cardiovascular Business) / BioSpace (BioSpace) |

| 2026-02-26 | FDA clears qXR-Detect CXR AI — 6 indications in one clearance, with PCCP lifecycle control | PCCP is the real story: this is a blueprint for faster iteration without constant resubmissions. | Diagnostic Imaging (Diagnostic Imaging) / FDA DB (FDA Access Data) |

| 2026-02-24 | Inova first to implement new GE cardiac MRI technology | “First install” announcements are early indicators of deployment velocity and site-level proof points for platform upgrades. | ICE (ICE) |

| 2026-02-21 | GE updates LOGIQ ultrasound systems with automation | Workflow automation claims are increasingly framed in minutes saved, not “AI features”—a more defensible value story. | Diagnostic Imaging (Diagnostic Imaging) |

| 2026-02-24 | NXXIM takes over Apollo Enterprise Imaging operations (MSA) | Enterprise imaging operations are being platformized (MSO-style)—this is a direct distribution channel for AI workflow layers. | PRNewswire (PR Newswire) |

| 2026-02-25 | Xenocor announces FDA clearance of Saberscope single-use articulating laparoscope | Single-use visualization expands outpatient flexibility, but shifts costs into per-case consumables + supply reliability. | BioUtah (BioUtah) |

| 2026-02-23 | AHA urges guardrails for AI used in prior authorization | Providers are pushing back on “black-box denial” risk; utilization AI vendors need transparency + governance-by-design. | AHA (American Hospital Association) |

| 2026-02-26 | CMS billing/coding article update adds ICD-10 codes (A57591 R8) | Incremental policy changes can widen payable populations; operators should re-check pre-auth + documentation rules. | CMS (cms.gov) |

| 2026-02-27 | Harrison.ai radiology AI 510(k) exemption petition comment window closes | If this pathway changes, barriers to entry shift—watch for “flood vs filter” dynamics in CAD/triage. | Federal Register (Federal Register) / STAT (STAT) |

*Medica’s announcement with Axon Diagnostics and MITIS Health was issued ~Feb 17; trade coverage within the reporting window.

MARKETSTRAT POV

- Providers: Treat cloud migrations and OEM alliances as capacity projects (downtime, scheduling, staffing utilization), not “IT refreshes.” Contract around measurable operational KPIs (scan uptime, report TAT, room closures avoided).

- OEMs: The moat is shifting from magnets and probes to operating model + upgrade velocity (remote scanning support, standardized protocols, managed cybersecurity, predictable refresh cycles).

- AI vendors: Distribution is the bottleneck. Prioritize platform surfaces (enterprise imaging stacks, telerad networks, MSO-style ops) and regulatory lifecycle tooling (PCCP-capable change management).

- Payers: Category III CPT signals “evidence collection mode,” not coverage. Define coverage-with-evidence thresholds early to avoid multi-year ambiguity.

- MIS vendors: Expect intensified capital competition with imaging modernization. Win by quantifying cross-service-line ROI (LOS, complication reduction, OR time) and integrating imaging guidance + data.

INNOVATION HOOK

GE HealthCare + UCSF Health 10-year Care Alliance (remote scanning + workforce + clinical innovation).

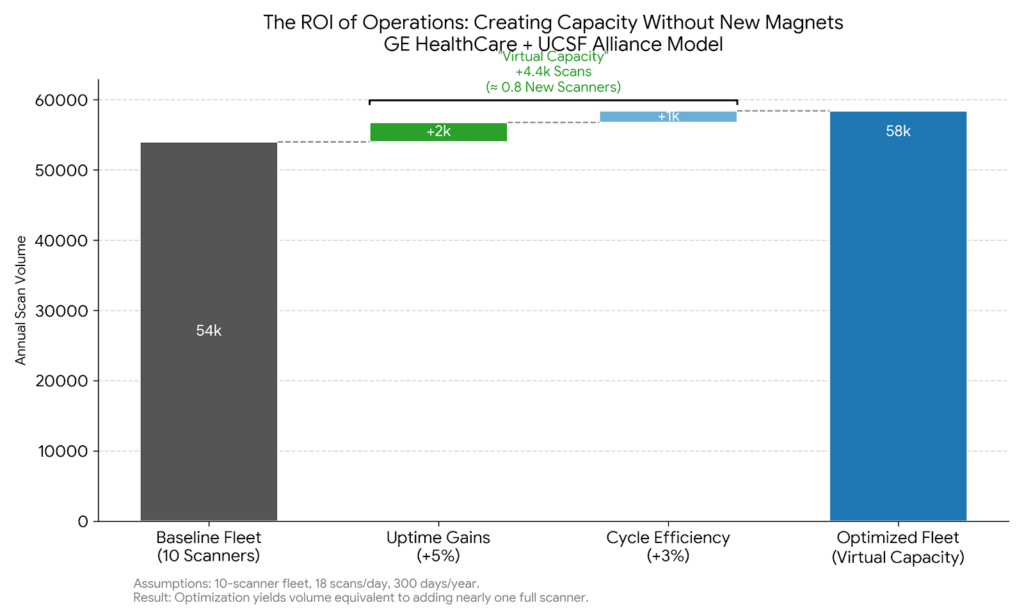

The novelty isn’t “another partnership”—it’s the explicit positioning of imaging as an operating model problem. When alliances include remote scanning support, training pipelines, and standardized innovation workflows, the commercial unit shifts from “hardware sale” to “capacity outcomes.” That matters because in constrained labor markets, the highest-ROI “new scanner” is often the one you already own—if you can lift uptime and cycle efficiency without adding headcount.

The chart below visualizes the core argument of the GE HealthCare + UCSF alliance: operational improvements create “virtual capacity” equivalent to buying new hardware. This “Waterfall” model demonstrates how marginal gains in uptime and cycle efficiency stack up to create the output of nearly one full additional scanner—without the capital expense of a new magnet. Explore the interactive chart (hover for specific data points) here.

Key Takeaway: By treating imaging as an operating model problem rather than a hardware problem, the alliance unlocks ~4,400 additional scans per year from the existing fleet.

Illustrative capacity math: a 10-scanner fleet running 18 scans/day at 300 days/year is ~54k scans/year. A modest +5% uptime and +3% cycle-time gain lifts throughput ~8% (~4.4k incremental scans/year), equivalent to adding ~0.8 scanners of capacity—without new magnets. (Assumptions shown; not UCSF-disclosed.)

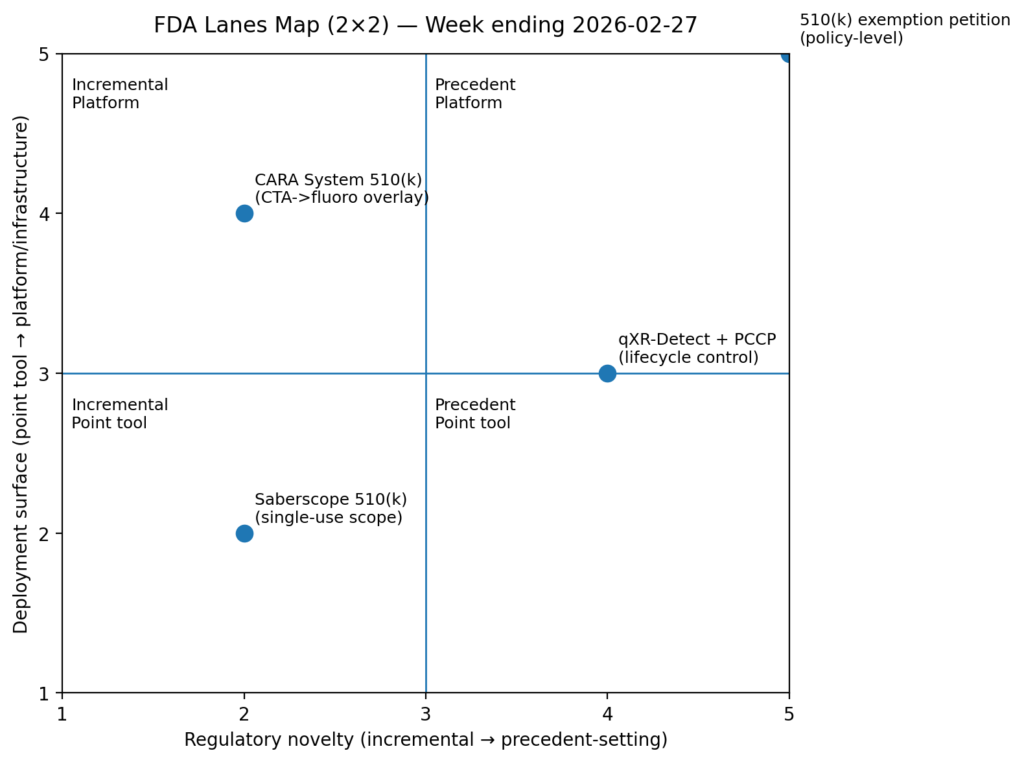

FDA LANES MAP FOR AI SOFTWARE

Incremental vs precedent-setting pathways

Regulatory is bifurcating into (1) steady incremental clearances in procedural guidance and visualization, and (2) precedent-setting proposals and lifecycle controls that could reshape radiology AI velocity. PCCP-style authorizations matter because they potentially decouple model improvement from repeated submissions. Meanwhile, exemption petitions create pathway uncertainty—raising the strategic value of compliance-ready data/QA infrastructure.

Think of the FDA lanes as a portfolio: incremental tools add workflow value today, while precedent-setting moves (PCCP, exemptions) change the economics of iteration. Companies with enterprise deployment surfaces will benefit most if pathway friction falls, because they can ship improvements faster across larger installed bases.

The complete Marketstrat Pulse is available on AlphaSense – – with the full analytical toolkit, including all frameworks including Signal Heatmap, Supply Chain Sensitivity, MIS Lens, EVI, and more.

About Marketstrat

Marketstrat® is a market intelligence and GTM enablement firm committed to empowering clients in data-driven industries. Under the Markintel™ brand, it delivers robust market intelligence, while GrowthEngine solutions offer specialized GTM advisory and app-based tools—together fueling growth, innovation, and competitive advantage. For more information, visit www.marketstrat.com.

Marketstrat® is a registered trademark and Markintel™ is a pending trademark of Marketstrat.

Check out free Research and Insights and Analysis of Industry Events

Check out our collection of Markintel Horizon and Markintel Pulse research.

Check out details on our reports, World Market for AI in Medical Imaging World Market for Oncology Imaging AI and other Pulse Reports in the Imaging space.