The week ending June 5, 2026 showed imaging AI becoming infrastructure for workflow, capacity, oncology planning, nuclear medicine, and outpatient distribution.

🎧 Listen to this week’s Marketstrat Pulse Insight:

Estimated read time: 5 minutes

This week’s Marketstrat Pulse shows a clear shift in imaging AI strategy. The strongest signals were not isolated algorithms. They came from companies embedding AI into modality fleets, reporting systems, oncology planning, PET workflows, and provider distribution channels. Philips, GE HealthCare, Subtle Medical, Lantheus, Telix, United Imaging, RadNet, Microsoft, and payer-policy signals all pointed to the same conclusion: imaging AI is becoming a platform-control market.

The week’s thesis

The imaging AI market is moving into a more disciplined phase. The early question was whether algorithms could detect, segment, quantify, or triage better than traditional workflows. That question still matters, but it is no longer sufficient.

The new question is where AI sits in the operating model.

The week ending June 5, 2026 produced several signals that point in the same direction. AI is becoming more valuable when it is embedded in installed modality fleets, radiation oncology planning, PET capacity management, reporting infrastructure, outpatient imaging networks, and reimbursement-sensitive workflows.

That makes platform control the central commercial issue.

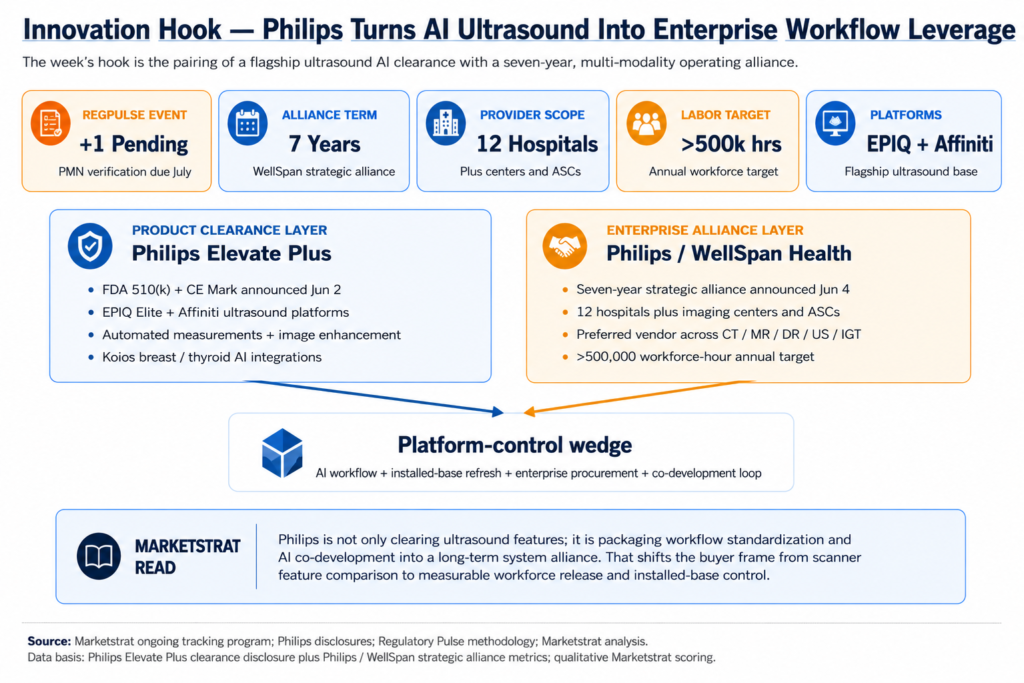

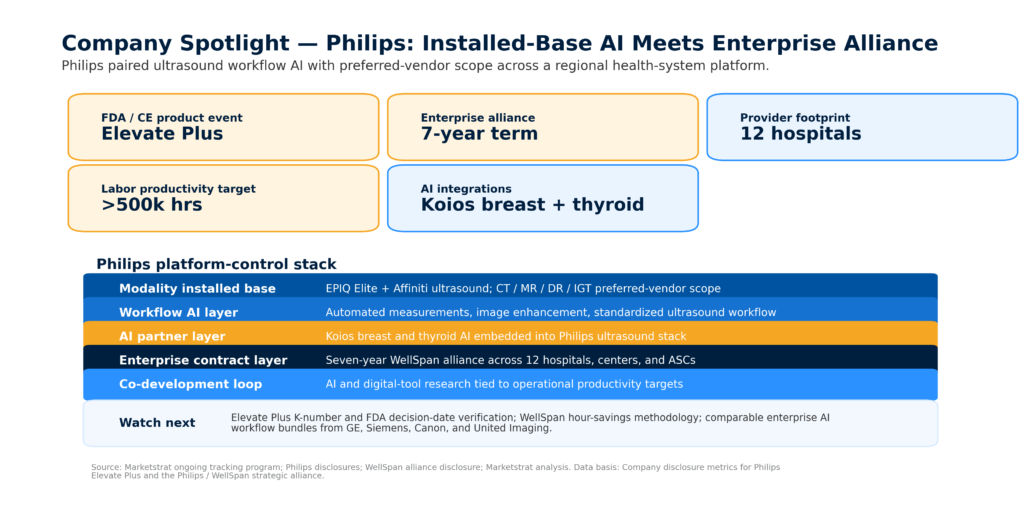

Philips made ultrasound AI part of an enterprise procurement story

Philips was the clearest structural signal of the week.

The company received FDA 510(k) clearance and CE Mark for Elevate Plus on EPIQ Elite and Affiniti ultrasound platforms. The product brings AI-enabled measurement automation, image enhancement, and Koios breast and thyroid AI integrations into Philips’ flagship general-imaging ultrasound systems.

That would have been meaningful on its own. But the same week, Philips and WellSpan Health announced a seven-year strategic alliance that covers imaging, patient monitoring, informatics, AI co-development, and preferred-vendor scope across CT, MR, digital X-ray, ultrasound, and image-guided therapy.

The combination changes the commercial frame. Philips is not only adding AI to ultrasound. It is connecting AI-enabled workflow automation to a broader enterprise operating model.

For health systems, that matters because ultrasound is labor-dependent, highly variable across operators, and often exposed to capacity pressure. Workflow automation becomes more valuable when it can be deployed across an installed base and tied to productivity goals.

GE HealthCare moved AI deeper into oncology workflow

GE HealthCare’s FDA clearance for MIM Contour ProtégéAI+ 2.0 is a different but related signal. The system targets AI-enabled auto-contouring in radiation therapy planning, including MR Brain and CT Male Pelvis models.

This is not generic AI. It addresses a specific operational bottleneck in oncology care: treatment-planning labor.

Radiation oncology workflows depend on contouring accuracy, review burden, consistency, and planning turnaround. If AI sits inside that workflow and reduces manual burden without introducing excessive edit time, it can become a durable software layer.

The broader read-through is that imaging AI is moving toward defined workflow economics. Tools that compress measurable bottlenecks are likely to have a clearer adoption path than tools that require users to leave their workflow or justify a standalone use case.

Nuclear medicine is becoming an operating-system market

Nuclear medicine was another high-signal lane.

Lantheus’ 18F-GP1 PET/CT won SNMMI Image of the Year for thrombus imaging. Telix and United Imaging announced a U.S. theranostics collaboration. GE HealthCare highlighted nuclear medicine software and workflow strategy. RMTA raised concerns about PET drug manufacturing friction.

These events are different in form, but they share one commercial implication: nuclear medicine and theranostics are becoming operating-system markets.

The scarce asset is not only the tracer or the scanner. It is the coordinated pathway across patient scheduling, tracer supply, scanner time, quantitative software, radiation safety, oncology referrals, and provider capacity.

That is why PET capacity and radiopharmaceutical logistics increasingly belong in the same strategic conversation.

Capital is still targeting workflow and access control

The week also showed that capital remains available for companies that control deployment surfaces.

Subtle Medical raised $33 million in growth capital and named Ohad Arazi CEO, building on the prior week’s PET clearance narrative. RadNet proposed a $200 million incremental term loan intended for acquisitions, organic expansion, health-system partnerships, and technology platforms. Lumexa and Hospital for Special Surgery formed an outpatient musculoskeletal imaging joint venture.

These signals show that imaging access, throughput, and deployment channels remain investable. AI matters more when it has a clear path into scanners, reports, patient flow, or provider networks.

Policy is tightening around compliance and evidence

Policy signals were mixed. Aetna’s planned 15% payment reduction for certain CT services billed with modifier CT places pressure on legacy CT economics. ACR appropriateness updates and SCCT / SCAI consensus guidance for FFR-CT reinforce the importance of clinical standards, protocol discipline, and evidence-backed utilization.

The takeaway is not that reimbursement is uniformly favorable or unfavorable. It is that the policy environment increasingly rewards compliant infrastructure, clear documentation, and standardized pathways.

For providers, that adds a new layer to capital planning. Legacy equipment, weak documentation, and inconsistent protocols can become revenue risks.

The next phase of imaging AI will not be won by the most novel algorithm alone. It will be won by the platforms that control workflow, capacity, evidence, reimbursement exposure, and distribution.

What to watch next

The near-term watchlist is practical.

First, whether Philips and WellSpan can translate the 500,000 workforce-hour target into auditable operating metrics. Second, whether GE HealthCare can use MIM workflow integration to expand software attach in oncology. Third, whether nuclear medicine capacity constraints create more scanner, tracer, and software partnerships. Fourth, whether outpatient imaging platforms continue to use debt, JVs, and AI deployment to consolidate referral access.

Related research themes

- Imaging AI workflow adoption

- Enterprise imaging IT and reporting infrastructure

- Nuclear medicine and theranostics capacity

- Outpatient imaging consolidation

- FDA 510(k) and AI-enabled medical devices

- Imaging reimbursement and CT compliance

- Procedure-suite imaging and MIS adjacency

Subscribe to The Marketstrat Pulse for weekly analysis of medical imaging AI, enterprise imaging, nuclear medicine, reimbursement, provider-platform strategy, and image-guided procedure markets: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.