ONE BIG THING

Imaging AI is rapidly consolidating into platform procurement (bundled clinical AI + viewer/reporting + governance), while OEM differentiation is shifting toward capacity math (speed, planning automation, fewer repeats)—and reimbursement risk is re-emerging as the most levered near-term constraint for brain MRI AI.

🎧 Listen to this week’s Marketstrat Pulse Insight on ECR 2026:

KEY TAKEAWAYS

- Fact: Consolidation accelerated: RadNet announced its acquisition of Gleamer, while Sectra entered into an agreement to acquire Oxipit. Interpretation: Distribution control is consolidating into fewer “AI operating systems,” increasing bundling power and raising the switching-cost stakes for point AI vendors.

- Fact: FDA activity concentrated around “time-to-action” problems, including non-contrast CT stroke triage and cardiac MR planning automation. Interpretation: The commercial wedge keeps shifting from abstract accuracy claims to measurable operations (queue prioritization, planning time, variability reduction), which aligns with CFO-led imaging procurement.

- Fact: A major evidence milestone landed: Perimeter Medical Imaging AI reported FDA PMA approval for its AI-enabled intraoperative breast margin assessment system. Interpretation: PMA-grade evidence has strategic “read-through” for surgical imaging and intraoperative decision support—expect more scrutiny on study design for any AI that claims to change surgical outcomes.

- Fact: ECR 2026 (Vienna) became an unusually dense “launch window” for throughput-oriented imaging. Philips positioned CT around speed/capacity, and Siemens Healthineers positioned angio around AI-guided planning + motion reduction. Interpretation: OEM storylines are converging on staffing constraints and schedule compression—not just hardware specs.

- Fact: Payment remains the swing variable: a MAC comment window is closing on a proposed noncoverage LCD for automated brain MRI AI, while CPT tracking momentum continues via a new Category III code. Interpretation: Coding progress ≠ reimbursement unlock; regional contractor posture can still chill adoption even when the technology is clinically plausible.

- Fact: MIS had two distinct signals: Intuitive consolidated distribution, and the UK executed its first remote robotic prostatectomy with low reported latency. Interpretation: Near-term telesurgery is niche, but it elevates a new procurement checklist (connectivity redundancy, security posture, failover ops) that will increasingly matter in robot selection.

QUICK-GLANCE TABLE

| Date | Headline | Our Take | Source |

| 2026-03-05 | Sectra to acquire Oxipit, bringing autonomous chest X-ray AI closer to PACS | This is the clearest new distribution signal of the week: autonomous normal-case clearance moves from stand-alone AI into the imaging IT stack, where renewal leverage is stronger. | S1 |

| 2026-03-06 | Philips wins FDA 510(k) for SmartHeart cardiac MR planning | SmartHeart matters because it monetizes MR capacity, not novelty; planning simplification is easier for providers to underwrite than a marginal image-quality claim. | S2 |

| 2026-03-05 | Philips launches Rembra CT at ECR 2026 | Rembra’s positioning is explicitly throughput-led. That matters because CT capital budgets are increasingly defended on access and utilization, not only on hardware spec escalation. | S3 |

| 2026-03-05 | Harrison.ai clears acute infarct triage on non-contrast CT brain | The commercial read-through is earlier triage in the stroke chain. Moving value upstream on NCCT broadens workflow impact relative to narrower downstream tools. | S4 |

| 2026-03-04 | Siemens launches AI-enabled angiography systems for liver embolization | This extends the same capacity thesis into interventional radiology: fewer workflow breaks, better planning, and potentially fewer repeat scans in high-skill, labor-constrained settings. | S5 |

| 2026-03-04 | DeepHealth unveils integrated native clinical AI portfolio at ECR | The point is not portfolio breadth alone; it is RadNet/DeepHealth’s effort to sell AI as a unified enterprise layer across modalities and workflows. | S6 |

| 2026-03-02 | RadNet closes Gleamer acquisition | The deal remains a structural benchmark for platform consolidation, but readers should see Marketstrat’s dedicated research for the full analysis. See Marketstrat’s research note on this acquisition on AlphaSense. | S7 |

| 2026-03-02 | Bracco launches AiMIFY in the EU and partners with Avicenna.AI | Bracco is testing whether contrast leadership can be extended into software attach. That is strategically relevant because workflow ownership is creeping beyond traditional OEM and PACS boundaries. | S8 |

| 2026-03-03 | AIQ highlights new Category III CPT X567T for metastatic lesion heterogeneity | Coding progress matters, but this is still a tracking milestone rather than a payment unlock. Providers need reimbursement proof, not code presence alone. | S9 |

| 2026-03-02 | Intuitive completes southern Europe distributor acquisition | In MIS, this is a distribution-control move, not a clinical one. Direct channel ownership improves margin capture and competitive response as robotics competition broadens. | S10 |

| 2026-03-03 | Philips-led SHERPA begins seven clinical studies in AI-assisted MIS | MIS still needs evidence, and SHERPA is one of the week’s cleaner examples of workflow AI being pushed toward outcomes-grade validation instead of demo-stage enthusiasm. | S11 |

| 2026-03-02 | Medimaps and Radiobotics announce MSK imaging AI merger | MSK AI is consolidating around workflow ecosystems instead of point apps, especially where X-ray triage and bone-health analytics can be sold together. | S12 |

| 2026-03-05 | iMerit, Segmed, and Advocate Health release annotated DBT dataset | Lower on immediate commercial impact, but open clinical-grade data can shorten development cycles and intensify competition in breast imaging AI. | S13 |

| 2026-03-02 | FDA De Novo listing highlights Ultrasound AI’s Delivery Date AI | The decision predates the week, but the March 2 database refresh is worth noting because a De Novo matters more strategically than another routine 510(k). | S14 |

| 2026-03-06 | Perimeter Medical PMA (Claire, intraoperative breast margin assessment) | PMA-grade evidence has strategic “read-through” for surgical imaging and intraoperative decision support | S14 |

Source Key

S1 — Sectra, Mar. 5, 2026 — Oxipit acquisition

S2 — Philips, Mar. 6, 2026 — SmartHeart FDA 510(k)

S3 — Philips, Mar. 5, 2026 — Rembra CT at ECR

S4 — Business Wire / Harrison.ai, Mar. 5, 2026 — NCCT infarct triage clearance

S5 — Siemens Healthineers, Mar. 4, 2026 — AI-enabled angiography systems

S6 — DeepHealth, Mar. 4, 2026 — native clinical AI portfolio at ECR

S7 — DeepHealth, Mar. 2, 2026 — RadNet acquires Gleamer

S8 — Bracco, Mar. 2, 2026 — AiMIFY EU launch / Avicenna.AI partnership

S9 — PR Newswire / AIQ Solutions, Mar. 3, 2026 — Category III CPT X567T

S10 — MedTech Dive, Mar. 2, 2026 — Intuitive southern Europe distribution move

S11 — Philips, Mar. 3, 2026 — SHERPA clinical studies

S12 — Radiobotics, Mar. 2, 2026 — Medimaps/Radiobotics merger

S13 — iMerit, Mar. 5, 2026 — annotated 3D mammogram dataset

S14 — FDA De Novo database, page updated Mar. 2, 2026 — Delivery Date AI / DEN250007

S15 — Perimeter Medical PMA

INNOVATION HOOK

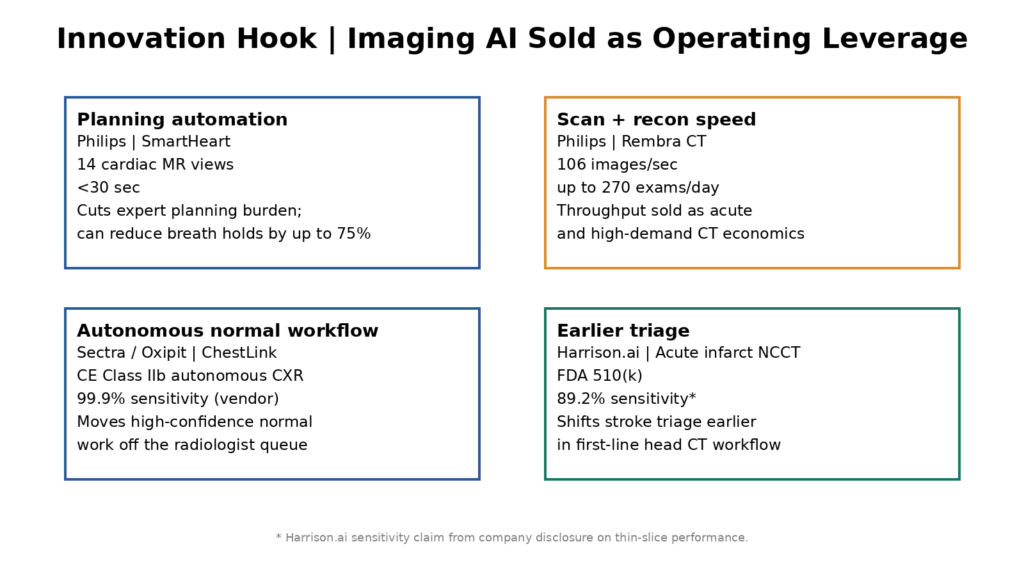

Imaging AI sold as operating leverage

At ECR 2026 and in adjacent clearance news, the highest-signal theme was not another point algorithm but time reclaimed from the imaging chain. Philips SmartHeart automates 14 cardiac MR views in under 30 seconds and is positioned to reduce breath holds by up to 75%; Philips Rembra CT was launched around reconstruction speed and daily throughput; Sectra’s acquisition of Oxipit pulls autonomous normal chest X-ray workflow closer to the PACS stack; and Harrison.ai’s NCCT infarct clearance shifts triage earlier in stroke workflow. The commercial denominator is labor substitution and queue compression. That matters because vendors are now selling capacity with existing staff and installed base, which is a stronger budget narrative than standalone accuracy claims.

The Perimeter PMA is a reminder that the highest-signal AI wins are those attached to hard economics—repeat procedures, OR blocks, and pathology delay—not just incremental reader performance. The next question is scaling: training, adoption, and real-world re-excision impact.

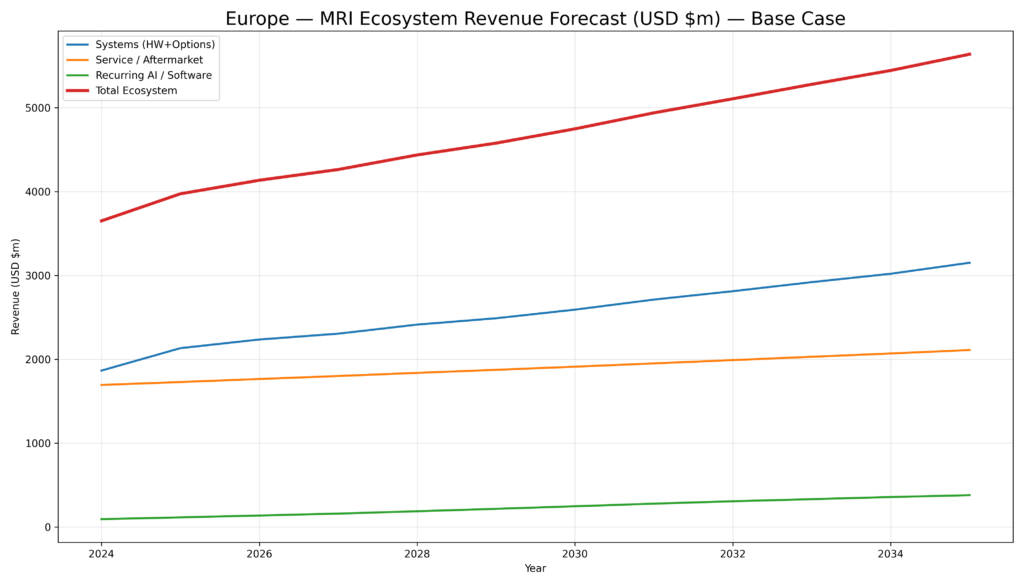

MARKET LENS – EUROPE MRI ECOSYSTEM MARKET

Europe is a large, high-quality MRI value pool, but it behaves like a mature fleet economy: unit growth is modest, while revenue growth is driven by mix, ASP, upgrades, and attach. Europe remains service-heavy (large installed base and service intensity), yet systems value grows faster than service because the market premiumizes toward higher-end 3T and “package-rich” configurations. AI becomes increasingly material as a recurring layer, but the primary near-term monetization lever is still workflow-linked productivity, not “AI as an isolated product.”

Europe increasingly rewards commercial architectures that bundle (1) premium hardware, (2) upgrade pathways, (3) service guarantees, and (4) AI/workflow modules into a single procurement story with measurable operational outcomes (capacity, uptime, standardization).

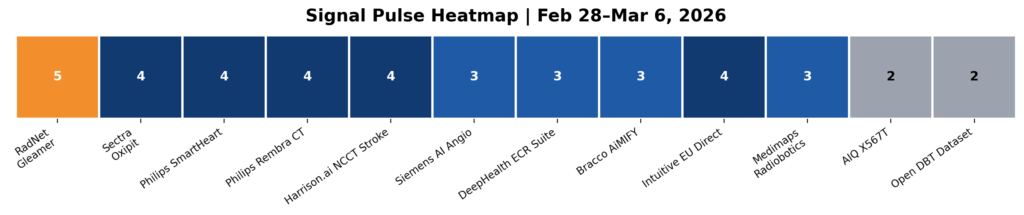

SIGNAL PULSE HEATMAP – FEB 28 – MAR 6, 2026

Event-level

The heatmap should be read as a 12–24 month impact screen, not a popularity contest. This week’s highest-scoring cells cluster around two themes: control of distribution surfaces and measurable operating leverage. RadNet/Gleamer remains the structural benchmark but is not the new thesis this week; the fresher signals are Sectra/Oxipit, Philips SmartHeart, Philips Rembra CT, Intuitive’s southern Europe direct move, and Harrison.ai’s NCCT stroke triage clearance. Mid-tier items such as DeepHealth’s ECR portfolio expansion, Siemens’ AI-guided angio launch, and Bracco’s AiMIFY push matter because they reinforce the same direction of travel. Lower-tier items like the AIQ Category III code and the open DBT dataset are strategically relevant, but they do not yet shift near-term market structure.

This week’s score concentration sits where platform control meets operating economics. The strongest signals were not isolated product launches; they were moves that tighten workflow control or create measurable capacity with existing staff and installed base.

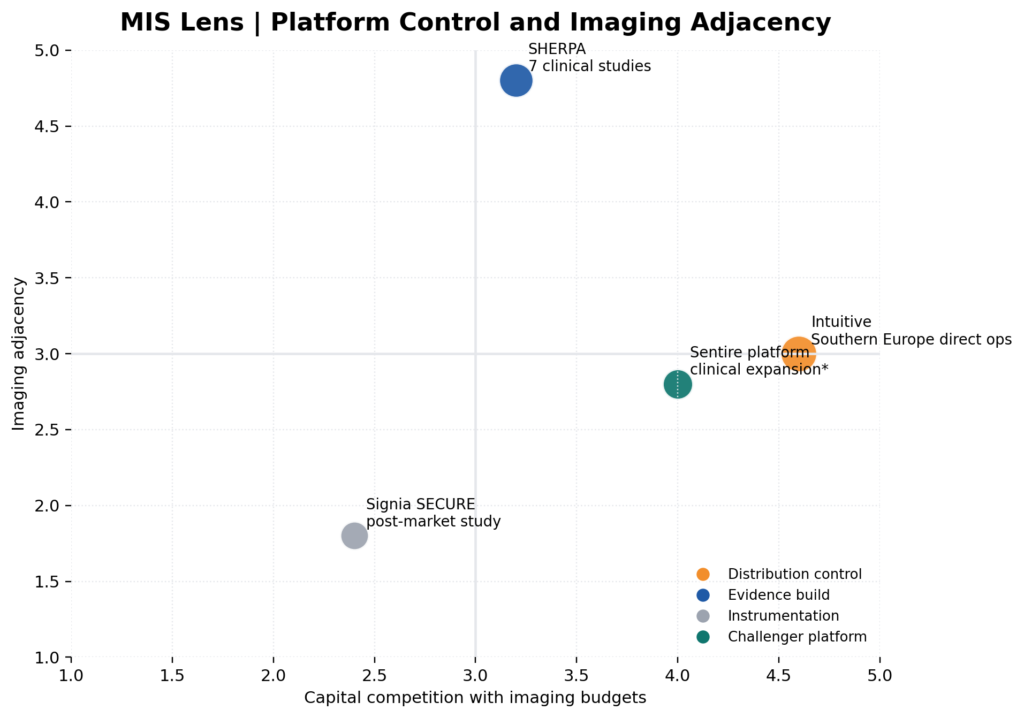

MINIMALLY INVASIVE SURGERY (MIS LENS)

The MIS lens is active this week because the same commercial playbook showing up in imaging AI is now visible in robotics and image-guided therapy. Intuitive’s completion of its southern Europe distributor acquisition is a direct channel-control move, not a clinical novelty story. Philips-led SHERPA, by contrast, is an evidence-building program for AI- and robotics-assisted minimally invasive treatment in neurovascular and liver interventions. Together they show the two routes to scale in MIS: own the channel or build the evidence. Both compete with imaging modernization for the same capital envelope, and both rely increasingly on imaging-guided planning, visualization, and post-procedure follow-up. That makes MIS relevant to imaging readers even in weeks when radiology dominates the headline flow.

MIS matters here because it is running the same playbook as imaging AI: distribution control, workflow automation, and evidence generation — all competing for the same hospital capital envelope.

MARKETSTRAT POV

- Providers should treat “platform consolidation” as a procurement risk and an opportunity: fewer integrations can reduce IT overhead, but vendors will push bundling and multi-year terms. Counter with modular pricing, measurable throughput KPIs, and explicit exit clauses tied to clinical adoption.

- OEMs are successfully reframing capex as capacity unlock—buyers will insist that throughput claims be validated on site-specific constraints (staffing, protocol mix, scheduling), and demand a “deployment playbook” with staffing and protocol assumptions, not just physics specs.

- AI vendors without distribution should assume spreadsheet reality: IDNs increasingly want one integration and governance tooling. If you’re not inside PACS/enterprise imaging, partnerships that embed into existing workflow are becoming the shortest path to revenue.

- Payer posture remains the most asymmetric risk. MAC LCD activity around brain MRI AI shows that “clinically plausible” is not enough; vendors should prioritize outcomes-grade and multi-site evidence designed for coverage language (utility, not accuracy).

- MIS adoption is splitting into two tracks: (1) consolidation of channel control and service footprint; (2) early infrastructure experiments (telesurgery). Hospitals should anticipate new due diligence around cyber/latency/redundancy and build those into robot tenders now.

The complete Marketstrat Research Note is available on AlphaSense – – with the full analytical toolkit, including all frameworks including Signal Radar, Supply Chain Sensitivity, Supply Chain Sensitivity, Imaging Capacity Model, EVI, and more.

About Marketstrat

Marketstrat® is a market intelligence and GTM enablement firm committed to empowering clients in data-driven industries. Under the Markintel™ brand, it delivers robust market intelligence, while GrowthEngine solutions offer specialized GTM advisory and app-based tools—together fueling growth, innovation, and competitive advantage. For more information, visit www.marketstrat.com.

Marketstrat® is a registered trademark and Markintel™ is a pending trademark of Marketstrat.

Check out free Research and Insights and Analysis of Industry Events

Check out our collection of Markintel Horizon and Markintel Pulse research.

Check out details on our reports, World Market for AI in Medical Imaging World Market for Oncology Imaging AI and other Pulse Reports in the Imaging space.