This week’s medical imaging AI signal was not another model launch. It was the market moving toward reimbursable, governed, and routed workflow infrastructure.

🎧 Listen to this week’s Marketstrat Pulse Insight:

The medical imaging AI market is entering a more disciplined phase.

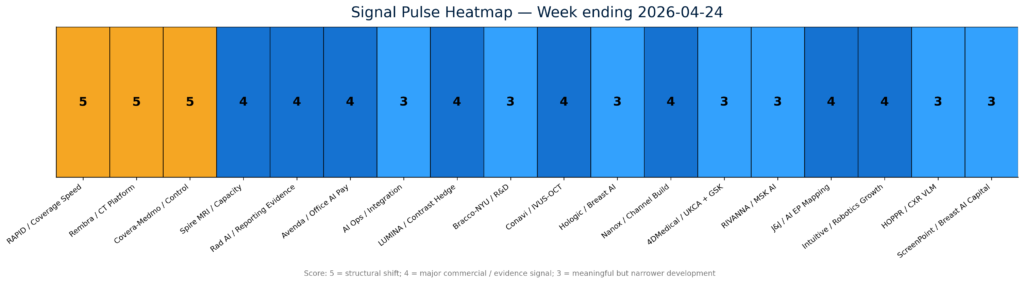

For the past several years, the category has been defined by algorithm count, FDA clearances, model accuracy, and pilot adoption. Those still matter. But this week’s strongest signals point to a different commercial hierarchy: coverage speed, workflow ownership, and measurable operational impact are becoming the new moats.The highest-signal developments clustered around reimbursement acceleration, order-to-read platform control, domain-specific AI evidence, and measurable MRI throughput.

The highest-signal developments clustered around reimbursement acceleration, order-to-read platform control, domain-specific AI evidence, and measurable MRI throughput.

The most important policy development was the CMS/FDA launch of the RAPID coverage pathway, which is designed to align FDA market authorization for eligible Breakthrough Devices with a faster Medicare National Coverage Determination process. CMS says the pathway could enable national coverage and payment as soon as roughly two months after market authorization for qualifying Class II and Class III Breakthrough Devices, compared with roughly a year or more under prior coverage routes. TCET is also being paused for new candidates as RAPID moves forward.

RAPID changes the commercialization clock for eligible Breakthrough Devices by aligning FDA authorization with Medicare national coverage development.

That matters for imaging AI and AI-enabled medtech because reimbursement lag has often been the real commercialization bottleneck. FDA clearance may create market access, but predictable payment creates budgetability. For venture-backed device companies, AI imaging vendors, and hospital capital committees, RAPID could make the reimbursement pathway more visible earlier in product development—especially when pivotal studies are designed with Medicare-relevant outcomes in mind.

The second major signal was platform control. Covera Health and Medmo Medmo combined to form an end-to-end diagnostic imaging management platform that links ordering, patient routing, site selection, study completion, and diagnostic intelligence. The strategic read-through is straightforward: imaging AI vendors increasingly need access to the workflow surfaces where studies are ordered, routed, interpreted, and paid. It is not enough to sit outside the operating layer and claim better performance. The route to the scan is becoming as important as the model attached to the scan.

The third signal came from evidence. Rad AI’s peer-reviewed study in npj Digital Medicine showed that domain-specific AI generated radiology impressions that were better aligned with radiologist expectations than general-purpose LLMs. The study reinforces an emerging procurement standard: healthcare buyers are not simply asking whether AI can generate fluent text; they are asking whether it fits specialty workflow, communication norms, safety expectations, and clinical usability.

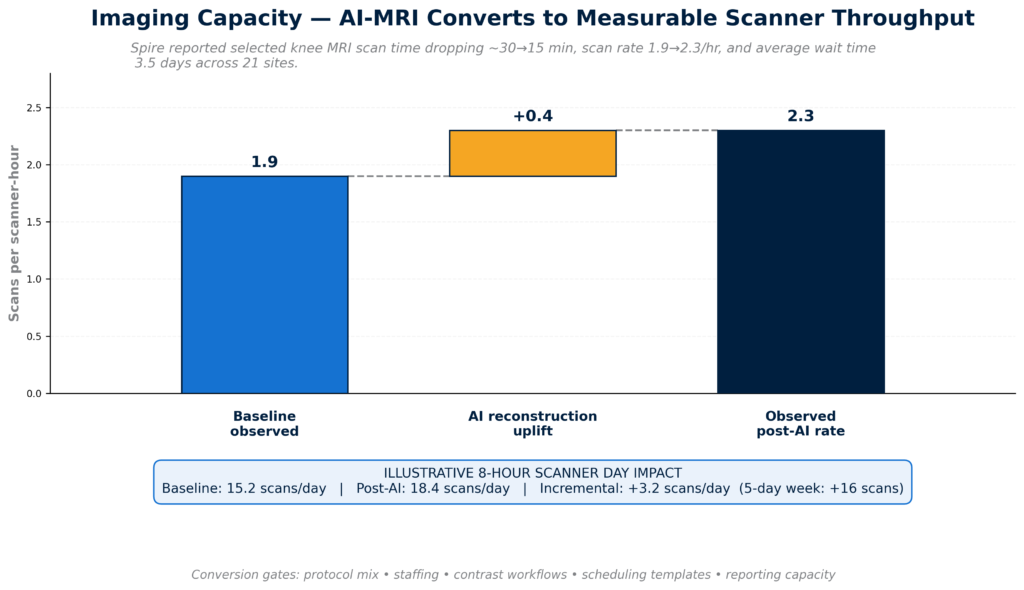

Capacity was the fourth theme. Spire Healthcare Group plc reported enterprise-scale AI-MRI deployment results across 21 UK hospital sites, including materially shorter knee MRI scan times and improved scan rates. This kind of real-world throughput evidence is commercially important because it links AI to a capacity problem providers already understand: scanner demand, staffing constraints, and wait times. AI that helps convert the same installed base into more usable capacity is easier to defend than AI sold only as abstract productivity software.

The strongest capacity signals came from AI that expands throughput inside existing infrastructure rather than requiring new modality capital.

Several adjacent developments reinforced the same market direction. Avenda Health expanded Medicare office-setting reimbursement for Unfold AI across seven western states. DeepTek and deepc launched an integrated radiology AI operating environment, underscoring the move from point algorithms to orchestration layers. GE HealthCare dosed the first patient in its LUMINA Phase 2/3 trial for mangaciclanol, a manganese-based MRI contrast agent, while Bracco Imaging and NYU Langone announced a multi-year imaging research alliance across MRI, photon-counting CT, ultrasound, and AI-enabled PET/CT.

The broader takeaway: imaging AI is not becoming less strategic. It is becoming more commercially demanding.

The market is starting to separate three categories:

First, reimbursable AI that can attach to defined payment pathways or accelerate coverage timing.

Second, routed AI that sits inside order capture, referral management, PACS, modality, reporting, or payer workflows.

Third, measurable AI that can show hard effects on throughput, turnaround time, utilization, quality, or downstream cost.

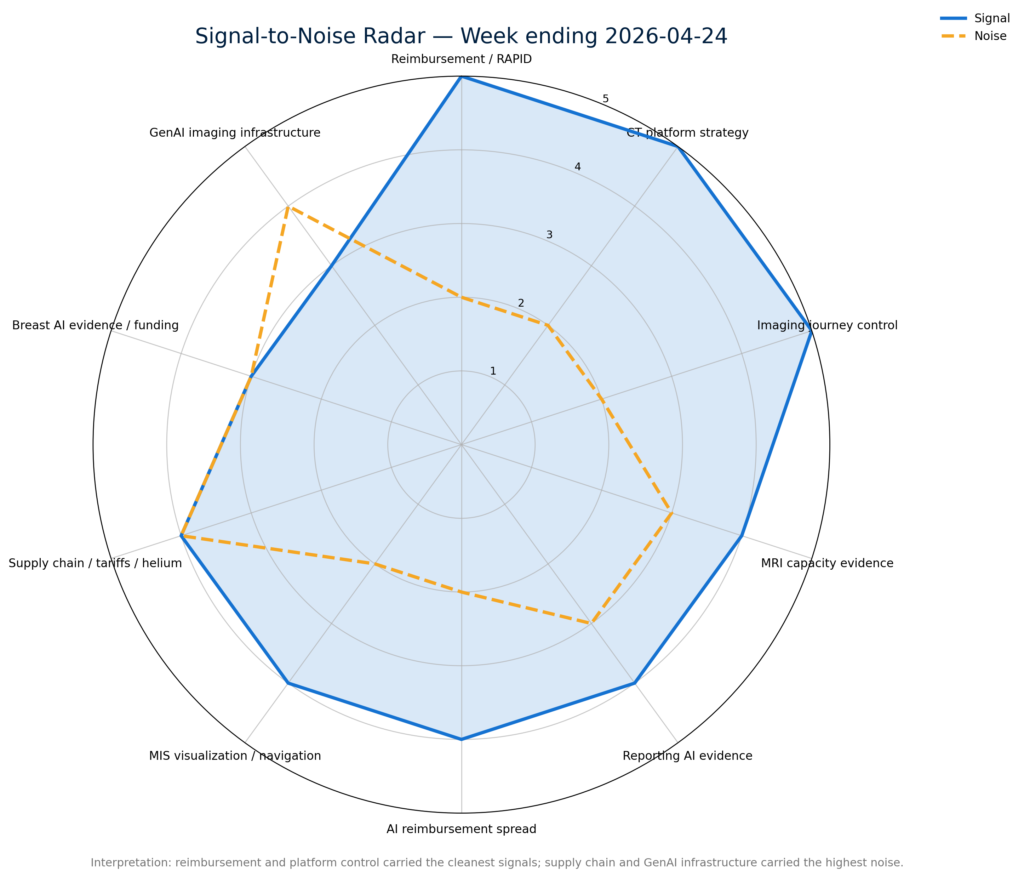

Signal outran noise where AI was reimbursable, platform-routed, or supported by real-world operational evidence.

Everything else will face tougher scrutiny.

For health systems, this means AI evaluation should move beyond model accuracy into four questions: Does it create billable value? Does it reduce a measurable bottleneck? Does it fit the existing workflow surface? Does it generate evidence that a value-analysis committee can actually use?

For vendors, the implication is sharper: model quality is necessary but no longer sufficient. The commercial winner will be the company that can pair validated performance with reimbursement strategy, workflow integration, governance, and distribution.

That is the shift this week’s Markintel Pulse focuses on: imaging AI is moving from point-model promise to reimbursable, routed, and evidence-backed infrastructure.

Subscribe to our newsletter on LinkedIn: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.

All Marketstrat® research products are developed through Markintel®, our proprietary methodology and workflow system for producing decision-grade market intelligence.

Contact

marketstrat.com | research@marketstrat.com