I-MED’s A$3.4B sale, SubtleHD(PET)’s FDA clearance, CBCT perfusion, cloud-native teleradiology, and payer friction relief point to a market valuing infrastructure over standalone AI.

🎧 Listen to this week’s Marketstrat Pulse Insight:

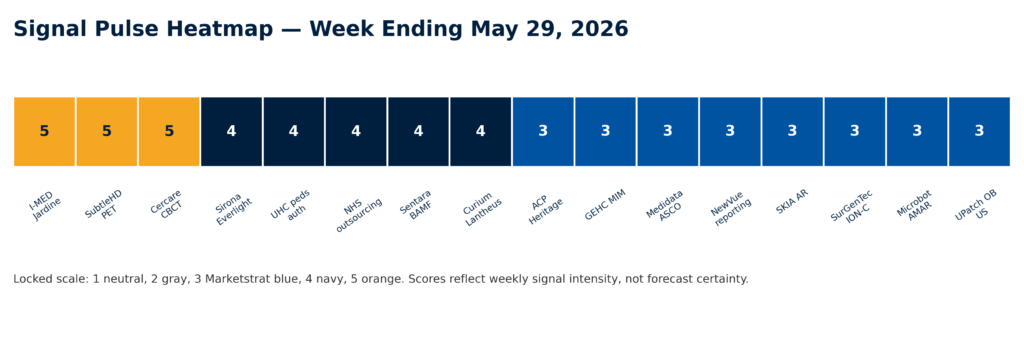

The latest Marketstrat Pulse highlights a shift in medical imaging: the strongest commercial signals are clustering around assets that control bottlenecks. Jardine Matheson’s A$3.4B I-MED transaction, Subtle Medical’s SubtleHD(PET) clearance, Cercare’s CBCT Perfusion clearance, Sirona / Everlight’s cloud-native teleradiology partnership, and UnitedHealthcare’s pediatric prior-auth rollback all point to a market repricing access, throughput, read capacity, and workflow infrastructure.

ther an algorithm can detect a finding or whether a scanner produces better images.

The more important question is becoming: what bottleneck does the asset control?

This week’s Marketstrat Pulse points to a clear pattern. Imaging value is concentrating around scaled access networks, scanner productivity software, cloud-native interpretation infrastructure, direct-to-procedure imaging, and lower-friction reimbursement workflows.

That does not mean diagnostic AI is becoming less relevant. It means the commercial bar is higher. The most valuable tools are those that can translate AI, software, or platform scale into measurable operating leverage.

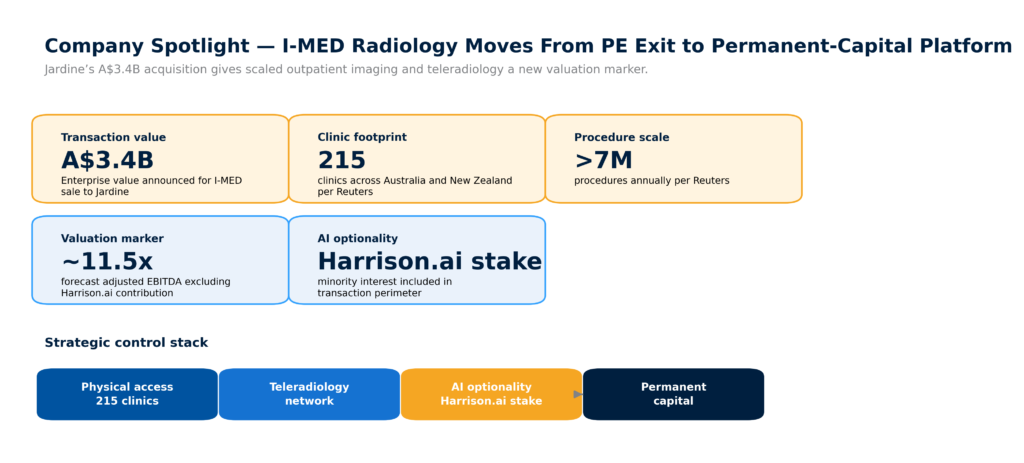

I-MED puts a price on imaging platform control

The week’s largest structural signal was Jardine Matheson’s agreement to acquire I-MED Radiology Network for A$3.4 billion.

I-MED is not just a collection of imaging centers. It is a scaled outpatient imaging and teleradiology platform with a broad modality footprint, millions of annual procedures, and a minority stake in Harrison.ai.

For strategic buyers, OEMs, AI vendors, and investors, the transaction reinforces a core point: scaled imaging networks control more than patient access. They influence scanner utilization, procurement leverage, data density, read workflow, AI distribution, and payer contracting power.

That combination is increasingly scarce.

The transaction also shows why permanent capital may become more active in diagnostic infrastructure. Imaging platforms can generate durable demand, but they also require long-horizon investment in technology, staffing, workflow, and network expansion.

Marketstrat visual on Jardine Matheson acquisition of I-MED Radiology Network and imaging platform control

I-MED’s A$3.4B transaction highlights the strategic value of scaled imaging access, teleradiology, and AI optionality

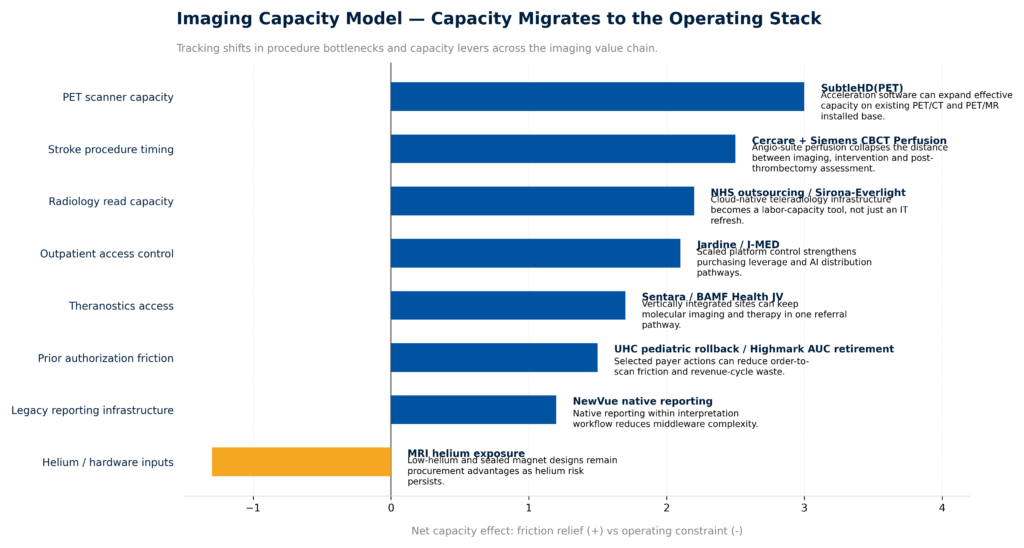

PET AI becomes capacity software

Subtle Medical’s FDA clearance for SubtleHD(PET) was the counted RegPulse AI radiology event for the week. The company says the software supports PET/CT and PET/MR systems, works across FDA-approved radiotracers, and can enable up to 75% faster PET imaging on existing scanners.

The important point is not just image enhancement.

PET capacity is becoming more strategically important as molecular imaging, radiopharmaceuticals, and theranostics grow. A site can add PET capacity by buying another scanner, but that path requires capital, space, staffing, scheduling, and radiopharmacy support. Capacity software offers a different lever: increase effective throughput on the installed base.

That makes SubtleHD(PET) commercially relevant beyond the radiology AI category. It belongs in the same conversation as PET utilization, oncology pathway access, theranostics readiness, and nuclear medicine infrastructure.

Stroke workflow moves closer to the angio suite

Cercare Medical received FDA 510(k) clearance for CBCT Perfusion, and Siemens Healthineers and Cercare announced a global collaboration around cone-beam CT perfusion-guided stroke treatment.

This is another example of capacity and workflow moving closer to the point of care. In acute stroke, time is not an abstract operating metric. The physical separation between imaging, decision-making, and intervention can affect workflow efficiency and treatment timing.

CBCT perfusion places advanced imaging analysis closer to the procedure suite. For OEMs, that supports a broader strategy: sell not only the imaging system, but the clinical workflow around the system.

For hospitals, the value case will depend on local stroke pathways, interventional volumes, training, and integration into existing neurovascular workflows. But the direction is clear: image analysis is increasingly embedded into procedural environments.

Read capacity becomes visible in operating dollars

The read-capacity constraint was also visible this week. The Guardian reported that NHS spending on outsourced CT and MRI scan interpretation reached £241 million in 2025.

That figure matters because it converts a widely discussed workforce shortage into an operating-cost signal. Radiology read capacity is not just a staffing issue. It shapes turnaround times, outsourcing dependence, worklist design, AI adoption, and teleradiology platform demand.

Sirona Medical and Everlight Radiology’s five-year cloud-native platform agreement fits directly into this trend. Large reading networks need systems that can support assignment, interpretation, reporting, quality management, and AI orchestration at scale.

NewVue’s native AI-driven reporting launch points in the same direction. Reporting is becoming part of the operating layer, not just a downstream documentation step.

Imaging capacity is migrating across scanner productivity, procedure workflow, cloud reads, and reimbursement friction.

Reimbursement friction eases selectively

UnitedHealthcare said it will remove prior authorization for nearly two-thirds of services for members under 18 by the end of 2026. Highmark also retired its advanced-imaging Appropriate Use Criteria policy, while CMS claims-attachment standards became effective.

These are not sweeping reimbursement expansions. The better interpretation is more measured: selected forms of administrative friction are becoming harder to defend.

For imaging providers, reduced friction can improve scheduling, documentation burden, and revenue-cycle execution. For vendors, the message is that workflow value includes payer-facing and claims-facing efficiency, not just clinical performance.

Weekly signal intensity clustered around platform control, PET capacity, and direct-to-angio workflow.

Marketstrat POV

Imaging infrastructure is being repriced because the market is rewarding assets that control real constraints.

The relevant constraints include:

- Patient access

- PET scanner time

- Read capacity

- Teleradiology workflow

- Procedure-suite imaging

- Radiopharmacy logistics

- Prior authorization and documentation friction

- Reporting productivity

The strongest companies and platforms will not be defined only by detection performance or scanner specifications. They will be defined by how much operating leverage they create inside constrained imaging pathways.

The most valuable imaging assets are increasingly the ones that control bottlenecks: access, throughput, read capacity, payer friction, and procedure workflow.

For weekly market intelligence across medical imaging, radiology AI, enterprise imaging, reimbursement, provider consolidation, and adjacent MedTech markets, subscribe to The Marketstrat Pulse: https://www.linkedin.com/newsletters/the-marketstrat-pulse-7426689322839588864/

Related research themes

- Medical imaging AI commercialization

- Enterprise imaging and cloud-native PACS

- Radiology workflow and read-capacity constraints

- PET/CT and theranostics infrastructure

- Provider consolidation and imaging platform strategy

- Imaging reimbursement and prior authorization

- Image-guided procedure workflow

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.