AI breaks out of the lab—and into clinical ops, policy, and even the iPhone. May 16, 2025.

One Big Thing

In one seven-day span we saw:

- FDA green-lights its first agency-wide generative-AI rollout to accelerate device, drug, and biologic reviews — a potential game-changer for submission timelines.

- GE HealthCare and United Imaging deploy deep-learning upgrades that clean up cone-beam CT and add voice-controlled angiography, setting a new bar for interventional imaging UX.

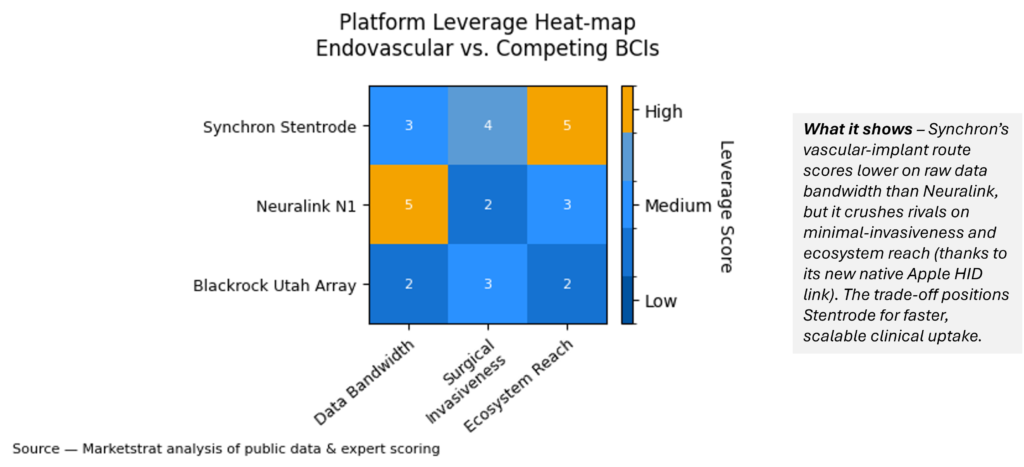

- Synchron’s Stentrode™ gains “native” HID integration with Apple devices, signaling that brain-computer interfaces (BCIs) are poised to leap from assistive tech to mainstream human-device interaction.

Why it matters: Clinical, regulatory, and consumer frontiers converged this week—underscoring that competitive advantage now hinges on execution speed in AI adoption and ecosystem partnerships rather than on algorithms alone.

Signal Pulse — Week ending May 16, 2025

Quick-Glance Grid

| Category | Headline (Date) | So What? |

|---|---|---|

| Regulatory | FDA to scale gen-AI across all Centers by 30 Jun 25 | Shorter review clocks could pull forward revenue for novel devices. |

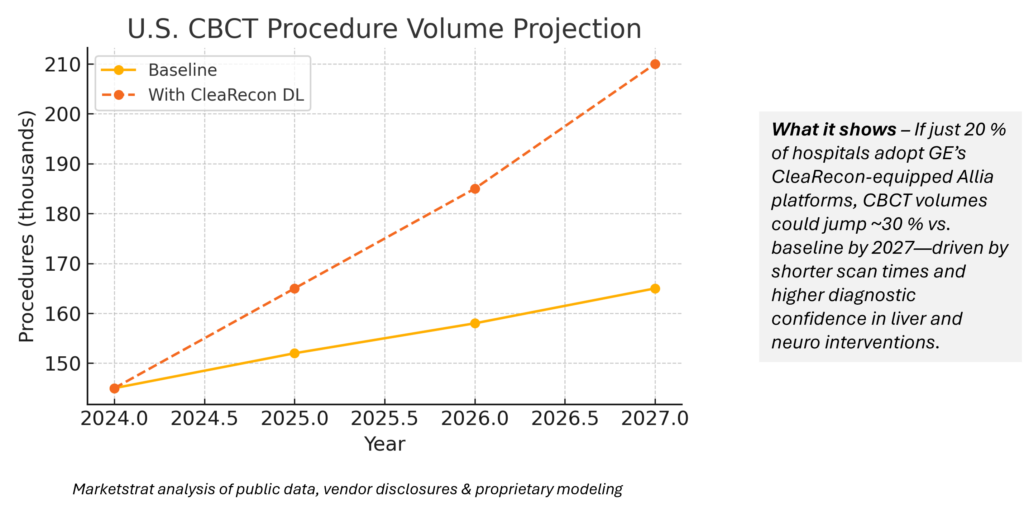

| Approvals | CleaRecon DL wins 510(k) & CE Mark (GE) | 98 % of cases clearer CBCT → higher confidence in liver & neuro interventions. |

| Approvals | uAngio AVIVA (United Imaging) cleared | First 8-axis, voice-assist angio lab hits U.S.; Chinese OEMs step on GE/Philips turf. |

| Product | Philips × NVIDIA to build MRI foundation model | Zero-click planning + noise-free scans aim to cut table time 30–50 %. |

| Mfg / Tariffs | Siemens pumps $150 M into U.S. Varian factory | Onshoring offsets €200-300 M tariff hit & wins “Made in USA” tenders. |

| BCI | Synchron–Apple native link | Endovascular BCI as new UI layer; Morgan Stanley pegs BCI TAM at ~$400 B. |

| Funding | Chipiron raises €14 M for cryogen-free MRI | Ultra-low-field MRI on path to FDA trials in ’26; accessibility play. |

| Service | SimonMed rolls out AI-enhanced DEXA + TBS | Picks up 30 % more osteoporosis-risk pts without cap-ex spike. |

| Research | EXPLORER total-body PET cut to 20 min | DL noise-reduction unlocks routine parametric PET. |

| Earnings | Philips says >50 % of sales now AI-driven | Software margin helps offset litigation-related cash drag. |

Deeper Dive

1. AI Turbo-charges the Interventional Suite

What happened

- CleaRecon DL: GE’s DL algorithm wipes out streak artifacts in cone-beam CT; 94 % of readers report higher diagnostic confidence.

- uAngio AVIVA: United Imaging brings voice commands + 8-axis robotics to cath labs, with low-dose uVERA IQ reconstruction.

Why it matters

- Clinical ROI: Cleaner CBCT means fewer DSA cross-checks, up to 5 min shaved per complex embolization.

- Competitive shake-up: Chinese OEMs now compete on workflow, not just price, pushing incumbents toward similar hands-free UX.

Marketstrat angle: Our GTM Growth-Maturity quadrants (AI Imaging Part 5) flagged interventional AI as early-growth; this week’s launches validate that thesis and will feed our updated attach-rate benchmarks.

2. Tech-Medtech Convergence Goes Mainstream

Synchron × Apple

- First OS-level HID for neural input → instant addressable market of 1.3 B iOS devices.

- Early clinical roll-out to current Stentrode™ trial participants H2’25.

Philips × NVIDIA MRI model

- Building a 3-D foundation model (VISTA-3D + MAISI) to enable “zero-click” scan planning and synthetic contrast.

Implications

- Platform lock-in: OEMs bundling proprietary AI tighten moats; standalone algorithm vendors must pivot to API/plug-in plays.

- BCI ethics on clock: Mainstream branding accelerates regulators’ need for neural-data rules; we expect draft FDA “AI transparency label” guidance by Q3.

3. Policy & Supply-Chain Watch

- FDA AI rollout led by new CAIO Jeremy Walsh; generative AI turned a week-long review task into “minutes.”

- Tariff drag forces Siemens to shift Varian Linac builds from Mexico to California; similar moves signaled by GE HealthCare.

Stakeholder impact

| Stakeholder | Upside | Risk |

|---|---|---|

| Start-ups | Faster 510(k) clocks; narrative tailwind for AI raises | Tougher bias / real-world-evidence audits |

| Health systems | Onshore supply reduces 12-week linac back-orders | Higher ASPs as OEMs pass through U.S. labor costs |

| Investors | Policy clarity de-risks AI theses | Earnings volatility from tariff pass-through |

Takeaway: AI’s center of gravity is shifting from isolated algorithms to end-to-end experience layers—in the cath-lab, on the scanner console, and soon on your phone.

Marketstrat POV: Providers planning FY-26 cap-ex should budget for AI-embedded upgrades rather than bolt-ons, and start building AI governance playbooks now that the FDA is, too.

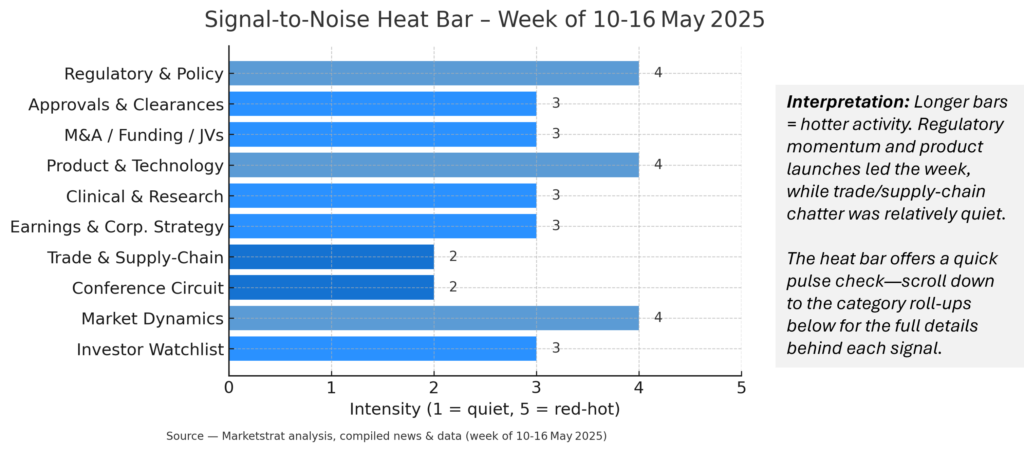

Signal Pulse — Week ending May 16, 2025

- Regulatory & Policy – Momentum builds toward global AI rule-books: FDA draft SaMD guidance, UK MHRA PMS rules (go live 16 Jun 25), and EU IVDR final deadline (26 May 25) all converge on greater post-market evidence and transparency—expect compliance spend to tick up 15-20 % for exporters.

- Approvals & Clearances – AI now table stakes: 8 additional FDA/CE wins—ranging from BrightHeart’s fetal-echo assist to Nanox ARC-X tomosynthesis—confirm that every new imaging modality seeks an AI differentiator.

- M&A, Funding, JVs – Selective capital returns: €27 M for Gleamer, €14 M for Chipiron, plus Optellum-BMS lung-cancer pact show investors shifting to disease-specific scale-ups rather than broad AI point tools.

- Product & Technology – Workflow supremacy theme: Philips’ SmartSpeed Precise (3× faster MR), Carestream’s Focus HD detector, and Fujifilm’s award-winning enteroscope all tout time-to-diagnosis wins over raw image specs.

- Clinical & Research – Evidence climbs: Perimeter’s OCT-AI breast-margin trial hit endpoints; EXPLORER total-body PET cut scan time to 20 min, underscoring real-world AI efficiency data regulators crave.

- Earnings & Corporate Strategy – Tariff drag dominates calls (Siemens, Solventum) while Philips discloses >50 % AI revenue mix, validating software margins as hedge against hardware headwinds.

- Trade & Supply-Chain – AdvaMed lobbies for “zero-for-zero” tariffs; society statements warn isotope shortages. OEMs are re-routing production to NA/EU, a theme likely to persist into CY-26 budget cycles.

- Conference Circuit – Regional tech summits (Arizona Digital Health, LABEST Week) spotlight local AI ecosystems, hinting at decentralized innovation clusters feeding national roll-outs.

- Market Dynamics – Imaging TAM steady at 4.95 % CAGR, but AI sub-segment racing at 30 %+ through 2032; payer moves (CCTA reimbursement doubling) accelerate modality-specific growth pockets.

- Investor Watchlist – VC trackers show later-stage rounds recovering; early-stage remains thin → funding scarcity will favor start-ups with clinical evidence + clear regulatory path by Q4.

About Marketstrat™

Marketstrat™ is a market intelligence and GTM enablement firm committed to empowering clients in data-driven industries. Under the Markintel™ brand, it delivers robust market intelligence, while GrowthEngine™ solutions offer specialized GTM advisory and app-based tools—together fueling growth, innovation, and competitive advantage. For more information, visit www.marketstrat.com.

Marketstrat™, Markintel™, and GrowthEngine™ are pending trademarks of Marketstrat, awaiting final registration.

- Check out our collection of Markintel Horizon and Markintel Pulse research.

- Check out details on our upcoming report, World Market for AI in Medical Imaging

- Check out free Research and Insights and Analysis of Industry Events

FAQ

Q1. What is Cone-Beam CT (CBCT) and how is it used in interventional radiology?

A1. CBCT is a 3-D X-ray technique that rotates a cone-shaped beam around the patient, producing high-resolution volumes in under 30 seconds. Interventional teams use it to guide embolizations, spine hardware placement, and trauma repairs with lower dose than conventional CT.

Q2. How will the FDA’s new agency-wide generative-AI rollout affect device approvals?

A2. The FDA is piloting gen-AI to screen submissions and flag safety issues, a move that could shave weeks off 510(k) and De Novo reviews—accelerating time-to-market for AI-driven imaging devices.

Q3. Which imaging modalities show the fastest AI-adoption growth?

A3. Radiology still leads in cleared AI devices, but cardiology and pathology are growing fastest, expanding their share from <10 % in 2018 to ~15 % today.

Q4. Why are Chinese OEMs gaining ground in U.S. interventional imaging?

A4. Vendors like United Imaging combine advanced deep-learning reconstruction with lower price points, pressuring incumbents to match workflow features such as voice-controlled angio labs.

Q5. What does “platform leverage” mean for brain-computer interfaces (BCIs)?

A5. Platform leverage measures a BCI’s data bandwidth, surgical invasiveness, and ecosystem reach—key factors that determine how quickly the tech can scale beyond clinical trials.