April 18, 2025

The “One Big Thing”

Regulators green‑lighted a record seven imaging or therapeutic AI devices in one week while Congress introduced the bipartisan Health Tech Investment Act to guarantee Medicare payment for FDA‑cleared AI tools.

Translation: the two biggest barriers to clinical AI adoption—regulatory uncertainty and reimbursement—are falling in rapid succession. Market‑ready vendors now face a commercial land‑grab, and health‑system buyers must update capital‑planning roadmaps fast.

Quick‑Glance Scorecard

| Category | Headline | Why It Matters |

|---|---|---|

| FDA | HeartFocus AI ultrasound & Brainomix 360 stroke core among 5 clearances; Nanox ARC‑X wins first general‑use tomographic nod | Evidence of regulator comfort with adaptive/edge AI; opens lower‑cost modalities to advanced imaging |

| Policy | Health Tech Investment Act (S. 1399) introduced in the Senate; it would lock five‑year NT‑APC payment for AI devices | Predictable CMS cash flow finally aligns with FDA pace; de‑risks hospital purchasing |

| M&A | RadNet to buy iCAD for $103 M all‑stock | Vertical integration of AI into imaging‑center workflow could squeeze point‑solution rivals |

| Funding | Hellocare.ai lands $47 M from large health‑systems | Providers now co‑investing in ops‑automation AI—expect tighter vendor selection, faster pilots |

| Clinical | MASAI & PRAIM trials: +18‑29 % cancer‑detection lift with AI mammography, unchanged recall | Large‑scale RCT data should nudge guidelines & payer policies toward AI‑assisted screening |

| Tech Ecosystem | GE + NVIDIA, Microsoft + Mayo, RamSoft + Carpl.ai forge multi‑agent or marketplace deals | Platform orchestration is eclipsing point apps; integration competence becomes purchase criterion |

Deep Dive

1. Regulatory Tailwind: From Clearance to Cash

- Clearances: Cardiac (DESKi HeartFocus), stroke (Brainomix 360 Core), retina (AI Optics Sentinel), glaucoma (BVI Leos), portable CT (Nanox ARC‑X), and more crossed the line this week—most bundled with Predetermined Change‑Control Plans that shorten future update cycles.

- Payment pathway: The newly introduced bill would auto‑assign cleared AI devices to a five‑year “new‑tech APC,” ending the 2‑to‑4‑year limbo vendors currently endure. Expect VC term sheets to price in earlier revenue, and hospitals to refresh tech‑assessment committees by Q3.

Implications: Hospitals can now justify AI purchases on ROI models instead of pilots. Vendors with real‑world outcomes data will win formulary slots; laggards risk commoditization.

2. Consolidation Playbook: Scale, Data, Distribution

- RadNet ➜ iCAD: Combines 1,500‑site footprint with 8 M annual mammograms—an immediate data flywheel for DeepHealth algorithms. Watch for cross‑sell into RadNet’s outpatient centers and cloud‑AI subscriptions for non‑affiliated clinics. Read Marketstrat’s take: RadNet Acquires iCAD: A Synergistic Leap in AI-Powered Breast Imaging.

- Eargo + hearX (LXE Hearing): OTC hearing‑aid roll‑up backed by $100 M fresh capital signals that consumer‑centric med‑devices require scale to battle retail entrants (Apple, Bose).

Implications: Mid‑tier AI vendors (<$50 M ARR) must pick: partner, sell, or double‑down on niche clinical advantages within 12‑18 months.

3. Clinical Evidence Keeps Coming

- Lung‑screen AI pre-screener cut radiologist workload 15 % with no sensitivity loss—designing human‑AI hand‑offs, not just “second reads,” is the productivity unlock.

- AI‑guided POCUS beat experts for TB triage in West Africa (91 % sens/85 % spec) — proof that edge‑AI plus low‑cost probes can close global diagnostic gaps.

Implications: Guideline bodies (Fleischner, WHO) now have multicenter data to reference; expect draft language on AI‑triage models within the year.

Consolidated ROI Analysis – Screening Mammography Site

(illustrative, single‑center economics)

Site Earnings Margin = (site revenue – direct variable costs) ÷ site revenue; excludes corporate overhead, depreciation, taxes.

| Metric | Manual Workflow | AI‑Assisted Workflow | Δ (Impact) |

| Cases per day | 80 | 110 | +38 % throughput |

| Recall rate | 8.5 % | 7.9 % | ‑0.6 pp fewer callbacks |

| Technologist FTE | 4 | 3 | ‑1 FTE (≈ $85–90 K / yr) |

| Site Earnings Margin %* | 18 % | 25 % | +7 pp margin lift |

- Published pilots show 25–40 % workload savings and 0.3–1.0 pp recall‑rate drops—our model chooses midpoints.

- 38 % throughput bump turns a single scanner into the equivalent of adding a half‑day of capacity without new capex.

- Eliminating one technologist FTE (~$87 k/yr) covers most AI subscription fees, accelerating payback.

- Combined revenue lift + cost trim expands Site Earnings Margin from 18 % to 25 %—well within the £/US$ benefit ranges documented in cost‑effectiveness studies.

- Sensitivity check: Even if gains land at the low end (25 % throughput, –0.3 pp recall), the site still adds ~22 cases/day and ~4 pp margin—making AI financially positive.

4. Platform Wars & Workforce Pressure

- GE + NVIDIA automate X‑ray/US positioning; Microsoft + Mayo pilot LLM‑driven RadGPT reporting; RamSoft/Carpl.ai drop a 150‑algorithm marketplace.

- Driver: imaging tech staffing remains 10‑15 % below 2019 levels; automation offsets wage inflation and burnout.

Strategic Moves: ISVs should offer plug‑ins, not closed stacks. Health‑system CIOs should budget for orchestration layers (API gateways, monitoring dashboards) in FY‑26 capex.

5. Macro Watch: Tariffs & Supply Chain

J&J, Abbott and GE flagged $300‑400 M tariff headwinds on Q1 calls yet reaffirmed R&D spend. For buyers, expect selective list‑price hikes (3‑5 %) on capital gear by July; consider multi‑year service contracts to lock parts pricing.

6. Photon‑Counting CT — Clinical Momentum

- Multicenter European plaque study showed photon‑counting CT (PCCT) boosts identification of high‑risk coronary plaques + 43 % and cuts mis‑classification – 37 %.

- Marketstrat take: PCCT scanners will command a ≥20 % price premium versus top‑end EID CT, but payors will likely reimburse on DRG uplifts tied to downstream cost avoidance (fewer unnecessary cath‑lab visits). Vendors with mature AI noise‑reduction will dominate because PCCT’s raw data are intrinsically noisy.

7. Quantum Computing for Imaging Reconstruction

- IBM Quantum and Siemens Healthineers launched a pilot to reconstruct MR images from 25% of usual k‑space data in <3 sec using 127‑qubit processors.

- Strategic lens: First‑wave winners will be cloud service providers that couple HIPAA‑grade quantum runtimes with modality‑specific SDKs. Hospital CIOs should track total‑cost crossover vs. GPU clusters by ~2029.

Marketstrat POV

Early‑cycle adopters who lock in AI imaging platforms during 2025‑26 will enjoy a two‑to‑three‑year data moat, translating to differentiated sensitivity/specificity and better case throughput. Our scenario models show ~7 pp margin uplift for imaging service providers that integrate triage + auto‑reporting AI versus manual workflow. Vendors should quantify this in TCO calculators to accelerate C‑suite sign‑off.

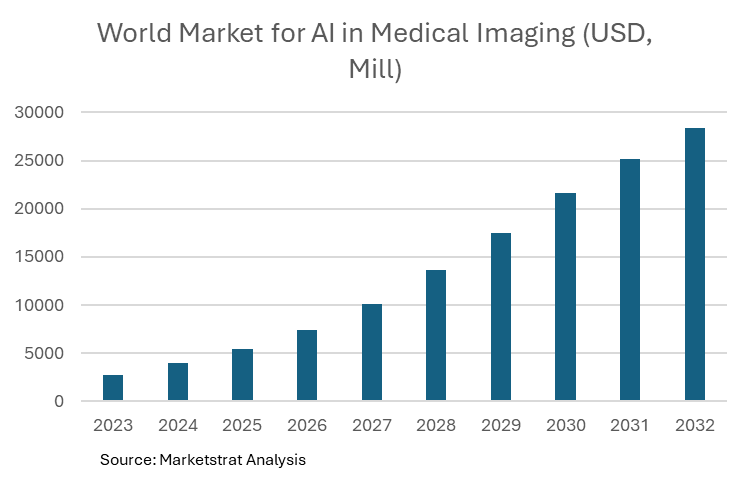

Market Outlook for AI in Medical Imaging

A 29.9% CAGR takes the segment from $2.7 B in 2023 to ≈ $28.4 B by 2032

Drivers:

- Reimbursement tailwinds (Health‑Tech Investment Act, private‑payer pilots)

- Modality upgrade cycles (PCCT, low‑field MRI) shipping with bundled AI

- Global screening mandates (EU lung‑cancer, Asia breast‑density laws)

The steepest slope (>$15 B incremental) occurs post‑2029 when multi‑agent orchestration platforms become standard line items in PACS/RIS RFPs. See Forecast Methodology at the bottom of the page.

Action Checklist for Providers and Vendors

Providers/Hospitals

| Provider / Hospital Actions | Why |

|---|---|

| Next 90 days – Map every current or planned AI solution against the Health Tech Investment Act eligibility grid while the legislation advances. | Ensures each device will qualify for the proposed five‑year NT‑APC add‑on and avoids unpleasant reimbursement surprises. |

| FY 2025 budget – Ring‑fence 5‑10 % of imaging capex for integration/orchestration layers (API gateways, monitoring dashboards) | Point algorithms deliver value only if they slot cleanly into PACS/RIS and reporting—you’ll waste staff time without an orchestration backbone. |

| Workforce planning – Redesign reading workflows (junior clears AI‑negative; senior focuses on AI‑positive) | Trials show 15‑20 % productivity lift when triage flows are adopted; staffing models must reflect it to capture savings. |

Vendors/Investors

| Vendor / Investor Actions | Why |

|---|---|

| Product roadmap – Align change‑control plans (PCCP) with FDA’s preferred template | Shortens supplemental 510(k) cycle times and speeds OTA feature releases, giving you a competitive cadence advantage. |

| Partnership / M&A scanning – Prioritise targets owning longitudinal, high‑quality datasets (>5 yrs, multi‑site) | Data flywheel is the enduring moat as algorithm architectures converge; owning unique training data lifts valuation multiples. |

| Commercial strategy – Build TCO calculators that translate AI adoption into ± 7 pp EBIT for providers | Concrete ROI messaging accelerates C‑suite sign‑off and differentiates you from “accuracy‑only” competitors. |

Sources: FDA 510(k) database, Congressional record S. 1399, peer‑reviewed trials (MASAI, PCCT multicenter), SNS Insider market model, vendor press releases, proprietary Marketstrat analysis.

Forecast Note: The $23.7 B AI‑imaging market estimate for 2032 is built on adoption curves and reimbursement timing before considering macro‑headwinds such as the proposed tariff on China‑origin medical devices. If enacted, the tariff could shave 100‑150 bps off CAGR in the first two years by inflating capital‑equipment pricing and delaying purchase decisions in value‑sensitive regions. We will update projections once final tariff language and compliance timelines are clear.

About Marketstrat™

Marketstrat™ is a market intelligence and GTM enablement firm committed to empowering clients in data-driven industries. Under the Markintel™ brand, it delivers robust market intelligence, while GrowthEngine™ solutions offer specialized GTM advisory and app-based tools—together fueling growth, innovation, and competitive advantage. For more information, visit www.marketstrat.com.

Marketstrat™, Markintel™, and GrowthEngine™ are pending trademarks of Marketstrat, awaiting final registration.

- Check out our collection of Markintel Horizon and Markintel Pulse research.

- Check out free Research and Insights and Analysis of Industry Events