Consumer-led imaging, embedded ultrasound components, MRI capacity software and FDA’s controlled-update framework are expanding the definition of an imaging AI platform.

Estimated read time: 6 minutes

The most consequential imaging AI signals this week were not additional point algorithms. Midjourney Medical tested a consumer-led distribution model, Butterfly Network expanded ultrasound into embedded component licensing, AIRS Medical attracted growth capital for cross-fleet MRI software, and FDA formalized a pathway for controlled model updates. Together, the developments show why authorization alone is no longer sufficient to explain commercial advantage.

The market is moving beyond clearance

Medical imaging AI has historically been organized around a straightforward sequence: build an algorithm, obtain authorization and sell it into a hospital or imaging-center workflow.

That sequence is becoming more complex.

This week’s developments show companies competing across several additional layers. Midjourney Medical is attempting to create consumer demand before pursuing a broader diagnostic position. Butterfly Network is supplying imaging technology as a component inside a third-party platform. AIRS Medical is scaling software that increases output from heterogeneous MRI fleets. FDA is formalizing how some imaging AI products can improve after authorization.

At the same time, breast-biopsy consumables, radiopharmaceutical production and intellectual-property enforcement demonstrate that digital productivity still depends on physical and legal infrastructure.

The result is a broader definition of imaging AI commercialization. It now includes distribution, lifecycle regulation, operating evidence, capacity economics and supply continuity.

Midjourney is testing whether demand can precede diagnostics

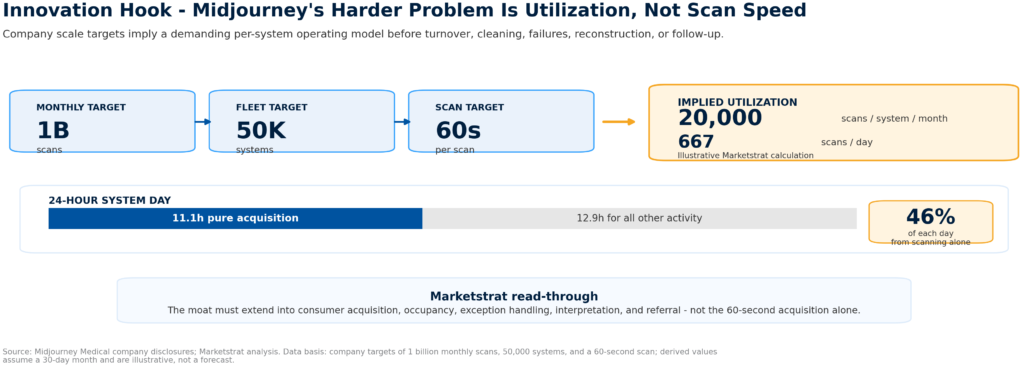

Midjourney Medical’s proposed full-body ultrasound platform has been framed around a 60-second scan and a consumer “research spa” experience.

The more strategically relevant element is the company’s sequencing.

Midjourney plans to begin with body-composition outputs and pursue additional regulated capabilities over time. This differs from the traditional imaging model, where diagnostic authorization generally precedes scaled distribution.

A wellness-first entry could give Midjourney several potential advantages. It may allow the company to develop consumer awareness, observe utilization patterns and build longitudinal data before competing directly in conventional diagnostic imaging.

It also introduces substantial risks.

Consumer expectations must remain aligned with the intended use. Findings need a responsible escalation pathway. False positives, incidental abnormalities and downstream referrals can create clinical burden. High equipment occupancy will be necessary to support the company’s stated scale ambitions.

The product therefore extends beyond the scanner. Scheduling, consent, data management, interpretation, triage and referral all become part of the operating architecture.

Butterfly is moving from finished devices to embedded imaging technology

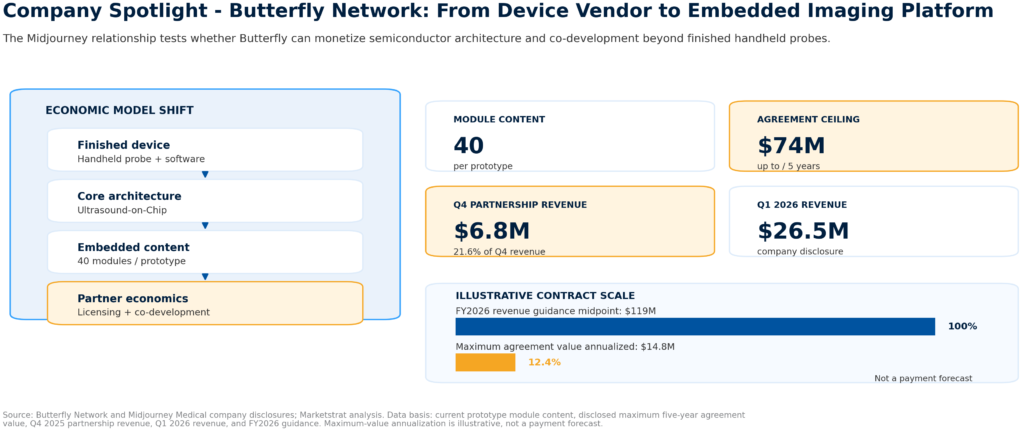

Butterfly Network is a critical part of the Midjourney architecture.

The current prototype uses 40 Butterfly Ultrasound-on-Chip modules. Butterfly’s disclosed five-year agreement provides for up to $74 million in expected payments, subject to development, commercial and contractual milestones.

The partnership illustrates how an imaging company can monetize proprietary technology beyond its original product category.

Butterfly has historically been associated with handheld ultrasound devices and enterprise software. Embedded licensing allows its semiconductor and software architecture to sit inside products designed and distributed by other companies.

That can expand the addressable market, but it also changes the risk profile. Revenue becomes more dependent on partner execution, manufacturing scale, module yield, regulatory progress and customer concentration.

The key question is whether Butterfly can repeat the model with additional partners. A single large embedded relationship is strategically useful. A diversified licensing platform would represent a broader change in the company’s economics.

FDA is defining how imaging AI can improve after authorization

FDA’s new Class II classification for radiological machine-learning quantitative software creates a more structured route for products that include predetermined change control plans.

A PCCP does not permit unrestricted model modification. It establishes planned changes, validation methods, performance boundaries and testing requirements in advance.

This matters because static authorization is increasingly inconsistent with the way software products are developed and maintained. Imaging AI vendors need to address evolving acquisition conditions, patient cohorts, scanner environments and clinical workflows.

The ability to update a product within a governed framework can reduce lifecycle friction, but it also creates a higher operating burden. Vendors need strong datasets, independent testing, subgroup analysis, post-market monitoring and documentation.

Larger OEMs and scaled software vendors may be better positioned to absorb that burden. Smaller vendors can use the same pathway, but only if they build the underlying evidence and quality infrastructure.

The competitive distinction therefore shifts from the number of authorizations to the ability to maintain regulated product evolution.

Capacity software is becoming a standalone investment thesis

TA Associates’ investment in AIRS Medical highlights another route to imaging growth.

AIRS reports that its software is deployed across more than 1,700 institutions in over 40 countries and supports more than six million MRI examinations annually. Its products are designed to improve acquisition, reconstruction, quantification and reporting across heterogeneous equipment environments.

This model differs from owning imaging centers or selling new scanners. It seeks to increase output from the existing installed base.

The economics can be attractive when time savings translate into additional exam slots, reduced overtime, lower repeat rates or improved patient access. However, technical acceleration must still be converted into operational capacity. A faster scan does not create another completed exam if scheduling, staffing, room turnover or downstream interpretation remain constrained.

Recent CT workflow data reinforce that point. A reduction of seconds per examination can become meaningful at high volumes, but the value must be measured at the site level.

Providers should therefore evaluate capacity software using operating metrics rather than image-quality claims alone.

Supply resilience remains part of imaging strategy

Digital optimization can be neutralized by a single physical constraint.

FDA expects disruptions in stereotactic breast-biopsy needle availability to continue through March 2027. For breast-imaging centers, this affects scheduling, diagnostic follow-up and procedure capacity.

Siemens Healthineers’ new UK radiopharmacy addresses a different constraint. Molecular-imaging capacity depends on reliable production, quality control and same-day distribution of short-lived radiopharmaceuticals.

Hologic’s patent enforcement against Siemens adds legal availability to the risk framework. Intellectual-property disputes can affect production, sales, recall obligations and installed-base decisions.

Together, these developments suggest that imaging capacity should be treated as a chain. The usable output of a scanner depends on labor, software, consumables, tracers, service support and legal access to the technology.

What providers, vendors and investors should take from the week

Providers should move beyond counting approved AI applications. The more useful measures are activated sites, eligible study volume, utilization, time saved, exceptions created and downstream work generated.

Vendors should define their distribution strategy before adding another model. Consumer access, embedded licensing, OEM integration, academic validation and direct enterprise sales solve different commercialization problems.

Investors should distinguish capacity software from generic workflow software. The category becomes more defensible when vendors can demonstrate incremental exams, reduced overtime or lower cost per completed study across multiple customer environments.

Payers should also separate technology that improves capacity from technology that increases unnecessary utilization. Evidence on downstream cost and outcomes will remain central.

The next phase of imaging AI will be shaped by companies that connect regulatory permission to recurring use, measurable capacity and resilient delivery.

Conclusion

The imaging AI market is not moving away from regulation. It is moving toward a more complete commercialization model.

Authorization remains a prerequisite. The stronger strategic position comes from combining authorization with controlled updates, differentiated distribution, measurable workflow value and a reliable physical delivery chain.

About Marketstrat

Marketstrat® is an independent market intelligence firm focused on MedTech, medical imaging, imaging AI, enterprise imaging, PACS, and adjacent healthcare technology markets. Through its Markintel® research methodology and publishing system, Marketstrat produces Horizon Reports, Pulse Reports, Company Research, Market Signals, and weekly Pulse Insights. The firm’s research combines market sizing, forecasting, segmentation, competitive mapping, company intelligence, and event-driven analysis to help corporate strategy, product, commercial, investment, consulting, and industry media professionals interpret fast-moving healthcare markets with greater clarity.

Marketstrat® and Markintel® are registered service marks of Marketstrat, Inc.

Our Research

- Horizon Reports — Comprehensive market landscape assessments with sizing, segmentation, forecasting, and competitive mapping across multi-year time horizons.

- Focus Reports — Targeted market intelligence reports on specific segments, technologies, or competitive dynamics drawn from Marketstrat’s broader Horizon research program.

- Company Research — Decision-grade company intelligence covering strategy, competitive positioning, product portfolio, business model, financial structure, partnerships, and stakeholder impact.

- Market Signals — Event-driven analysis tied to specific catalysts, including regulatory actions, M&A, product launches, policy shifts, reimbursement changes, and earnings. Each signal is structured around strategic implications, not just news.

- Pulse Insights — Weekly market intelligence digest covering what moved, what it means, and what to watch across healthcare, MedTech, medical imaging, imaging AI, and adjacent life sciences markets.