GE’s Intelerad close turns enterprise imaging strategy into balance-sheet reality, while new screening evidence and cyber/helium disruptions sharpen what buyers will actually fund

ONE BIG THING

Enterprise imaging crossed from conference narrative into owned infrastructure this week: GE’s Intelerad close made platform control tangible, new breast-screening AI data made labor relief more credible, and cyber/helium shocks kept resilience at the center of buying decisions.

🎧 Listen to this week’s Marketstrat Pulse Insight:

KEY TAKEAWAYS

- Enterprise imaging control moved from messaging to ownership. GE HealthCare’s Intelerad close is the week’s most material signal because it puts a cloud-first enterprise imaging layer inside an OEM stack, raising bundling leverage, recurring-software exposure, and switching-cost risk for providers and independent AI vendors.

- Breast AI finally delivered a prospective labor signal that matters. The Nature Medicine trial showed materially lower radiologist workload with higher cancer detection, but higher recall means the economics are still pathway-dependent. This is evidence for workflow redesign, not effortless margin expansion.

- Pediatric imaging remains underbuilt as a commercial and regulatory category. The JAMA labeling analysis and OXOS’s pediatric clearance expansion point in the same direction: low-friction workflow tools can move faster than pediatric-specific AI categories that require heavier evidence, labeling, and liability work.

- The model layer is commoditizing faster than the workflow layer. HOPPR’s NVIDIA integration, Circle’s vascular CT expansion, and GE’s Springbok collaboration all reinforce the same commercial truth: distribution and installed workflow matter more than open-model novelty by itself.

- Reimbursement was quiet, not solved. In the accessible strict-window source set, no material new imaging-specific CMS/MAC LCD/NCD/CPT action surfaced. That keeps enterprise contracting, throughput math, and operational ROI as the primary monetization path for imaging AI.

- MIS and medtech resilience still shape imaging budgets. Imperative Care’s financing and Stryker’s cyber disruption both reinforce that procedural ecosystems and operating resilience remain live competitors for the same hospital capital envelope.

INNOVATION HOOK

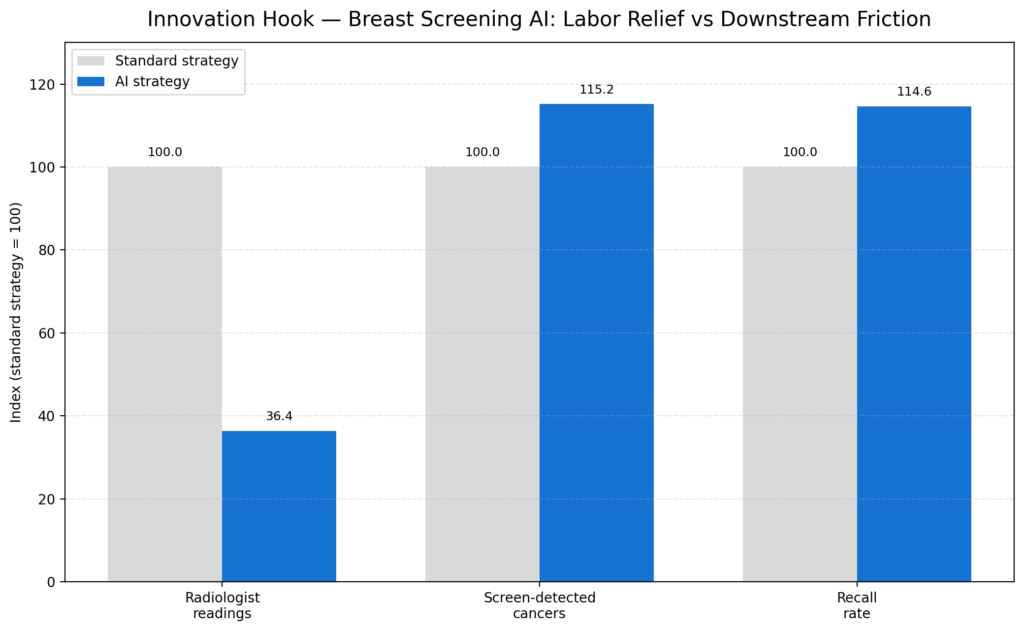

Breast screening AI finally produced prospective labor proof — but not frictionless economics

The week’s highest-signal evidence item was not another accuracy claim. It was a prospective workflow result. In the Nature Medicine study, the AI strategy cut radiologist reading volume sharply while increasing screen-detected cancers but recall also moved higher. That makes the commercial lesson unusually clear: screening AI can create real labor relief, yet the economic case still depends on what happens downstream. A buyer cannot underwrite the value of fewer reads in isolation if workup volume, callbacks, or pathway complexity rise at the same time. In practical terms, this is evidence for operating-model redesign, not plug-and-play margin expansion.

Source: Nature Medicine prospective trial; study follow-on coverage; Marketstrat analysis.

Data basis: Study-reported radiologist readings, cancer detection, and recall indexed against standard workflow.

Prospective breast-AI evidence now points to a real labor-capacity lever. The catch is that recall still matters commercially, so the value case is workflow redesign, not just “better detection.”

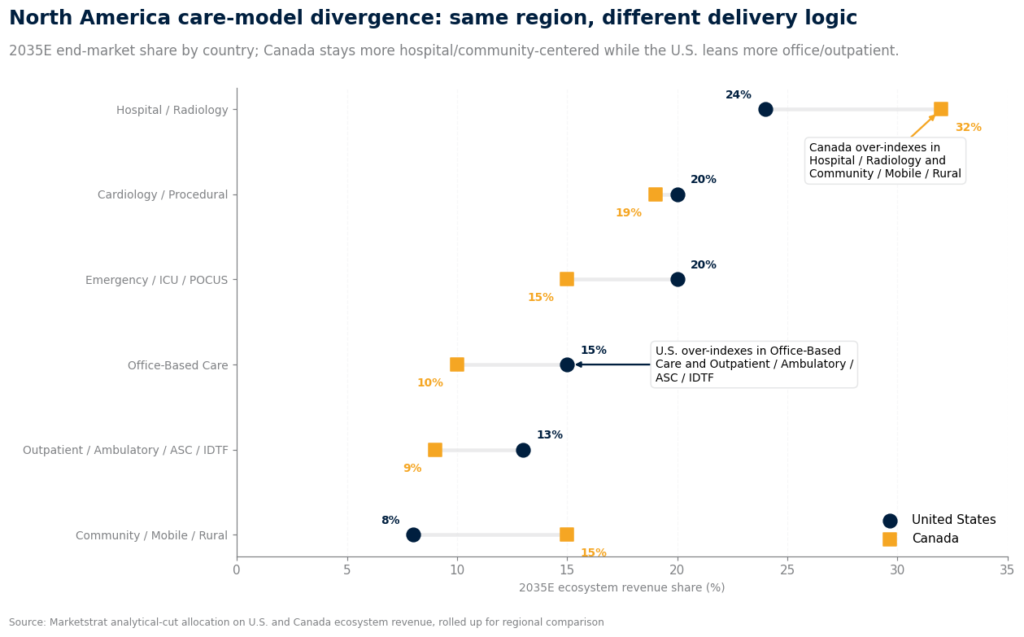

MARKET LENS – NORTH AMERICA ULTRASOUND MARKET

Care model divergence: Same region, different delivery logic

North America should be read as a mature installed-base, workflow- and labor-driven ultrasound region, not as an access-creation market. The region is still overwhelmingly U.S.-driven in scale. By 2035E, the U.S. represents about 91% of North America systems revenue, 91% of ecosystem revenue, and roughly 91% of unit shipments. Canada is much smaller in scale, but it matters strategically because it changes the regional care-model mix and highlights that North America is not one single commercial model.

The key takeaway is that the two countries are directionally aligned on technology, but not identical in delivery logic. In both markets, compact / portable becomes the largest revenue engine by 2035E and handheld / POCUS becomes the fastest shipment-growth engine. Where they diverge is in site of care, procurement logic, and monetization intensity.

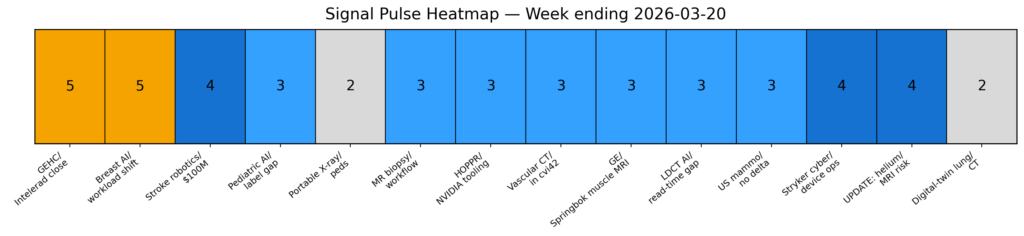

SIGNAL PULSE HEATMAP – MAR 14 – 20, 2026

Event-level

The heatmap shows a week where platform control and clinical evidence shared the top tier. GE’s Intelerad close and the new breast-AI trial both scored at the structural end of the range because they affect how buyers think about ownership and labor. Mid-tier signals clustered around financing, governance, quantification, and operational reality checks. The pattern matters: the market did not reward raw algorithm novelty this week. It rewarded events that either changed control of the deployment surface or improved clarity on whether AI actually alters operating models. That is a more mature signal pattern than the one-off clearance-heavy weeks seen earlier in the year.

The strongest signals this week were ownership and operating-model signals, not feature releases. Platform control and evidence quality dominated the score distribution.

QUICK-GLANCE TABLE

| Date | Headline | Our Take |

| 2026-03-18 | GE HealthCare closes Intelerad | Enterprise imaging moved from conference narrative to balance-sheet ownership; that raises bundling leverage, pricing power, and switching costs faster than another stand-alone AI launch. |

| 2026-03-19 | Nature Medicine breast-AI triage study | The real signal is labor-model redesign. Detection improved and reading load plunged, but higher recall means buyers still must underwrite downstream cost, not just radiologist time saved. |

| 2026-03-18 | Imperative Care closes oversubscribed $100M financing | Capital remains available where products sit inside urgent interventional workflows with training, distribution, and platform logic—not just another AI or robotics proof-of-concept. |

| 2026-03-20 | JAMA finds only 4.4% of FDA AI devices specifically labeled for pediatrics | This is a governance signal, not a footnote: pediatric AI remains structurally under-built because evidence, labeling, and liability are harder than adult imaging markets imply. |

| 2026-03-17 | FDA expands OXOS portable X-ray clearance to pediatric imaging | Portable imaging wins when it removes movement, sedation, and rooming friction. That is commercially cleaner than a broader AI pitch in pediatrics. |

| 2026-03-18 | FDA clears Mammotome Prima MR-guided biopsy system | This matters as workflow retention for premium breast programs: easier MR-guided biopsy can keep referrals and downstream procedures inside the system. |

| 2026-03-17 | HOPPR adds NVIDIA open models to imaging AI Foundry | Open models are not the moat. Workflow control, synthetic-data governance, and validation infrastructure are becoming the defendable layer. |

| 2026-03-19 | Circle CVI expands cvi42 with vascular CT analysis | Embedding vascular CT inside an installed platform is commercially stronger than launching another detached point solution. |

| 2026-03-18 | GE HealthCare and Springbok partner on MRI muscle quantification | A distribution attach move: quantification matters only if GE can convert niche analytics into a scalable installed-base workflow add-on. |

| 2026-03-18 | AJR study: AI-assisted LDCT raised actionable nodule detection but not reading speed | Higher actionable detection without faster reads shifts the buyer case from productivity to downstream pathway management. |

| 2026-03-20 | AJR single-reader U.S. mammography study shows no significant benefit | The screening-AI thesis survives, but operating-model fit matters: European double-reading logic does not automatically port to U.S. single-reader workflows. |

| 2026-03-19 | Stryker cyber fallout exposes medtech operating fragility | Stryker’s March 11 cyberattack disrupted order processing, manufacturing, and shipping globally, forcing rescheduling of patient-specific surgical cases that depended on custom implant delivery. That makes cyber resilience part of procedural uptime, not a background IT concern. |

| 2026-03-18 | UPDATE: helium disruption persists, keeping MRI operating risk live | Persistence, not novelty, is the update. Helium is re-entering MRI planning as a service and margin variable, not just a price headline. |

| 2026-03-16 | LTTS launches CT-based digital-twin lung planning platform | Interesting architecture, but without integration, procedural proof, or reimbursement, digital-twin lung platforms still risk outrunning procurement. |

This week’s Pulse research note also covers: GE HealthCare’s Intelerad close and the shift from enterprise imaging strategy to owned infrastructure; breast screening AI evidence and the real economics of labor relief versus downstream recall burden; FDA and governance signals including pediatric imaging gaps, portable X-ray expansion, and MR-guided breast biopsy workflow advances; platform-control moves across imaging IT, open-model tooling, and vascular CT analysis; MRI operational risk and medtech resilience, including helium sensitivity and cyber-related disruption; minimally invasive surgery funding and procedural ecosystem competition; and provider, OEM, payer, and AI-vendor read-through across workflow, distribution, and capital allocation.

About Marketstrat

Marketstrat® is a market intelligence and GTM enablement firm committed to empowering clients in data-driven industries. Under the Markintel™ brand, it delivers robust market intelligence, while GrowthEngine solutions offer specialized GTM advisory and app-based tools—together fueling growth, innovation, and competitive advantage. For more information, visit www.marketstrat.com.

Marketstrat® is a registered trademark and Markintel™ is a pending trademark of Marketstrat.

Check out free Research and Insights and Analysis of Industry Events

Check out our collection of Markintel Horizon and Markintel Pulse research.

Check out details on our reports, World Market for AI in Medical Imaging World Market for Oncology Imaging AI and other Pulse Reports in the Imaging space.