Dual ACC physiology trials, lower-operator maternal ultrasound, and distribution-rail concentration push imaging software closer to budgetable infrastructure

ONE BIG THING

The most important shift this week was not another point-model launch. It was convergence: two large, randomized ACC readouts materially de-risked software-first coronary physiology, Butterfly cleared a lower-skill obstetric ultrasound workflow at the point of acquisition, and distribution rails kept concentrating through teleradiology M&A and regional channel buildout. The market message is straightforward: imaging software is getting easier to underwrite when it reduces labor dependence, routes through existing operating surfaces, and sits inside familiar workflows—but monetization still runs into utilization management and access friction.

TOP EVENTS

Coronary physiology software crossed a proof threshold

ALL-RISE and FAST III matter together more than either would alone. ALL-RISE showed FFRangio performed similarly to pressure-wire testing in 1,930 patients and was faster with less fluoroscopy and contrast, while FAST III showed vFFR-guided revascularization was noninferior in 2,211 patients across 37 sites in seven European countries, with shorter procedural time and fewer intraprocedural complications. That combination moves the commercial debate away from “does software physiology work?” and toward “who owns cath-lab workflow, installed-base distribution, and reimbursement translation?”

Butterfly turned maternal ultrasound into a site-activation story

Butterfly’s clearance is important because it does not merely enhance interpretation; it reduces expertise requirements at acquisition. The cleared tool is the first FDA-cleared blind-sweep ultrasound AI tool for estimating gestational age, is designed to return a result in under two minutes through a three-step workflow, and targets emergency settings, rural U.S. access gaps, and maternal-health use cases in lower-resource settings. That is a stronger commercialization story than a retrospective review algorithm because it can activate new points of care rather than simply improve existing expert workflows.

Distribution rails kept strengthening

Premier’s GLOBIS acquisition and Nanox’s back-to-back U.S. distribution agreements reinforce the same truth: route-to-market matters more than another stand-alone modality claim. Premier added subspecialty teleradiology capacity and roughly 350,000 annual reads, while Nanox’s regional partners were selected explicitly for commercial reach, field service infrastructure, implementation, and uptime support. In imaging, the company that controls the operating surface usually decides which software gets routable access.

Installed-base software stayed easier to budget than capital replacement

GE HealthCare’s True Definition DL clearance and Stanford’s new imaging Center of Excellence illustrate the same installed-base logic from different angles. The clearance extends a CT software stack that can travel across existing equipment, while the Stanford collaboration deepens the translational and reference-site infrastructure around next-generation imaging, AI, MRI, CT, and interventional workflows. This is the kind of software-plus-validation architecture that enterprises can fund before they fund wholesale fleet refresh.

Reimbursement still lagged deployment momentum

UnitedHealthcare’s April 1 prior-authorization expansion was the week’s most practical reminder that commercialization friction can reappear faster than reimbursement expands. Adding CT cerebral perfusion and brain MRI quantitative analysis codes to PA does not block innovation, but it does raise the operational burden for providers and vendors who hoped coding progress alone would smooth adoption.

MIS kept competing for the same capital envelope

Distalmotion, Merit, Restore, and Boston Scientific all reinforced that procedural ecosystems continue broadening their economic case around utilization density, workflow control, and recurring-spend leverage. For imaging buyers, this matters because capital committees are still comparing imaging modernization against procedural platforms that promise device revenue, software attach, and service-line control at the same time.

KEY TAKEAWAYS

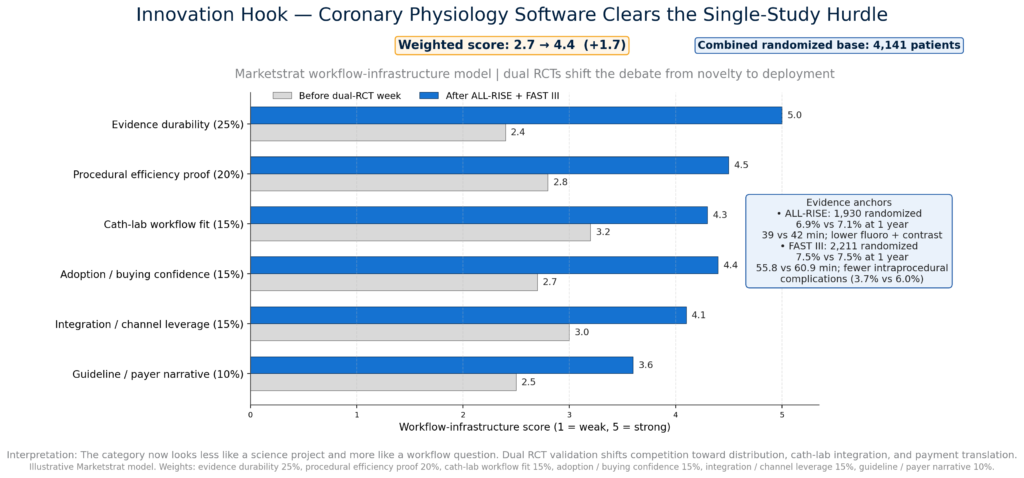

- Evidence quality improved materially. ALL-RISE randomized 1,930 patients and FAST III randomized 2,235 and 2,211 analyzed, giving software-first coronary physiology a combined 4,141-patient randomized evidence base in one conference window and reducing the usual “single-study novelty” objection.

- Butterfly delivered the week’s clearest access signal. Its FDA-cleared blind-sweep gestational-age tool estimates GA in under two minutes through a three-step workflow and is designed to eliminate image capture, interpretation, and fetal biometry requirements at the point of scan.

- Distribution remained the practical moat. Premier’s GLOBIS deal adds roughly 350,000 annual reads and marks its fourth teleradiology acquisition in recent years, while Nanox signed back-to-back regional distribution agreements built explicitly around service coverage, implementation, and uptime.

- Installed-base software is still the cleanest imaging monetization lane. GE HealthCare’s True Definition DL received FDA clearance on March 23, extending the software-defined CT upgrade stack without requiring a full modality replacement cycle.

- MIS signals were about utilization density and recurring spend, not robotics theater. Distalmotion’s gynecology submission broadens outpatient procedure mix, Merit moved earlier into lesion localization through View Point, and Restore attacked recurring da Vinci Xi instrument economics through remanufacturing clearances.

- Reimbursement friction remained active. UnitedHealthcare added 70472, 70473, 0865T, and 0866T to prior authorization effective April 1, reinforcing that coding progress does not stop utilization management from tightening operationally.

INNOVATION HOOK

Coronary physiology software cleared the “single-study” hurdle

The highest-signal evidence item this week was the pairing of ALL-RISE and FAST III. ALL-RISE showed FFRangio produced similar one-year outcomes to wire-based FFR while reducing procedural steps, time, fluoroscopy, and contrast. The real shift is not another ROC curve. Two large RCTs in one ACC window make coronary physiology software easier to defend as workflow infrastructure, which pushes competition toward distribution, integration, and payment translation.

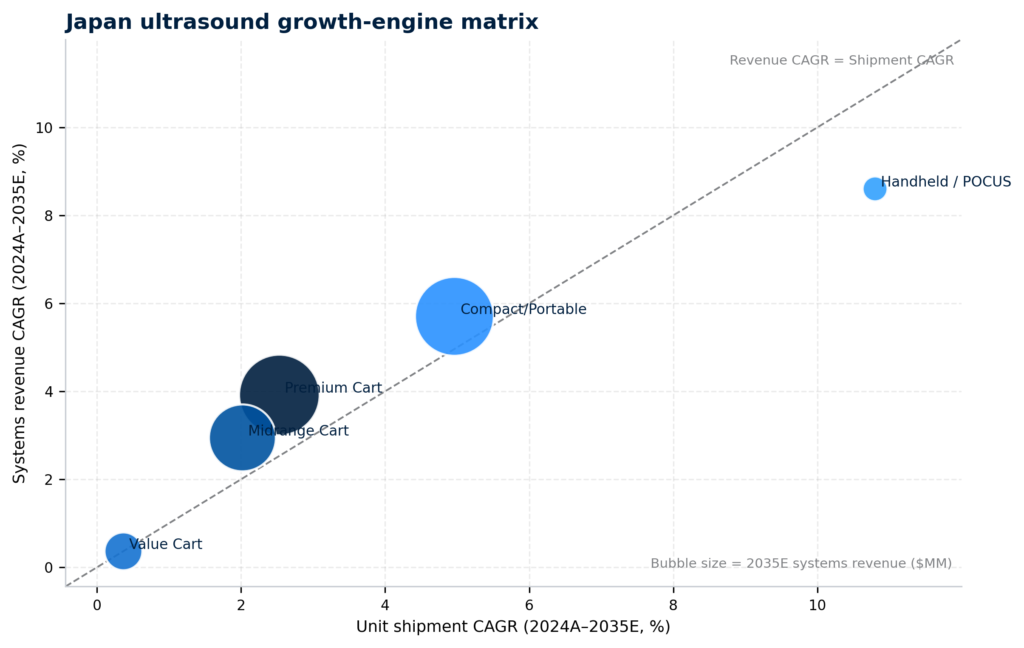

MARKET LENS – JAPAN ULTRASOUND MARKET GROWTH-ENGINE

Japan is a steady-growth, modest-mix-shift market, broadening into more placements and more lower-ASP form factors over time.

This chart separates volume growth from value growth in one view. Compact / Portable is the main scale growth engine: it is one of the largest bubbles and grows strongly on both axes. Handheld / POCUS is the clearest volume-led expansion engine: it is farthest to the right, with shipment growth materially above revenue growth. Premium Cart and Midrange Cart sit above the diagonal, which means revenue growth modestly exceeds shipment growth and monetization holds up relatively well. Value Cart sits near the origin, confirming that it contributes little to forward growth.

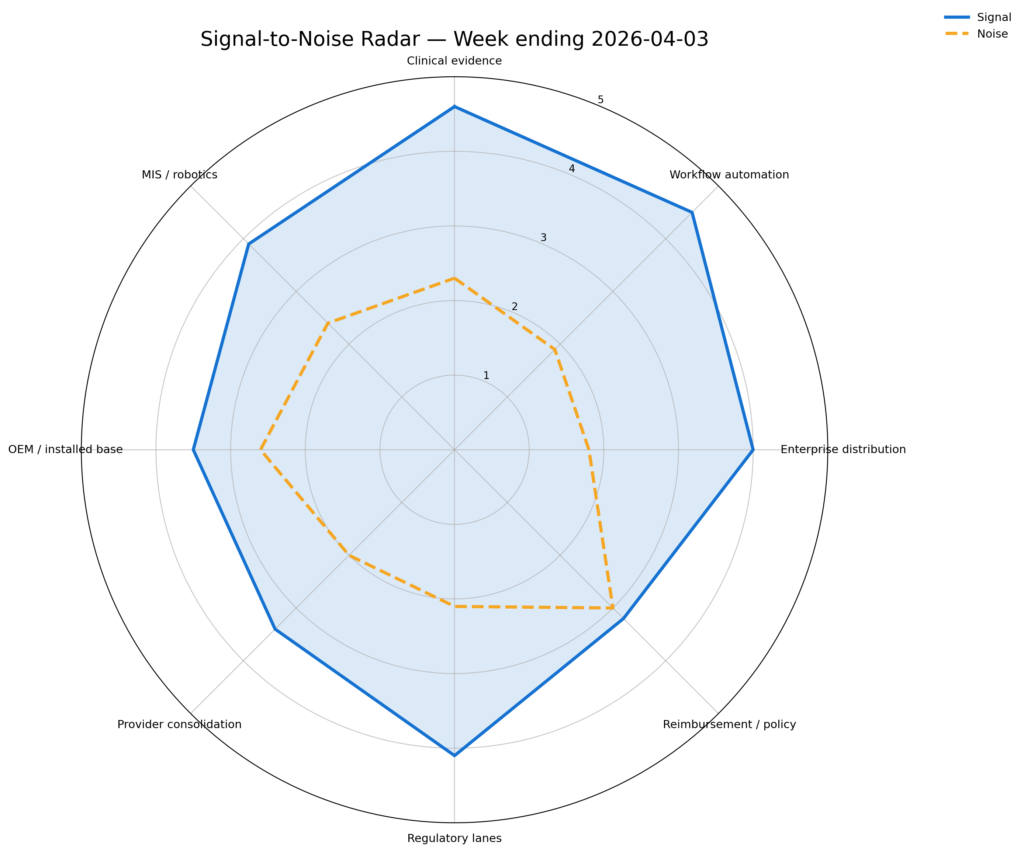

SIGNAL-TO-NOISE RADAR BY TOPIC – MAR 28 – APR 3, 2026

The clearest signal sat in clinical evidence, workflow automation, and enterprise distribution. The noisiest lane remained reimbursement/policy, where operational friction increased but no broad payment unlock offset it. Capital-market funding also remained secondary to routability: Lucida’s financing was relevant, but still less commercially decisive than the week’s workflow and distribution signals.

QUICK-GLANCE TABLE

| Date | Headline | Our take | Source key |

| Mar. 29 | ALL-RISE validates FFRangio | One RCT can be debated; two large same-window physiology readouts push the category toward workflow infrastructure. | Q1 |

| Mar. 29 | FAST III validates vFFR | The second RCT shifts the competitive question from novelty to integration, distribution, and payment translation. | Q2 |

| Mar. 30 | Butterfly clears blind-sweep GA AI | This is an access and staffing story more than a feature story because it lowers acquisition skill requirements. | Q3 |

| Apr. 3* | GE True Definition DL shows in-week on FDA tape | Software-defined CT remains easier to fund than modality replacement. | Q4 |

| Apr. 1 | Distalmotion broadens U.S. gynecology push | ASC robotics gets more defensible when one platform can carry more gyn volume in the same day. | Q5 |

| Apr. 1 | Merit buys View Point | Merit moves earlier into the imaging-to-intervention chain, where lesion localization is a workflow control point. | Q6 |

| Apr. 3 | Premier buys GLOBIS | Reading-network scale remains one of the strongest real-world AI distribution rails. | Q7 |

| Apr. 1–2 | Nanox signs two U.S. channel deals | Lower-cost imaging only scales when distribution density and field support show up with it. | Q8 |

| Mar. 31 | Restore adds Xi remanufacturing clearances | Recurring instrument economics remain one of the easiest robotic weak spots to attack. | Q9 |

| Apr. 1 | UHC adds imaging-AI and CT perfusion codes to PA | Monetization friction can tighten even when technology momentum improves. | Q10 |

Source key

- Q1 — ALL-RISE / ACC.

- Q2 — FAST III / ACC.

- Q3 — Butterfly blind-sweep gestational-age clearance.

- Q4 — GE True Definition DL 510(k).

- Q5 — Distalmotion gynecology submission.

- Q6 — Merit / View Point acquisition.

- Q7 — Premier / GLOBIS acquisition.

- Q8 — Nanox Elite + Integrity distribution agreements.

- Q9 — Restore Robotics remanufacturing clearances.

- Q10 — UnitedHealthcare prior authorization additions.

*FDA decision date was March 23, 2026; in-week visibility landed via the active FDA database tape.

About Marketstrat

Marketstrat® is an independent market intelligence and advisory firm focused on MedTech, medical imaging and AI-enabled healthcare. Guided by its Markintel™ methodology, Marketstrat publishes specialized research and briefings, and provides custom research and advisory work that help leaders evaluate market opportunity, track competitive, regulatory, and evidence shifts, and make sharper strategy, product, and commercialization decisions.

Marketstrat® and Markintel™ are trademarks of Marketstrat Inc. All other trademarks are the property of their respective owners.

Check out free Research and Insights and Analysis of Industry Events

Check out our collection of Markintel Horizon and Markintel Pulse research.

Check out details on our reports, World Market for AI in Medical Imaging World Market for Oncology Imaging AI and other Pulse Reports in the Imaging space.