Individual License: $4,950 | Team and Enterprise License Options Available

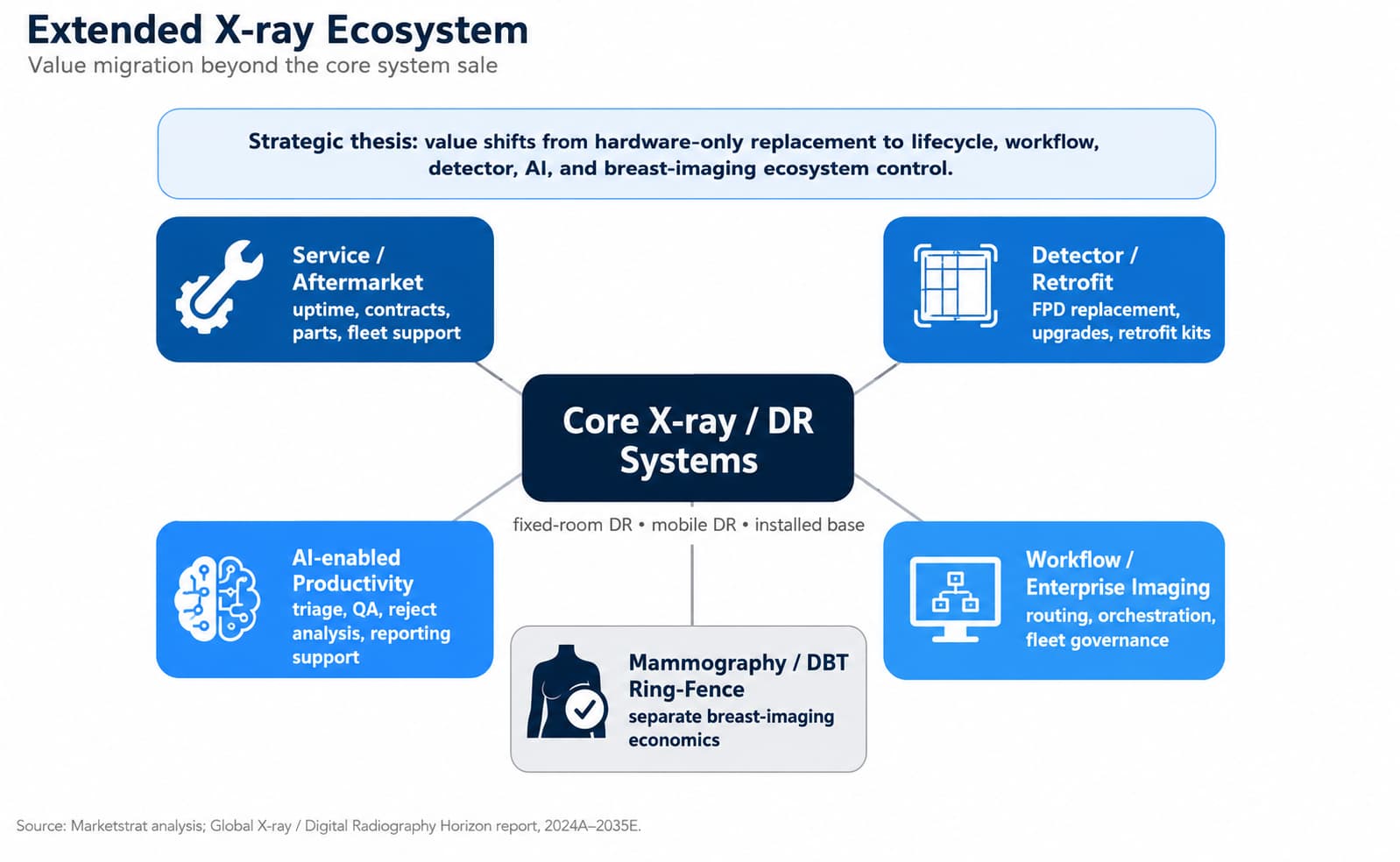

X-ray / Digital Radiography is one of medical imaging’s most widely deployed modalities, but it is no longer best understood as a simple hardware replacement market. Fixed-room and mobile DR systems remain essential, but the category’s profit pool is increasingly shaped by service attachment, detector replacement, retrofit economics, workflow software, AI-enabled automation, enterprise fleet control, China procurement pressure, and a ring-fenced mammography / DBT adjacency.

This Marketstrat® Horizon report answers the questions senior leaders are now asking: where does X-ray / DR still grow, where is hardware being commoditized, which segments remain defensible, how much value sits above the system sale, and which competitors are positioned to capture the next layer of revenue?

The report models core fixed-room and mobile DR systems, then layers in service / aftermarket revenue, recurring AI and workflow software, detector / retrofit overlays, and mammography / DBT ecosystem economics. The result is a structured view of the broader X-ray / DR value pool rather than a narrow equipment-shipment forecast.

This Horizon report is Marketstrat’s in-depth global analysis of the X-ray / Digital Radiography market and broader X-ray / DR ecosystem. It is built for medical imaging OEM executives, strategy and corporate development teams, service and aftermarket leaders, detector and component suppliers, AI and workflow vendors, enterprise imaging platforms, investors, private equity, and provider-side imaging leaders.

The report is designed to answer a practical commercial question: how does value get captured in a mature modality when the core hardware market is replacement-led and price pressure is rising?

The answer is not a single number. The report separates the market into layers:

- core fixed-room and mobile DR systems,

- service and aftermarket revenue tied to the installed base,

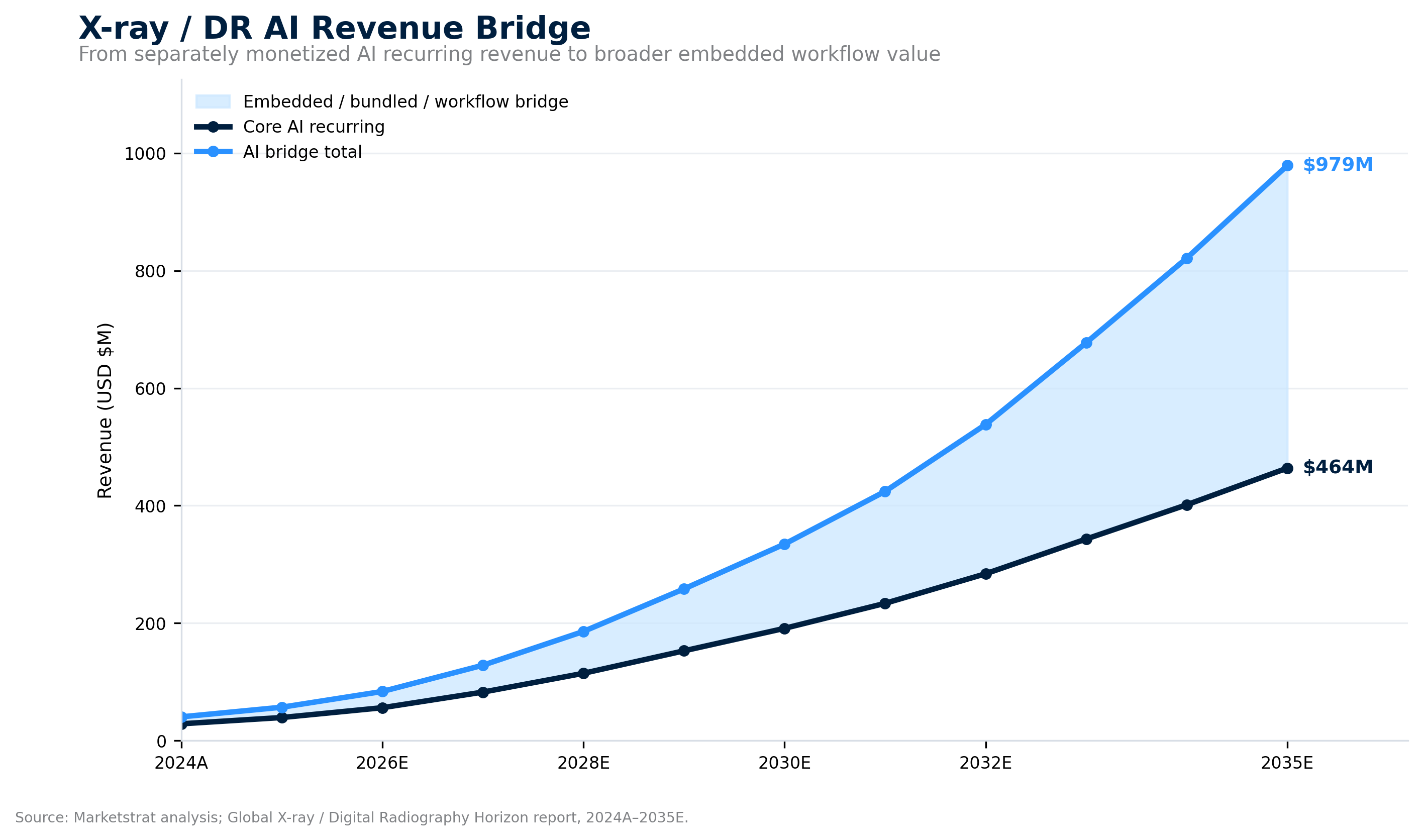

- recurring AI and workflow software revenue,

- detector replacement and retrofit economics,

- mammography / DBT as a ring-fenced adjacent ecosystem,

- and competitive control planes across hardware, service, workflow, AI, enterprise imaging, and China value channels.

The goal is not just to size the market. It is to explain which segments are defensible, where procurement pressure is highest, where installed-base monetization accumulates, how AI becomes paid software rather than an embedded feature, and which vendors are best positioned to capture value above the initial system sale.